The polls have dealt Democrats a strong hand heading into the mid-term elections. Health care affordability has emerged as Americans’ number one pocketbook concern, with voters trusting the minority party far more than Donald Trump and the GOP on the issue.

But that reality is now shrouded by the fog of war. The looming quagmire in the Middle East – it’s already costing lives, treasure and depleting the nation’s arsenal – will dominate political discourse as long as the bombs continue to fall. The electorate will soon realize that this will be their new normal for many months, and possibly years, to come.

The political fallout is predictable. The quarter of the electorate that are MAGA diehards will rally round the flag. Another quarter in the antiwar left (myself included) will scream about the flagrant violations of international and domestic law while reminding Americans of the repeated fiascos in Vietnam/Afghanistan/Iraq. The minimally-engaged middle will split, vacillating between its pro-Israel, anti-Iran sympathies and the gnawing fear that any attempt at nation-building through force of arms – especially led by this Trump mob – is unlikely to end either soon or well.

From the perspective of domestic health care policy, there may some benefit to a pause in the discussion. Over the past several months, I’ve read a number of op-eds and articles offering reform plans from leading health care thinkers, each of whom has close ties to various factions within the Democratic Party. I was not impressed.

Big problems, especially when it comes to affordability, require bold solutions. They must directly address the health care spending crisis as it is being experienced by average Americans. Most importantly, it must address the affordability crisis as it is being experienced by the working age population — the 170 million people with employer-based coverage, where co-premiums are soaring, deductibles are rising, and co-pays for expensive treatments are out of control.

For any plan to win broad political support, it must provide immediate relief — minor fixes won’t get the job done. And, most importantly, proposed solutions must be easily understood by the general population so that politicians who champion them can win broad political support for the legislation.

It is especially disturbing to me that leading thinkers in and around the Democratic Party continue to assert competition policy will address the immediate affordability crisis. No reforms that rely on the magic of the market can succeed in health care because health care does not behave like other commodities. Every sub-sector of the health care economy – insurance, hospitals, physician services, drugs, medical devices – is marred by systematic marketplace failure.

Nobel Prize-winning economist Kenneth Arrow outlined this reality in a seminal article in the American Economic Review more than six decades ago. “The special economic problems of medical care can be explained by adaptations to uncertainty in the incidence of disease and in the efficacy of treatment,” he wrote. In plainer language: No one knows when they’re going to get sick and the outcomes from treatment are variable and cannot be determined in advance. In his article Arrow laid out the many “adaptations to uncertainty” that led to market failure in each health care sector before concluding: “The logic and limitations of ideal competitive behavior under uncertainty force us to recognize the incomplete description of reality supplied by the impersonal price system.”

Yet numerous health economists and policy pundits continue to push competition policy – rigorous enforcement of antitrust laws to bolster price competition – as the solution to the problem of the U.S. paying the highest prices in the world for drugs, hospital care, and physician services. The latest articulation of this point of view comes from Dr. Ashish Jha, the dean of the Brown University School of Public Health who served as President Biden’s Covid-19 coordinator in 2022 and 2023.

Competition will not save us

In the first three parts (Part 1, Part 2, Part 3) of what promises to be an eight-part series in the Boston Globe, Jha argues that Americans pay the highest prices in the world (true), not because they consume more health care (also true), but because “in many American communities, there have been real breakdowns in the market. Patients largely cannot shop because they have too few choices (and) prices are opaque”

His solution is to break up the monopolistic hospital and insurance chains that dominate most regional health care markets in the U.S. In his most recent piece, co-written with Dr. Thomas Tsai, who teaches surgery at Harvard Medical School, they address the hospital sector, which is close to 40 percent of all health care spending. Jha and Tsai would foster competition by repealing certificate of need laws (a holdover from 1970s-style regulation that requires government approval of new facilities); allowing physicians to own hospitals; and encouraging more growth of ambulatory surgical centers, the in-and-out shops for minor procedures. This added competition, they conclude, will bring prices down and thereby lower household and business insurance premiums.

This approach represents the triumph of economic theory over experience. Most health care services are not even knowable in advance, much less shoppable. No one in the middle of a heart attack goes looking for the lowest cost ER. Chronic disease treatments (for cancer, diabetes and heart failure, for instance, which account for the majority of health care expenditures) are driven by physician prescriptions and recommendations, not consumer choice.

While estimates vary, shoppable services (low-cost lab and imaging tests; or discretionary cataract and replacement joints surgeries, for instance) account for less than 20 percent of all health care spending. Lowering costs for this limited set of services does nothing to relieve the financial pain of families in insurance plans with high deductibles and co-pays, who are forced to pick up thousands of dollars each year for the ongoing treatment of their chronic conditions.

