Health Insurance Premiums Are Set To Soar Just Before Midterm Elections

Anyone whose employer provides health coverage knows the drill. Each fall, they are offered a menu of potential health care plan choices for the following year.

It usually includes three options. First, there is a preferred provider plan, which pays most of the bills, has few limits on provider choice, and has the highest paycheck deduction. Second comes a mid-priced health maintenance organization plan, where provider networks are limited, prior authorization rules are strict, and co-pays and deductibles are moderate. Finally, there is a high-deductible plan, which has the smallest paycheck deduction, but can leave an individual or family with large, unaffordable bills when anyone covered by the plan requires hospitalization or expensive treatment.

The employer share for any one of those plans (the average family plan cost is nearing $30,000 a year) usually hovers around 75 percent of the total cost. Workers pick up the other 25 percent through a payroll deduction. In the decade after passage of the Affordable Care Act, the annual increase averaged around 6-7 percent or about the same rate as economic growth after inflation was taken into account.

But during the pandemic, health care cost began a rapid ascent to around 8-8.5 percent annually. Now, it has taken another upward lurch.

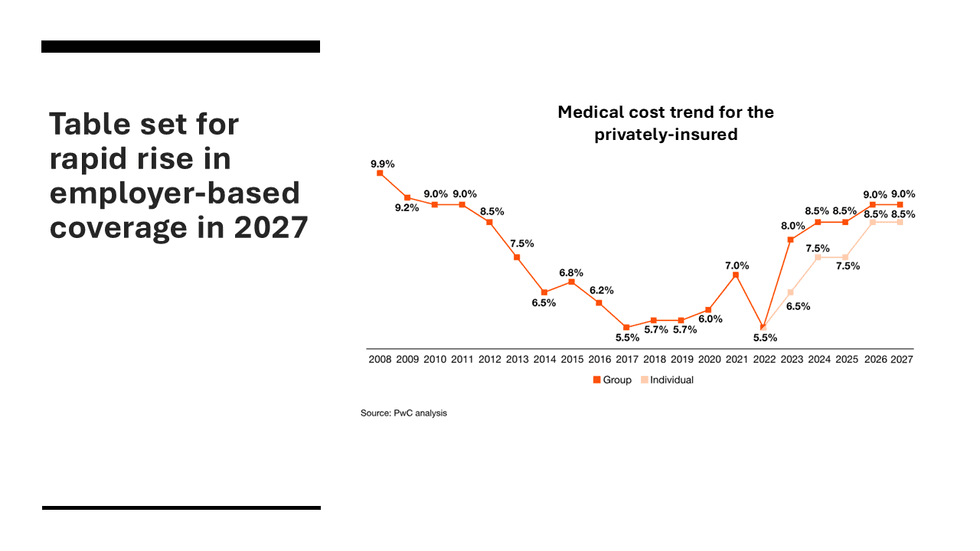

A new survey of health care actuaries by PwC (formerly known as Price Waterhouse Coopers) found private health insurers medical claims costs are rising at a nine percent clip this year and are expected to rise by a similar rate next year. Last year’s survey pegged this year’s expected cost increase at 8.5 percent.

“Health plans are projecting the highest medical cost trend in nearly two decades,” the consulting group said in its analysis. “Payers and employers face mounting pressure to act.”

This could prove a financial fiasco for people on employer-based plans, which cover about 160 million workers and their families. They will likely face co-premiums, co-pays and deductibles in their 2027 plans that are rising at nearly three times the rate of inflation.

And it could be a lot worse than that. As actuaries inside the insurance companies map out their costs, they will have to take into account the additional price increases levied by hospital systems due to rising utilization, AI-enabled billing tactics, and what’s likely to be a rapid rise in unpaid bills.

The sharp cutbacks in Medicaid contained in the One Big Ugly Bill signed by President Trump last year will hit in full force in 2027. Well over ten million impoverished Americans are expected to lose coverage due to their inability to leap over the bureaucratic hurdles erected to enforce the legislation’s work requirements.

Millions more are dropping coverage and falling into the ranks of the uninsured due to the Republicans’ refusal to extend the expanded subsidies in ACA plans enacted by Democrats during the Biden administration. Both cuts will trigger a huge increase in uncompensated care at the nation’s safety net hospitals that serve low- and moderate-income communities.

Like all hospitals, safety net hospitals must provide emergency treatment for anyone who lands on their doorstep thanks to the 1986 Emergency Medical Treatment and Labor Act, which was signed into law by President Ronald Reagan. Unlike their suburban counterparts, who face far fewer cuts because they serve mostly the privately insured, these safety nets have fewer resources and small or no endowments to fall back on.

The final rates will be determined by medical actuaries inside the insurance firms over the next few months. The rates for 2027 are usually unveiled in mid-October.

How will employees respond if they see their paycheck premiums rising at a near double-digit rate? Many more low-income workers will opt into high-deductibles plans, which will leave many with unpayable medical debt because they can’t afford the out-of-pocket expenses when someone in the family gets sick. More middle-class workers will opt into HMOs with their network limitations and prior authorization restrictions to save on their upfront costs.

The nation’s employees with employer-sponsored coverage will be making those decisions starting on November 1, the traditional date for open enrollment for the ensuing year. That’s two days before the midterm elections.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News