On Monday, the White House released the 2014 Economic Report of the President, providing insight into the economic progress made in the United States since the 2007-2008 global banking crisis, and presenting an optimistic prediction for the next several years.

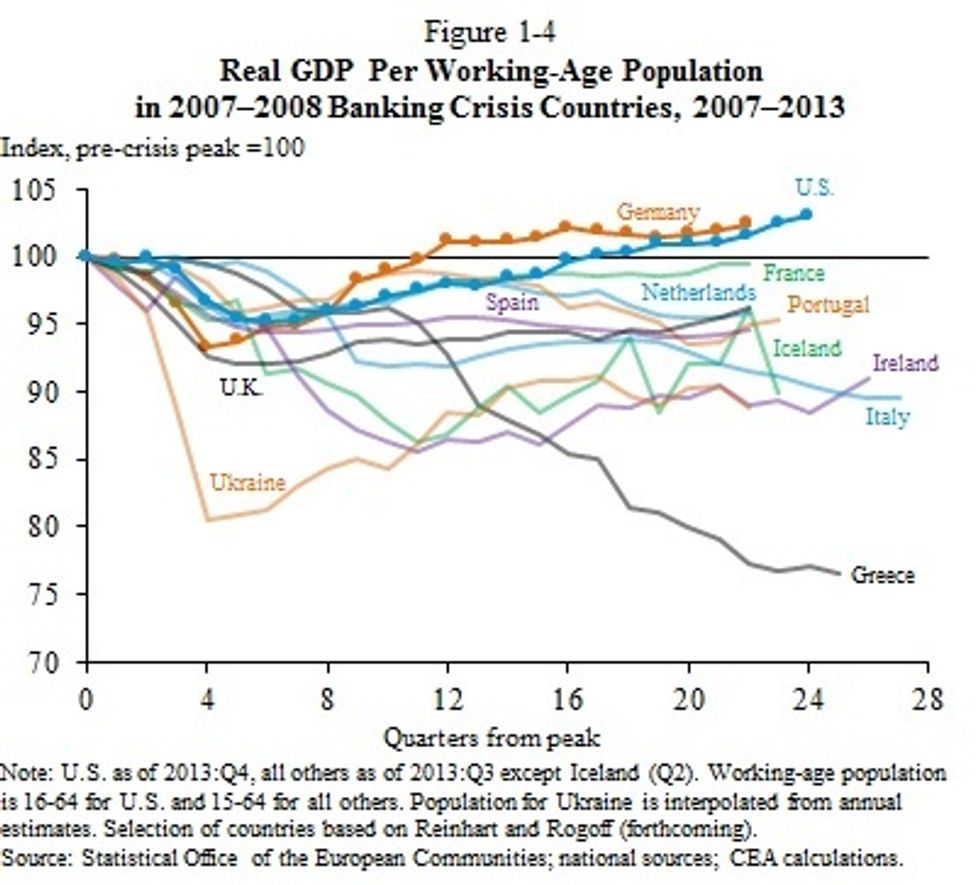

The report, compiled by the White House Council of Economic Advisers (CEA), highlights the positive gains made nationwide in the wake of the worst global financial crisis since the Great Depression. The gains are especially notable because they do not reflect sporadic economic advancements made only in concentrated areas, but rather widespread improvements that have allowed the rate of output per working-age person to return to pre-crisis level.

Among the 12 countries impacted dramatically by the crisis, only Germany experienced a nationwide economic recovery quicker than that experienced by the United States; by the end of 2008, Germany had reached its pre-crisis gross domestic product levels per its working-age population. The United States reached the same level two years later, in 2010.

The White House, which describes the country as “one of the best performing economies” since 2007, attributes the economic progress to the “full set of policy responses,” which were made under President Barack Obama.

According to the CEA, the Recovery Act of 2009 “raised the level of GDP by between 2 and 2.5 percent from late 2009 and through mid-2011.” Further contributing to GDP growth were “more than a dozen additional fiscal measures to create jobs and strengthen the economy” signed by the president. Those measures included the extension of federal unemployment insurance, small business tax cuts, and the payroll tax cut. The combined result of the Recovery Act and the later fiscal initiatives is a 9.5 percent GDP boost from 2009 to 2012.

Recovery has also meant an additional 2.4 million jobs added by businesses in 2013 – “the third straight year private employment has risen by more than 2 percent.” This may play a role in the decline in household debt, which has been falling since 2007. The report specifically attributes future economic progress to a greater percentage of households nationwide paying off debt, which then enables them to spend more – a process known as “deleveraging.”

The report adds that “a recovery in asset values, strengthening among our international trading partners, and demographic forces that are expected to maintain upward pressure on housing starts” all point to greater economic growth in 2014.

Still, the report concedes that the nation has not yet reached a full recovery, and there are still issues that must be combated in order to ensure economic growth and opportunity for all. The CEA admits that income distribution – which influences overall GDP and economic growth – has a “profound” effect on poverty. With rising income inequality plaguing the the middle and lower classes, many Americans have not actually felt the benefits of a recovering economy. Even if the economy continues to improve in 2014 and beyond, the widening gap between the nation’s rich and poor means that only a small population of Americans will benefit. This is perhaps why, as a Gallup poll released Tuesday finds, confidence in the economy among Americans continues to decline (57 percent now believe the economy is getting worse).

In order to boost the long-term overall economy, the CEA suggests federal funds be allocated to effective federal programs meant not only to help low-income Americans and the homeless, but also to set a foundation upon which the poor and unemployed are more easily able to access economic opportunities.

While the report offers good news, it also serves as a warning for those critical of the federal government’s “safety net“: These programs are among the most important means of achieving a full recovery in the coming years.

Chart via WhiteHouse.gov