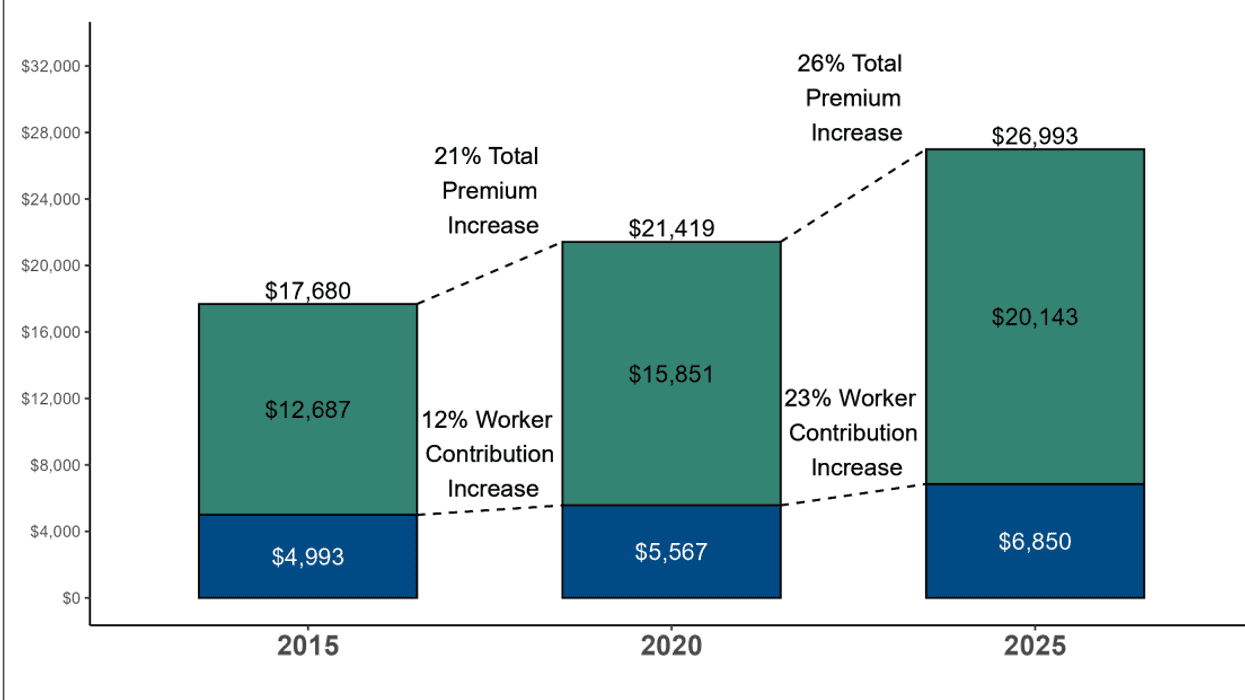

Average Annual Worker and Employer Premium Contributions For Health Coverage 2015, 2020 and 2025

The median cost of employer-based health insurance this year leaped ahead at nearly twice the rate of the consumer price index, according to the annual Kaiser Family Foundation employer survey released yesterday. Sadly, workers are bearing a larger share of the increased burden through rapidly rising co-premiums.

The press coverage this morning of the closely followed survey emphasized the combined top-line increase of 5.5 percent for a family plan, which now stands at a staggering $26,993 a year or about the price of a new compact car. The cost of an employer-based individual plan rose at the slightly lower rate of 4.6 percent to $9,325 a year.

But a deeper dive into the numbers provides a better understanding of why people are so upset about rising health care costs. Employee co-premiums for a family plan (the amount deducted from paychecks) rose 7.6 percent on average to $6,850. The employer share went up only 4.8 percent. The net effect was a downward shift in the share paid by employers and a corresponding upward shift in the share paid by their employees, which was a half percentage point more or 25.4 percent of the total.

This increased burden on workers comes after an eight-year period when the employer share of premiums rose fairly steadily (with a few years off early in the pandemic). Companies offset some of those increases by funneling more of their workers into plans that raised their out-of-pocket expenses for deductibles and co-pays.

Depending on the plan type (HMO, PPO, high-deductible), the average deductible from employer-based family plans now ranges from $3,118 to $5,095 a year. Fully a third of workers and their families enrolled in high-deductible plans for 2025, up from 28 percent the previous year and the most ever.

Put the two together, and the median family (half pay more, half pay less) now pays anywhere from $9,968 to $11,945 a year for health care or close to $1,000 a month. Given the median household income in 2024 stood at $83,730, that translates into anywhere from 12 percent to 14 percent of a typical family’s income.

