Health Inflation Won't Stabilize Until Politicians Confront Monopoly Hospitals

Today’s inflation report is a wake-up call for wannabe-be health care reformers. It provides the perfect opening for injecting how to control hospital prices into this year’s political debate.

The overall inflation rate ratcheted up 4.2% last month, driven largely by fast-rising gasoline and diesel prices that are entirely due to Trump’s ill-conceived, undeclared and unwinnable war against Iran. If you take out food and energy, inflation was up “only” 2.9%. That’s still nearly a full percentage point above the Federal Reserve Board’s target level.

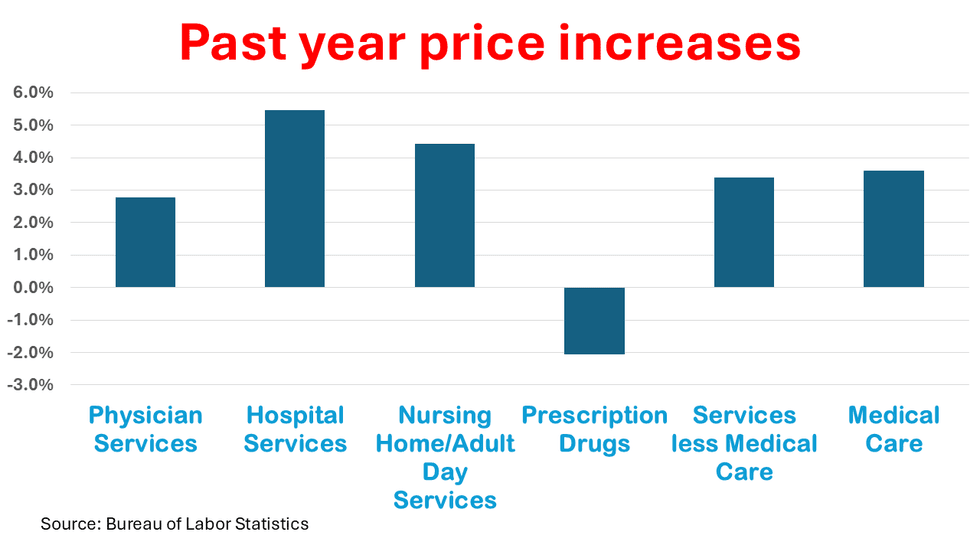

But dig a little deeper into the numbers and you find medical inflation, which many Americans consider their most pressing concern, rose 3.6% over a year ago, faster than the core inflation rate. Prices for hospital services were almost entirely responsible for the jump — up 5.7% year over year.

The second largest component of health care services — physician fees — grew at a much slower pace, up 2.8% or about the same rate as core inflation. Drug prices fell 2.1% over the past year.

The drug price component of the consumer price index is somewhat misleading since the Bureau of Labor Statistics measures the change in existing drugs and generics, not the price of new drugs coming to market. Big Pharma introductory prices for new drugs like the popular GLP-1s have reached sky-high levels, which often come down somewhat after launch to attract more customers.

Novo Nordisk’s Wegovy, for instance, came to market at $1,349 a month, but now can be purchased for as little as $350 a month. That shows up as a major price decline in the index, even though many consumers still can’t afford it because their insurance companies won’t pay for it.

Speaking of insurance companies, the New York Times reports their prices fell 6.4% over the past year, which is hard to understand given the rising prices for almost all of the services they finance with the premiums collected from employers and consumers. I also don’t know where the Times got that data since I couldn’t find it in either the Bureau of Labor Statistics press release or the agency’s detailed data tables.

I suspect at least some of the decline in health insurance prices reflects what individuals pay for plans sold on the exchanges, where millions of people are switching to bronze plans from pricier silver plans to lower their upfront premiums. Unfortunately, when they use their insurance, they will have much higher out-of-pocket costs.

This isn’t a price decline. It’s a cost-shift. I suspect some health care economists will insist cost-shifting doesn’t exist, claiming it reflects consumer preference for the cheaper item.