Moreover, opening the floodgates to more supply is no guarantee that it will lead to lower spending. Jha and Tsai failed to consider what is commonly known as Roemer’s law, named after a Cornell University professor who in the early 1960s pointed out that hospital beds that get built tend to get filled. Studies over many years (most famously through the work at Dartmouth University by Dr. Jack Wennberg and colleagues, who relied on Medicare data) have found that physician and hospital practice patterns are wildly variable across the country, with local supply rising to meet whatever demand that local practitioners generate. This has also been proven true in the broader private insurance market.

Do we really want physician-owners of an gastroenterology ASC encouraging more seniors over 75 to undergo routine colonoscopies? Or more cardiologists recommending under-65 individuals with stable angina to undergo PCI interventions at the catheterization labs they own? A host of new physician-owned hospitals and ASCs could easily lead to more demand and spending, not less.

Even if more competition were to have the desired effect of lowering prices and total spending, it would take years before health care consumers saw any benefit through reduced premiums and co-pays. Busting up monopolies can take up to a decade in the courts. Constructing new facilities can take years. As a political program, it offers no immediate relief to householders struggling now with unaffordable health care bills.

The incrementalist trap

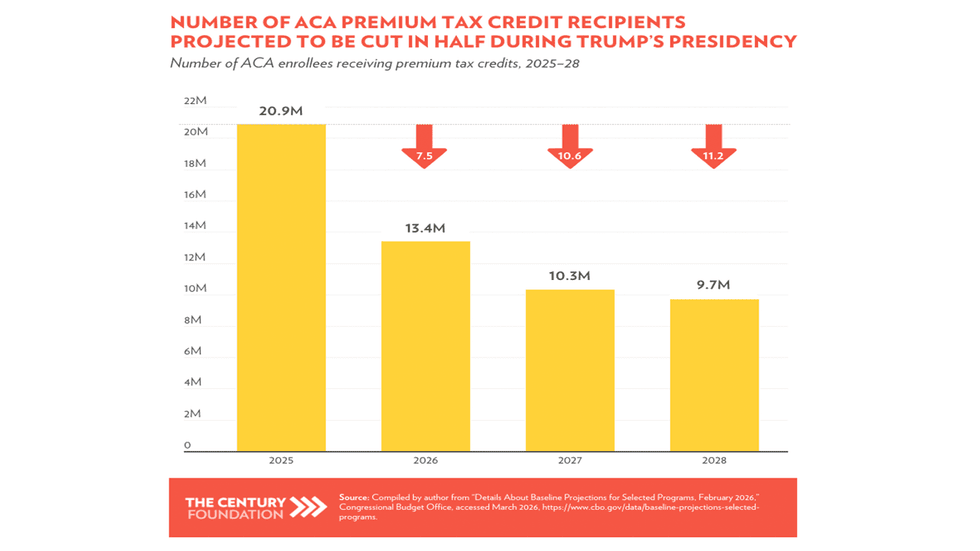

While the Jha/Tsai free market approach may appeal to the corporate wing of the Democratic Party, progressive health care economists, think tanks and patient/consumer advocacy groups continue to pursue incremental approaches to reaching universal coverage, improving benefits and lowering individual and families’ out-of-pocket spending. Their immediate struggle, which polls shows is backed by a clear majority of the electorate, involves fighting to reverse the massive setbacks suffered during the first year of Trump’s second term as president.

The damage will take its biggest toll starting next year unless Democrats win a veto-proof control of both houses of Congress, an unlikely scenario. Their demands are simple: First, restore the enhanced subsidies for Affordable Care Act plans whose expiration has massively increased health insurance costs for the millions of Americans who rely on purchasing individual and family plans on the exchanges. Second, restore the trillion dollars cut from Medicaid and eliminate the bureaucratic roadblocks to meeting the new work requirements and twice-yearly reassessments that will lead to millions of low-income people dropping the coverage they deserve. These advocates and the Democratic party are also fighting at the state level to raise taxes to offset the cuts, assuming, even if there is a blue wave, they won’t win a veto-proof majority.

Yet none of these efforts will have much impact on the half the population who depend on employer-based health insurance, where total costs and employee co-premiums, deductibles and co-pays are soaring. Those 170 million people are seven times more than the 24 million people with exchange-based plans, and 2 ½ times the number of people on Medicaid, all of whom are poor and less affected by rising costs.

