Here’s the good news. The Democratic Party’s demand that Congress extend the Affordable Care Act premium subsidies in exchange for helping end the government shutdown is fracturing the GOP monolith.

In recent social media posts, Rep. Majorie Taylor Greene (R-GA) articulated what every legislator on the GOP side of the aisle knows but won’t admit. Out-of-pocket costs for ACA plans will skyrocket next year if the enhanced subsidies passed by the Biden administration during the pandemic are allowed to expire.

“This is a major crisis in America,” she said this week on NewsNation, a conservative cable news network. “We’re looking at a massive spike in health premiums. It’s going to crush people. They’re going to have to drop their health insurance. That will put a lot of people in danger of becoming bankrupt with health care bills, with hospital bills,” she said.

Even Donald Trump, ever the prevaricator, has begun toying publicly with opening negotiations with Democrats after Greene made her comments.

But she went further. It is not just the 24 million people on ACA plans who will get hit hard with average premiums more than doubling to more than $1900 a month (before subsidies) without the enhanced premium subsidies. “People with regular or private plans, their premiums are looking to go up a median of 18 percent. That’s brutal,” she said.

Always fast and loose with her facts, Greene’s claim that private health plan premiums will rise 18% is more than double what employer benefits consultants are predicting. But there’s no doubt huge spikes in employer premiums and employee co-premiums are coming. Both will likely to see near double-digit increases.

That’s the issue I want to address in today’s post because it represents a messaging minefield for Democrats, even if they win an extension of the ACA plan subsidies.

Where’s the rest of us?

During September, there was an interesting debate within the Democratic Party about what to demand from the GOP majority before giving them the votes needed to keep the government running beyond September 30th. Progressives wanted to focus on limiting the Trump regime’s flagrant violations of the law and constitution. Centrists, led by Senate Minority Leader Chuck Schumer (D-NY) and House Minority Leader Hakeem Jeffries (D-NY), preferred putting health care — usually a winning issue for Democrats — front and center. The centrist majority won the day.

The political wisdom of the leaders’ decision now seems vindicated. As Jonathan Cohn wrote yesterday in The Bulwark (his post was headlined “The Democrats Are Winning the Shutdown Fight”):

“A big premium spike can be a political nightmare for the party in charge, as anybody who lived through the Obamacare rollout can attest. That’s the whole reason Republicans seem so uncertain about their current position—and why now even MAGA stalwarts like Greene are suggesting Republicans sign on to an extension. If nothing else, that would seem to give Democrats leverage to demand even more…

“Democrats actually do care passionately about making health care more affordable. If the subsidy boost lapses, the higher costs will mean real hardship for many millions, and 4 million more Americans with no insurance at all. Extending the subsidy boost would prevent most or all of that from happening. And insofar as Republicans are bound to support some kind of extension eventually—precisely because the blowback to the spike could be so strong—forcing a deal now, in this high-profile debate, would allow Democrats to claim (legitimately) it was their doing.”

Nowhere in his lengthy article did Cohn discuss the employer-based insurance market, which covers 164 million working Americans and their families. If the Democrats say nothing about their looming health care cost increases, it will be a huge mistake.

Should Democrats win on the ACA issue, it will no doubt be great news for the 24 million Americans whose health insurance comes through plans sold on the exchanges. Just seven percent or about 1.7 million purchasers pay the full cost of their plans. The rest receive subsidies based on income that limit their out-of-pocket premiums. The lowest wage workers pay nothing at all.

For most, the total cost of the plan is irrelevant. The federal government picks up most if not all of any increase in the total cost of the plan.

But that won’t be true for the far larger employer-based insurance market — the half of all Americans whose health plans come through an employer, group or union. Their plans receive no direct subsidy. The employer share — on average about 75 percent of a family plan — is tax deductible as is any employee premium, usually deducted from paychecks. But the employee share paid through co-pays and deductibles is not unless their medical expenses exceed 7.5 percent of adjusted gross income; they itemize deductions; and their total deductions exceed the standard deduction. Even then, the deduction is only the amount over 7.5 percent of AGI.

Both employers and employees will bear the full upfront cost of the expected large increases in premiums on tap for next year. A month ago, Mercer, a leading benefits consulting firm, projected average employer premiums could rise nine percent next year based on preliminary results from its annual survey of nearly 2,000 employers. It predicted actual increases would be closer to 6.5 percent because of steps employers will take to hold those costs in check. That’s still twice the overall inflation rate.