None of this is good news for the nation’s hospital leaders, who have launched a major media campaign to shift the blame for rising health care prices onto health care’s other special interests. The American Hospital Association’s March report “The Cost of Care” blamed the surging cost of drugs, labor and supplies for their price increases.

Some of that is true, but the document offers a classic inside-the-beltway manipulation of data to make its case. The AHA report used a consulting firm’s data to show that “advertised salaries for registered nurses have grown 26.6% faster than the rate of inflation over the past four years. These increases are essential to maintain staffing levels but also contribute to the overall financial challenges hospitals face.”

Let’s take a closer look at that claim. The cumulative inflation rate between May 2022 and May 2026 was 13.8%, an average of about 3% a year before compounding. A 26.6% increase brings that to 17.5% over four years, or an average of about 4% before compounding. If anything, the AHAs data shows nurse wages have gone up about a percentage point faster each year than underlying inflation, which is what you might expect from a sector of the economy with a large union membership. Hospital prices, on the other hand, have gone up about two to three percentage points faster than inflation.

Higher wages for nurses can actually be a good thing for hospitals, which frequently hire traveling nurses to staff unexpected surges in patient load or temporarily fill open positions. The staffing firms that provide those nurses (like publicly-traded AMN Healthcare) impose huge mark-ups on the underlying nurse salaries, which make their cost considerably higher than hiring permanent staff. The same is true for many of the support staff occupations inside hospitals. If hospitals paid adequate wages and provided decent working conditions for their permanent staff, perhaps they wouldn’t have to rely on high-priced staffing firms to keep their facilities running.

Meanwhile, the House Energy and Commerce Committee today held a hearing on Capitol Hill to promote greater hospital and insurance company price transparency, an issue for which there is bipartisan support. The assumption is that greater transparency will promote competition and allow health care “consumers” to shop.

This ignores the economic realities of health care. First, only a small portion of health care services are shoppable. Second, there is little or no competition in most markets. Third, even where competition exists, most patients are locked into networks and hospital systems that offer a closed loop of primary care and specialty physician providers. More than half of all doctors in the country now work for either hospitals or insurance companies.

“The monopolization with regard to hospitals and so many health care interests exists and is getting worse,” Rep. Frank Pallone Jr. (D-NJ), the ranking member of the committee, said in his opening statement. “So, let’s not forget that … to use transparency more effectively …, we have to also look at the competitive environment to make sure it truly is competitive.”

I’m not holding my breath for Republicans to endorse greater antitrust enforcement. But it is disappointing that Democratic leaders are putting all their marbles on competition policy to bring down hospital prices, which under the best of circumstances will take years of court battles to bring results.

I didn’t get a chance to listen to the hearing today, but I bet not a word was said about putting hospitals on budgets, putting physicians on salaries and giving administrators the freedom to deploy their financial resources in ways that deliver better health outcomes. The American people are ready for meaningful change. So far, such proposals are missing from this year’s health care debate as we head into the mid-term election season.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News