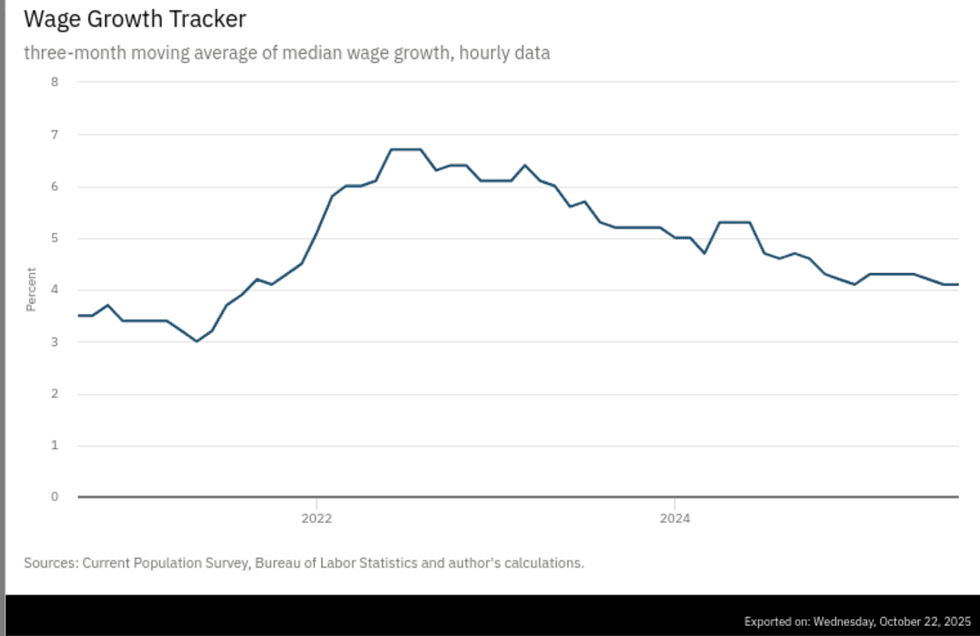

Things are about to get a lot worse. Next year’s premiums and co-premiums for employer-based plans, which cover an estimated 154 million people, are set to rise six percent to seven percent, according to a new survey by Mercer, a health care benefits consulting firm. If the split between employers and their employees remains the same, that will exceed wage increases by two to three percentage points. Wage increases have been trending down for the past three years, falling to just 4.1 percent this past August, the last month reported by the Bureau of Labor Statistics before the government shutdown.

Source: Atlanta Federal Reserve

Source: Atlanta Federal Reserve

No wonder health care costs now ranks as the second most important issue for inflation-weary Americans, just behind the deteriorating state of the overall economy. More than four in five of 1,300 adults surveyed in mid-October by the Associated Press and the NORC Center for Public Affairs said health care issues were extremely or very important to them personally. That was nine percentage points more than crime and 23 percentage points ahead of immigration — the next two biggest concerns.

The impact of ACA/Medicaid cuts on employer plans

The outlook for employer-based plans will also get a lot worse if Democrats fail to restore the Medicaid cuts and the enhanced subsidies for Affordable Care Act plans (which provides affordable insurance for tens of millions of low-wage workers, gig workers and sole proprietors). An estimated 7.3 million people who purchased subsidized exchange plans will drop ACA coverage, with more than half becoming uninsured, according to a Commonwealth Fund brief.

Many will look for cheaper, non-ACA compliant plans that don’t quality for listing on the exchanges because they provide skimpier benefits, are not required to provide free preventive care, can discriminate based on prior medical conditions, and often carry extremely high deductibles and co-pays. This summer, the Trump administration announced it wouldn’t enforce the rule approved by the Biden administration in mid-2024 that limited such plans to three months duration.

“Those who sell non-ACA plans … will absolutely see the coming open enrollment as an opportunity to push their plans as more affordable alternatives, without sharing full information with consumers about the limits of those plans,” said JoAnn Volk, a professor at Georgetown University’s Center on Health Insurance Reforms.

What happens when people who previously had Obamacare buy skimpy plans or become uninsured? They postpone care until their conditions require emergency room treatment — the most expensive place to obtain health care. When struck by serious illnesses like cancer, heart attacks and strokes, they often fail to pay their uncovered bills, or resort to Go Fund Me campaigns to pay off their high deductibles. Some will negotiate long-payoff periods and live the rest of their lives burdened by medical debt. Some will declare bankruptcy.

Hospitals and physicians, in turn, will raise their prices to cover the cost of uncompensated care, which will cause private insurance rates to rise even more. Rising prices, rising insurance premiums, and rising uninsured rates is an accurate description of what existed in the U.S. before passage of the ACA.

These health care economic fundamentals are of little interest to the modern-day Republican Party, which invariably includes some variation of bare-bones insurance as one of their answers to the affordability crisis. Early in the shutdown, they floated ideas like instituting new income caps on Obamacare subsidies, establishing minimum co-pays, and cutting off subsidies for new enrollees, none of which they would agree to negotiate until the government is reopened.

Then, last week, Politico reported they are also willing to beef up tax credits for investing in health savings accounts, which could be used to buy skimpy plans. Lower-income workers generally avoid HSAs since they can’t afford the voluntary deductions needed to fund them.

I can’t predict when or how the shutdown crisis will end. But I am pretty confident that I know what will happen to health care costs in the next few years given Republican control of Washington. They’re going up, up, and up.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News

- Federal Judge Angrily Orders Trump To Restore Health Agency Websites ›

- 'On Vacation': Jeffries Scorches GOP Leaders For Fleeing Town During Shutdown ›

- A Decent Slice: The Affordability Crisis Isn't Only About Prices - National Memo ›

- Facing 2026 Blowout, Trump Blinks On Obamacare Subsidies --Yet Still Aims To Gut Program - National Memo ›

- Pushing Back: A Bold Plan To Make American Health Care Truly 'Affordable' - National Memo ›

- Yes, The Fed Should Lower Interest Rates (Because Trump Is Wrong On The Economy) - National Memo ›

- With Looming Implosion, Health Care Reform Could Dominate 2026 Elections - National Memo ›

- Gallup Poll: Public Satisfaction With Health Care Costs Hits New Low - National Memo ›

- Why Democrats Must Bring A Fresh VisionTo Debate Over Health Care - National Memo ›

- Erupting Crisis Of Uninsurance, Created By Republicans, Will Soon Engulf US Families - National Memo ›

- Global Perspective on U.S. Health Care | Commonwealth Fund ›

- A Crisis in the Health System and Quality of Healthcare in ... ›

- The Relation of the Chronic Disease Epidemic to the Health Care ... ›

- The Republican Health Care Crisis: Higher Costs, Less Coverage ... ›

- Americans' Challenges with Health Care Costs | KFF ›