This failure to grapple with the cost problem in the private insurance market was evident in a long interview Nobel Prize-winning economist Paul Krugman conducted last month with Jonathan Gruber, the Massachusetts Institute of Technology professor who was one of the main architects of the Affordable Care Act in 2010. They spent nearly half the hour-long interview lamenting the Trump/GOP cuts; condemning under-insurance due to the increasing number of people in high-deductible plans; and the negative health consequences of the escalating level of financial toxicity in the system. Finally, Krugman got around to asking the key question:

“What next? Do you think we can actually move forward and get the system better, besides just restoring the subsidies?”

Replied Gruber: “I think it’s going to be modest changes. I mean, essentially, even if we restore the subsidies, we’ll have 30 million uninsured Americans. Who are they? 10 million are undocumented immigrants. There’s zero political consensus for writing them insurance. About 10 million are people who simply think they’re too healthy to pay for insurance, and without a mandate we’re not going to get them.”

He went on to describe what he suggested will become the next big issue in health care: Providing adequate long-term care and home health for a rapidly aging Baby Boom generation. That will require more immigration, not less, he said, since there aren’t enough native Americans willing to take jobs in these very low-paying but fast-growing fields. “We estimate that you could provide a universal home care program that’s very reasonable for about $40 billion a year, which is really chump change compared to the (Trump) tax cuts,” Gruber said.

Only near the very end of the interview did Gruber switch his focus to the fact Americans pay the highest prices in the world, which is the root cause of the affordability crisis. “The market fails nowhere worse than in health care,” he said, citing Arrow’s paper. “Every other country in the world has recognized that, and they regulate the prices paid in health care. We haven’t. So I think that’s going to be the next big debate,” he said.

But how?

The left-of-center reformers

Dr. Ezekiel Emanuel, a bioethicist/oncologist at the University of Pennslvania and a senior fellow at the Center for American Progress, has the ear of policymakers in the Democratic Party. He recently offered a plan in an op-ed in the Washington Post that would put limits on health care prices in the private sector.

Full disclosure: In 2022, I worked with Emanuel and two others on two Health Affairs articles that explored Maryland’s single-pricing/global budgeting system. We concluded with a recommendation that states adopt the Maryland model, which CMS confirmed in 2021 had saved the federal government more money that all the other alternative payment programs initiated by the agency.

Maryland requires every hospital charge every payer (whether covered by Medicare, Medicaid or private insurance) the same price for the same service, and sets those prices at levels designed to keep spending within a global budget whose growth is limited from year to year. Adopting the Maryland system would lead to higher prices for government payers, who currently pay the lowest prices; and lower prices for private payers, who currently pay the highest prices. It also trims hospitals’ and insurers’ bloated administrative costs since it eliminates the need to negotiate and maintain multiple pricing schedules.

These measures would provide immediate relief to businesses and their employees in the form of reduced premiums and co-premiums. If global budgets were set below the rate of economic growth, the rate of spending growth would slow gradually, giving providers time to adjust while guaranteeing future premium increases would be at or near the overall inflation rate, not two or three times higher as they are now. In the decade since global budgeting was added to to Maryland’s single-pricing system, the state has had one of the slowest growth rates in health care spending in the country.

Unfortunately, Emanuel shied away from comprehensive payment reform in his latest proposal. Instead, he offered a five-point program whose first priority was setting price limits for private health insurance payments at a fixed percentage of Medicare prices. Currently, private prices are about 254 percent of Medicare prices, according to a 2024 survey conducted by the Rand Corporation. “This would reward competition among hospitals and lower bills,” he wrote.

I foresee several roadblocks to adopting a cap on private pricing. First, it will engender massive opposition from hospitals and physician practices, which would see an immediate sharp reduction in total revenue from their best-paying customers. It would not reduce administrative costs since different insurers would still negotiate and maintain different rates under the cap, depending on the number of covered lives they brought to the table. And while capped private prices would immediately lower total premium costs for employers, there’s no guarantee they would share those savings with their employees.

The other four points in the Emanuel program are of interest to policy wonks, but would have little immediate effect on the affordability of current private insurance plans. His proposals include: Paying doctors through bundled payments, not multiple billing codes; equalizing hospital in-patient and out-patient rates, so-called site-neutral payments; increasing spending on primary care; eliminating excess payments to Medicare Advantage plans; forcing insurers to offer the same prices to self-insured employers, whose plans they administer, as they offer to those they fully insure; reforming the pharmacy benefit manager system (already underway in Washington); requiring more rapid adoption of biosimilars; and cutting administrative costs through automating scheduling, quality reporting, data entry and customer service functions.