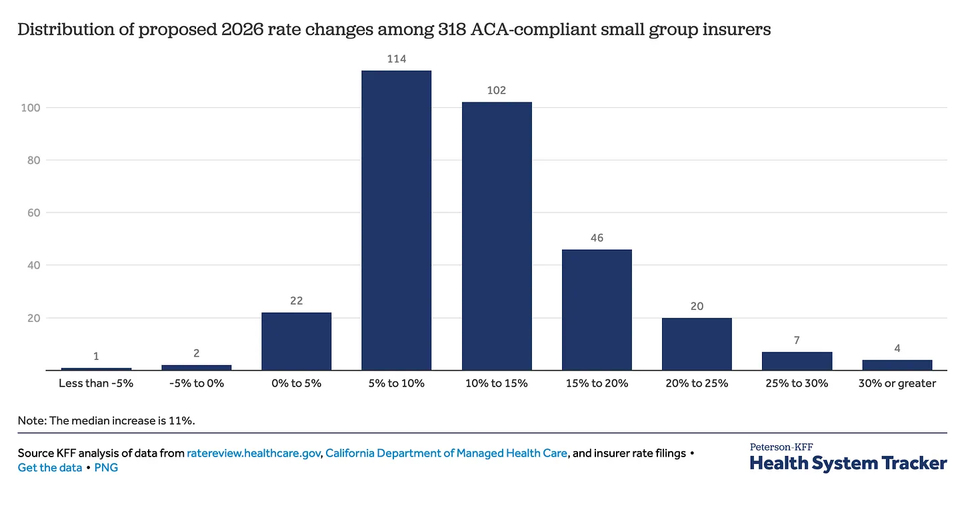

Smaller employers will be hit hardest of all. A recent issue brief from the Kaiser Family Foundation found the median proposed premium increase for 318 small group insurers who offer ACA-compliant plans was 11 percent.

What’s behind rising costs?

Mercer health research director Beth Umland cited the usual suspects for the biggest increase in health care costs since 2010: The high cost of cancer treatments and weight-loss drugs; higher-than-usual price increases enabled by provider consolidation; higher health care worker wages driven by rising inflation in the general economy; and the “buildout of AI-based platforms that help providers optimize billing.”

The KFF brief echoed that analysis. It cited higher prescription drug costs and utilization, rising labor expenses, and overall economic inflation. “Some insurers also note declining enrollment and worsening risk pool morbidity as factors leading to higher projected costs next year,” the brief said.

The daily news in the health care trade press is filled with stories of insurers and providers battling over who should be forced to absorb some of those rising costs. Insurers are increasingly resorting to the “just say no” form of prior authorization and receiving pushback from both providers and patients. Modern Healthcare (where I used to be editor) reported this morning that insurers Aetna and Cigna are imposing their own version of the two-midnight rule (don’t ask) by forcing hospitals to accept out-patient rates for emergency room visits deemed routine care, no matter how long they stay in the hospital.

There’s going to be a lot more of those ER visits next year should the ACA subsidies not be extended, since an estimated four million people are expected to drop coverage. That will force many folks to use hospital ERs instead of primary care physician practices for their routine care. And, given that those dropping coverage will be fairly low income, most will postpone or fail to pay those ER bills, which leads to higher prices for everyone else who uses hospital services. Hospitals invariably raise prices to make up for uncompensated care.

And how will employers mitigate some of those rising costs (thus whittling the expected nine percent increase down to 6.5 percent), according to Mercer? “The survey found that 59 percent of employers will make cost-cutting changes to their plans in 2026 — up from 48 percent making changes in 2025 and 44 percent in 2024,” Umland wrote. “Generally, these involve raising deductibles and other cost-sharing provisions, which can lead to higher out-of-pocket costs for plan members when they seek care.”

In other words, workers will see their out-of-pocket co-pays and deductibles rise sharply in addition to a 6.5% average increase in their co-premiums, which are taken directly out of their paychecks. Workers with chronic health care needs could see their annual medical expenses rise at three times the overall inflation rate — perhaps even into double digits.

Only a tiny share of those increased costs will be mitigated by a Democratic win on ACA subsidies. Nor will a win do anything to help the millions of people who will be thrown off Medicaid, whose uncompensated expenses when they also show up in ERs for routine care will also be reflected in higher private employer/employee insurance bills.

For a majority of Americans, any Democratic Party claim that they “saved” health care by their strong stance during the shutdown negotiations will ring hollow in the face of their still rising out-of-pocket expenses.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News

- Report: Trump Sent Mullin To Deal With Democrats As Shutdown Spooks GOP ›

- Medicaid Cuts Loom As House Republicans Declare War On Red States ›

- Breaking With GOP, Greene Demands Extension Of Obamacare Subsidies ›

- CBO Report: Trump's Big Ugly Bill Robs The Poor To Grease The Rich ›

- Why Are Fox Hosts So Eager To Jack Up Americans' Health Care Costs? ›

- Trump Van Winkle, Obamacare And The 'Money-Sucking' Health Insurance Industry - National Memo ›

- Despite Frustrating End, Democrats Can Still Build A Victory From 40-Day Shutdown - National Memo ›

- A Decent Slice: The Affordability Crisis Isn't Only About Prices - National Memo ›

- As Health Insurance Premiums Spike, Inequality Worsens -- But There Is A Solution - National Memo ›

- Facing 2026 Blowout, Trump Blinks On Obamacare Subsidies --Yet Still Aims To Gut Program - National Memo ›

- Pushing Back: A Bold Plan To Make American Health Care Truly 'Affordable' - National Memo ›

- With Looming Implosion, Health Care Reform Could Dominate 2026 Elections - National Memo ›

- Gallup Poll: Public Satisfaction With Health Care Costs Hits New Low - National Memo ›

- Health Insurance Premiums Are Set To Soar Just Before Midterm Elections - National Memo ›