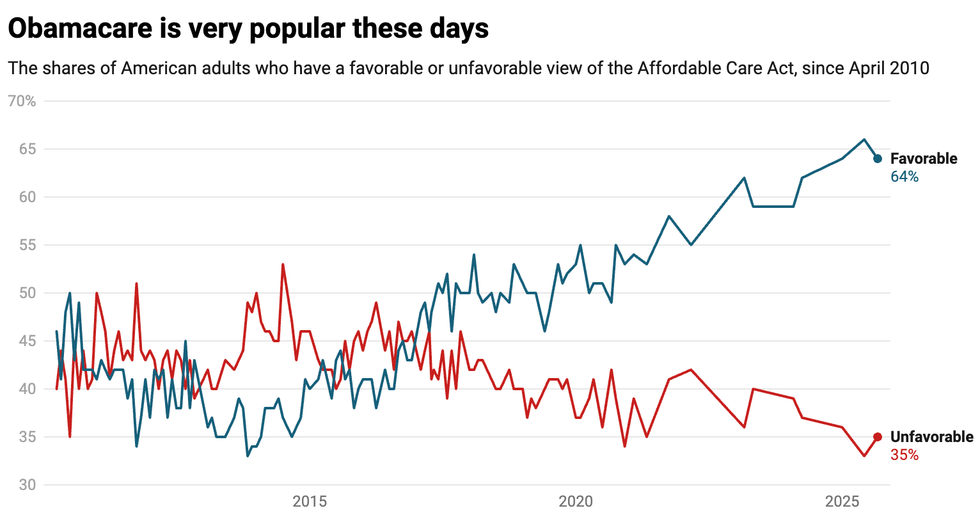

Respondents who answered "Don't know" are excluded.Chart: Andrew ManganSource:

Respondents who answered "Don't know" are excluded.Chart: Andrew ManganSource:

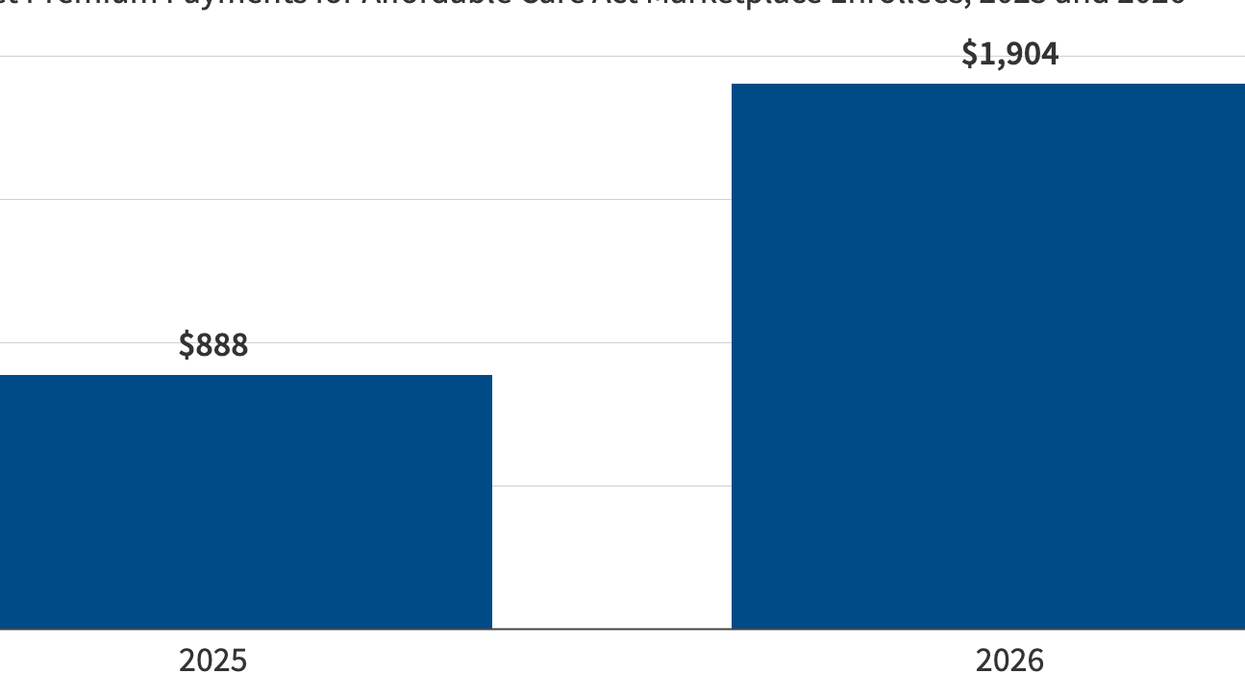

Source: Kaiser Family Foundation

Source: Kaiser Family Foundation