This is the type of multi-point program that policy wonks love, few people will read and even fewer will understand. It can’t be reduced to a slogan or be summarized in a 240-word social media post that convinces people they will benefit from these incremental and highly technical changes.

Moreover, the program’s only stab at providing immediate relief is setting a cap on deductibles (the amount people must pay in any given year before insurance kicks in) at two percent of the median household income, or about $1,650. While that sounds good, it will be of little solace to the 59 percent of U.S. adults who reported in a survey last year that they couldn’t afford a $1,000 surprise bill. It’s also unfair. A flat cap pegged to the median income provides its greatest benefits to those who earn more and can easily afford the new cap, while it takes a higher share of income from those who earn less. What’s needed is a percentage cap on all out-of-pocket expenses that is pegged to household income. In other words, the cap should be based on each individual household’s ability to pay.

The single-payer abdication

I would be remiss if I didn’t take into account the one-third to two-thirds of the electorate that currently backs single-payer health care, frequently called Medicare for All, as the ultimate solution to the affordability crisis. That wide variation in recent public opinion polls depends on how the question was posed in the surveys.

The Pew Research Center survey of 10,357 adults conducted last November found just 35 percent of favored “a single national health insurance system run by the government.” That same month, Data for Progress, which is affiliated with the Democratic Party-oriented Center for American Progress, asked 1,207 “likely voters” whether they backed “creating a national health insurance program, sometimes called ‘Medicare for All,’ that would cover all Americans and replace most private health insurance plans.” Sixty-five percent offered either “strong support” (36 percent) or “somewhat support” (29 percent).

When the D4P pollsters followed up by asking whether they would still back M4A if it “eliminate(d) most private insurance plans and replace(d) premiums with higher taxes, while guaranteeing health coverage for everyone and eliminating most out-of-pocket costs like co-pays and deductibles,” support fell to 63 percent with those strongly backing M4A falling six percentage points to 30 percent while “somewhat support” rose to 33 percent.

Many Americans, it would seem, so distrust the government that they wish it would keep its “hands off my Medicare” (as the much-lampooned sign at a 2009 South Carolina Town Hall read). Moreover, they begin to back away from supporting M4A as soon as they learn it will lead to higher taxes.

Medicare and Social Security remain the nation’s two most popular social insurance programs, still invulnerable to political attack, and still run by the government. Vermont’s Socialist Senator Bernie Sanders, through his two runs for the Democratic Party presidential nomination, made M4A one of his keystone planks and deserves credit for building a popular base of support for the program, which now commands the votes of over half the party caucus in the House.

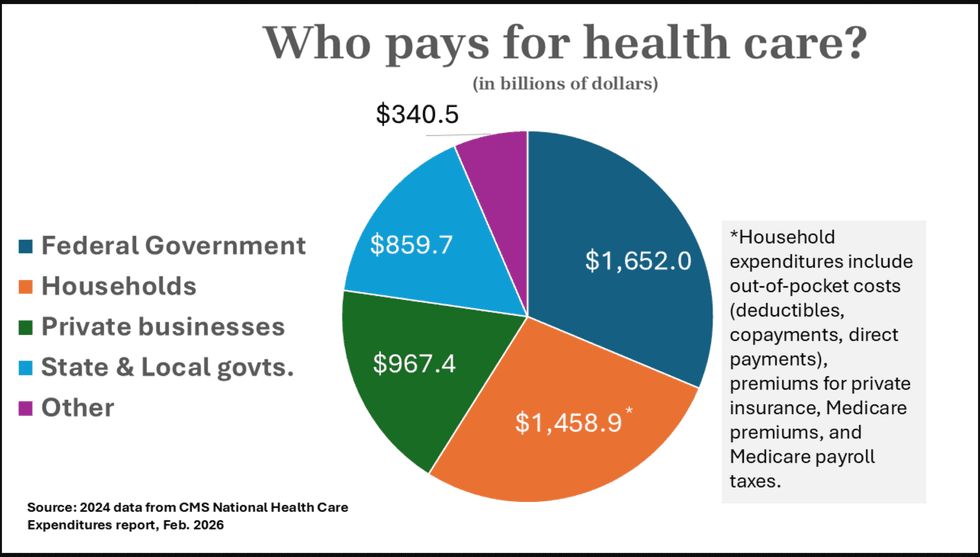

But those Democrats have never developed the tax reform program that would be necessary to implement M4A, at least not one that is capable of unifying the party and winning majority support in Congress. American businesses through private insurance paid for 18 percent of all health care expenditures in 2024, according to the actuaries at CMS. Householders, through co-premiums, deductibles, co-pays, direct payments, Medicare Part B premiums and Medicare payroll taxes, pay for a whopping 28 percent. Relieving businesses of their direct payments and individuals of “most out-of-pocket costs” would require raising somewhere between $1.5 and $2 trillion a year in new revenue. That’s three to four times the amount collected in corporate income taxes in 2024; it’s 75 to 80 percent of individual income tax collections.

