Why Would Any Voter Trust Republicans To Make A 'Better' Economy?

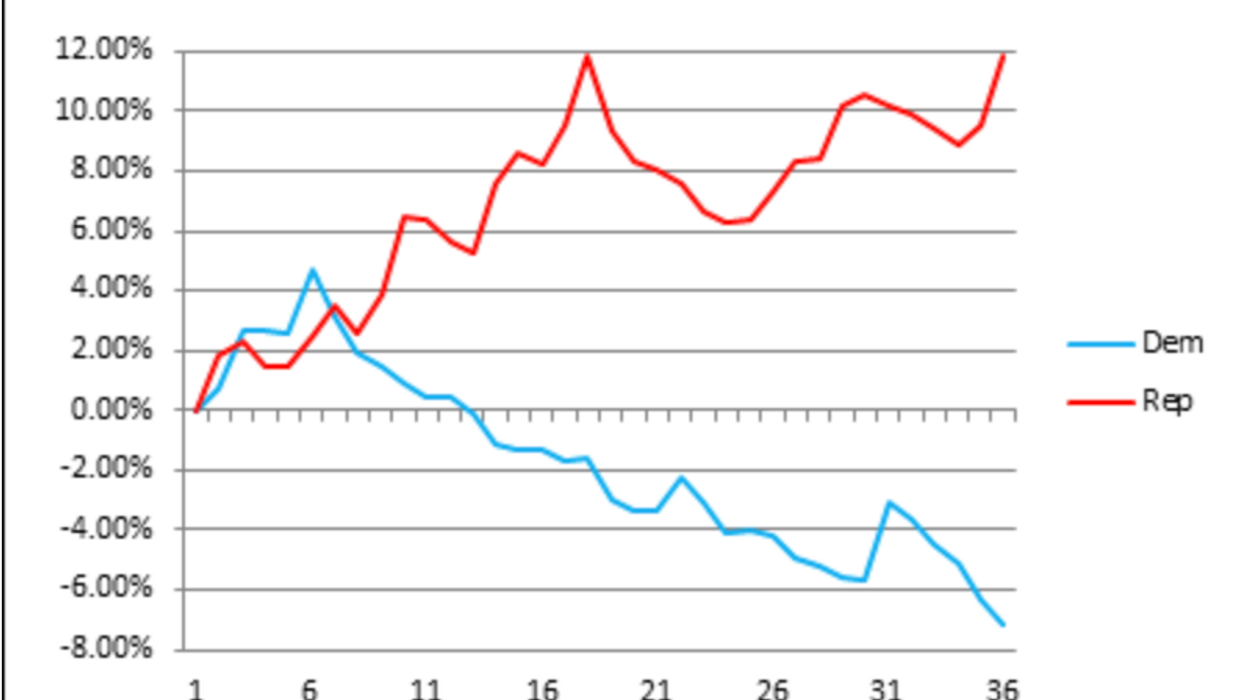

No delusion misleads American voters more than their certainty that Republicans are "better" and more worthy of "trust" on the economy than Democrats. Neither facts nor history support this durable fallacy, discredited by reams of studies over the years proving that Democratic administrations are consistently more successful in fostering economic growth, employment, family incomes, and nearly every other measure of prosperity — including reductions in the national debt.

That axiom has held true even when a Democratic president inherited the most miserable economic conditions from a Republican predecessor. It is certainly true of President Joe Biden, whose efforts to revive the United States from its pandemic slump have smashed records in the number of jobs created and sustained high employment. Inflation is beginning to abate, as are gas prices, and even so the latest quarterly data show renewed growth.

Yet because Americans are aggrieved over rising prices — and frightened by a potential recession — the mythology of Republican economic superiority now looms over the midterm elections. Evidently some voters aim to punish Biden for inflation by empowering his right-wing adversaries.

Before they do, perhaps they should ask how Republicans will exploit that enduring "trust" — and whether the result will be a "better" economy for them and their families. Based on past performance, and what Republican politicians themselves tell us, the only constituency that will see a better economy is the superrich.

In 2016, Donald Trump said he would close loopholes that allowed the very wealthy (including him) to avoid taxation. He also promised to erase the national debt and deficits in his first term. Instead, Trump and the Republicans in Congress passed an enormous tax cut that favored the wealthiest and inevitably exploded the deficit. Then the economy crashed.

Whatever their differences, that dismal Trump record is pretty much what George W. Bush achieved as president too. It is what Republicans always do.

Slashing taxes on the wealthy is what they yearn to do again — except that Sen. Rick Scott, who chairs the National Republican Senatorial Committee, has added an even "better" idea: He wants to raise income taxes on poor and working families, who make too little money to pay that levy under current law.

If you're a middle-class or working-class voter, in fact, there is a familiar agenda of economic policies that you can "trust" the Republicans to promote, because they are the same policies that the reactionary party has endeavored to enact since forever. They have vowed yet again, for instance, to ruin Social Security, Medicare and Medicaid, which serve as economic bulwarks for most Americans. And once more they are threatening to weaponize negotiations over the national debt ceiling to ram through those destructive cuts.

Will that be "better" for the older and disabled Americans who depend on those programs, and their families? Probably not, but what could be even worse is the recklessness of Republicans who would abrogate the credit of the United States Treasury to complete that cruel mission. So determined are they to cancel the benefits that Americans spend a lifetime earning that they would jeopardize the entire nation's economic stability.

You can "trust" their commitment to such financial insanity, which they continue to proclaim in this campaign, because they have pursued the same catastrophic scheme dating back to the bad old days of Speaker Newt Gingrich.

You can also trust the Republicans to seek total repeal of Biden's student-loan forgiveness plan, because they attempted to zero out all the federal student loan programs (the opposite of what Trump promised). Would that work "better" for middle-class students and their families? Presumably not, but it's what they insist on — with no proposal to improve college affordability.

For them it is now a matter of principle to have no principles, no platform, no constructive program. Remember when Trump promised a beautiful new health plan to replace the Affordable Care Act with something better that would insure everyone at low cost? Of course you do, just as you remember "Infrastructure Week," which came and went and came and went like Groundhog Day (until Biden finally passed the landmark Infrastructure Act).

In power, the Republicans will take that same pernicious approach to every aspect of economic policy that might improve life for working families. Not only would they refuse to increase minimum wages — highly popular across party lines — but nearly every one of them rejects the very idea of a minimum wage. They would obstruct any effort to reduce the cost of prescription drugs — also very popular — and repeal the provisions of the Inflation Reduction Act that are driving down those prices. They may still be too incompetent to repeal Obamacare, but that won't stop them from trying — and they will propose no "better" insurance plan to replace the health coverage they're so eager to strip away.

What you can assuredly trust the Republicans to do is what they always do. What you must never expect from them is anything better.

To find out more about Joe Conason and read features by other Creators Syndicate writers and cartoonists, visit the Creators Syndicate website at www.creators.com.