Those amounts could be sharply reduced if the legislation enacting M4A left Medicare payments rates where they are today, which average about 40 percent of private insurance rates. But that would entail hospitals, physicians, nursing homes and other providers taking a huge pay cut because patients who were previously insured privately would now be paying Medicare rates. For that reason alone, organized medicine and the hospital associations, whose memberships are located in every state and community in the nation, remain vehemently opposed to M4A, as they have been since it was first proposed by President Harry Truman in 1948. The insurance industry, needless to say, is existentially threatened by M4A, thus presenting a united front of corporate opposition within the health care sector. Their combined political clout has succeeded in keeping M4A off the national agenda, and will for the foreseeable future.

In the past year, M4A advocates have begun focusing on a more limited agenda: rescuing Medicaid, which is now under full scale assault by the Trump administration and the GOP-run Congress. Adam Gaffney, an associate professor at Harvard Medical School and past president of Physicians for a National Health Plan, last month offered an enlightened history of the program’s adoption and evolution in an article in the New York Review of Books.

After reviewing the devastating impact that the $1 trillion in Medicaid cuts will have on beneficiaries (his own research projects 16,000 people will suffer preventable deaths and 1.2 million people will accrue additional medical debt), he turned his attention to the work requirements newly imposed on the program – an extension of the “Elizabethan poor laws tradition of separating the ‘deserving’ from ‘undeserving’ poor.”

It’s been that way since its very beginnings in 1965, when it was tacked onto the legislation creating Medicare. The southern Democrats who controlled key committees in the House, backed by the American Medical Association and other health care lobbying groups, worried Medicare would be an opening wedge for adopting a national single-payer system, with poor people without employer-based coverage being the next group added to the rolls. So they created a separate program that states, “particularly Southern states, could control,” he wrote. “Rightly or wrongly, it was seen as less of a threat to the established, segregated medical order, which treated some people as second-class citizens.”

Over six decades, the 50 state programs have evolved in ways that reflect local choices, with all the biases that entails. Some states are generous, others are punitive; some cover most able-bodied adults, some very few or none at all; 10 states, including most of the deep South, have yet to expand Medicaid under the Affordable Care Act, despite the federal government offering to pay for 90 percent of the cost. Moreover, “Medicaid has also long generally reimbursed providers at a lower rate relative to other insurers, contributing to so-called informal segregation in healthcare provision,” he writes. “Such segregation takes place both across institutions and within them.”

Near the end of his well-written piece, he lays out the political argument for moving to a universal system by quoting Wilbur Cohen, the New Deal-era bureaucrat who stayed in government long enough to shepherd Medicare and Medicaid into existence. “Even as a committed incrementalist, Wilbur Cohen never lost sight of the benefits of universal systems,” he wrote. In a 1972 debate with conservative economist Milton Friedman, Cohen argued the universal case by stating “A program that deals only with the poor will end up being a poor program” since it will lack sufficient public support. For that reason, Cohen argued, “one must try to find a way to link the interests of all classes in these programs.”

Gaffney, like most M4A advocates, is not an incrementalist. He did not call for merging 50 state Medicaid programs into Medicare – something that should have been done in 1965 and still could be done today. Such a merger would generate huge benefits for its clientele in terms of increased access and more comprehensive benefits; it would lead to better pay for safety net providers; and it would provide massive tax relief for the states, who could then devote more resources to education, transportation and public safety — programs that, unlike health care, are best left to local control. The federal taxation required for a Medicaid takeover would be a third of what it would cost to nationalize the entire system. I made the case for federalizing Medicaid in this 2017 article in Democracy: A Journal of Ideas.

As I’ve attempted to show in this review, leading thinkers in and around the Democratic Party are mostly focused on undoing the damage done by the GOP and Trump over the past 14 months. Their proposals for incremental reforms are limited in scope and are unlikely to generate popular enthusiasm in the broader population. They have yet to come up with a comprehensive, achievable program that addresses the immediate affordability issue that is plaguing the majority of Americans, who are in employer-based plans and find themselves absorbing unsustainable increases in their co-premiums, deductibles and co-pays.

In my next post, I plan to revisit my bold proposal to make health care affordable for all, and show why this incrementalist approach is both achievable politically and necessary for putting the U.S. on a path toward a more affordable, higher quality and sustainable health care future.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News