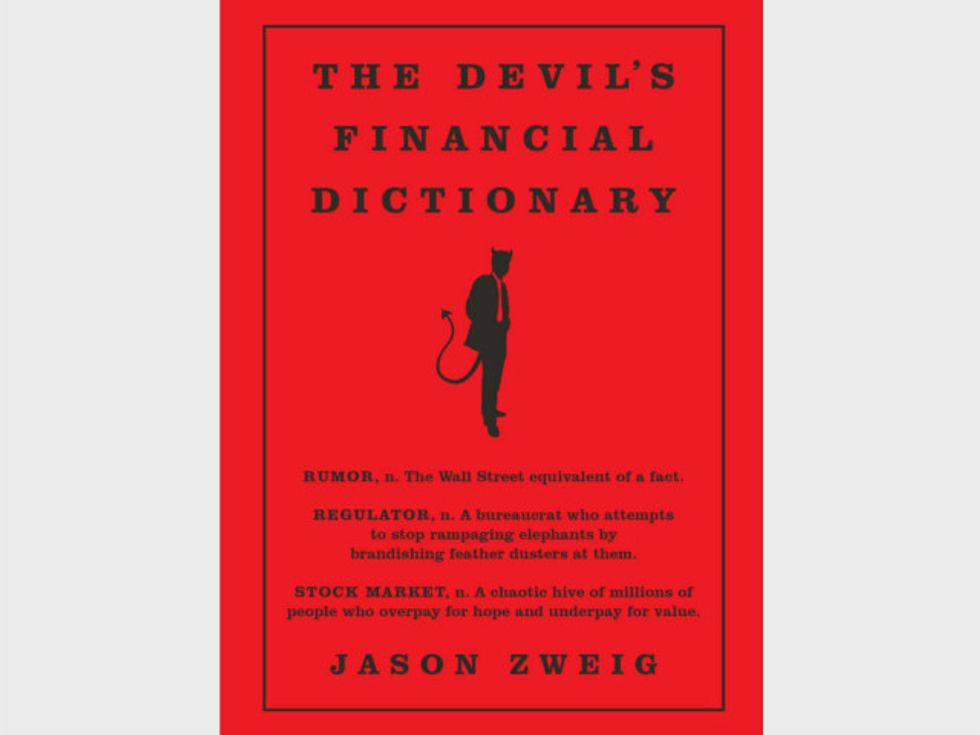

‘The Devil’s Financial Dictionary’ Cuts Through The Euphemism, Doublespeak, And Lies Of Wall Street

One of the defining characteristics of the financial crisis of 2008-2009 was that Wall Street’s gains were privatized while its risks were socialized: The CEOs and other top executives at banks and brokerages pocketed billions of dollars’ worth of bonuses for themselves, while taxpayers subsidized the losses after the same financial firms collapsed and had to be bailed out by the government. More recently, Wall Street would have you believe that you are better off being “advised” by stockbrokers who will put their own interests ahead of yours, that fund managers who have failed to protect their investors against losses in the past will do so in the future and that conflicts of interest can harm you only if you don’t know about them.

The great American satirist Ambrose Bierce wrote his Devil’s Dictionary (first published in 1906) to mock the pretension and hypocrisy of the Gilded Age. I started writing what became The Devil’s Financial Dictionary merely to amuse myself, but soon realized that it could be a vehicle to mock the pretension and hypocrisy of our own, latter-day Gilded Age. The financial industry abounds in euphemism, doublespeak, myth and mendacity. With this book, I seek to offer a glossary of what lies beneath.

—

APOLOGY, n. In the real world, an admission of culpability and remorse for an action that harmed someone else, typically followed by an attempt to right the wrong and a commitment not to repeat it; on Wall Street, a declaration that other people did something wrong and that any resulting harm was caused by circumstances beyond the bank’s control. A Wall Street apology always purports to take responsibility, but usually omits contrition, shame, a desire to make good on what went bad, or the willingness to make sure the same behavior never happens again.

In testimony at congressional hearings today, Manuel B. Schacht, chief executive of Bellow, Blair, Howell, Huff & Bragg, the investment bank, apologized for the $794 billion in losses his firm incurred on securities backed by the value of beachfront property in the Central African Republic. “I accept full responsibility for what happened, and as a firm we deeply regret the inconvenience that investors and taxpayers have experienced,” said Mr. Schacht.

He added: “The worst of the suffering, however, will be borne by our own employees, who must forgo their future bonuses and search for work elsewhere while bearing the stigma now so unfairly attached to our firm. It is important for policymakers and the public to recognize that, while mistakes were made, these losses were triggered by events beyond our control.”

BEAR MARKET, n. A phase of falling prices when you can no longer bear to think about what a fool you were for not selling your investments—which is generally a sign that you should think instead about buying more. A period of falling prices inevitably sets the stage for a period of rising prices. See also BULL MARKET.

A bear market is commonly believed to begin when a stock-market average or index has fallen by at least 20 percent. But, in fact, there is no official definition or threshold—still another reminder that reality on Wall Street is just a state of mind.

BIASED, adj. Human.

BULL MARKET, n. A period of rising prices that leads many investors to believe that their IQ has risen at least as much as the market value of their portfolios. After the inevitable fall in prices, they will learn that both increases were temporary. See BEAR MARKET.

BUY, v. What Wall Street analysts say investors should almost always do, regardless of a stock’s price or market conditions. See also SELL.

CLEARLY, adv. Unclearly.

Analysts and pundits using the word “clearly” are either (1) pretending, without any valid evidence, that they know what is going to happen, or (2) describing what has already happened and declaring, after the fact, that they knew it would happen when at the time they had no idea (see HINDSIGHT BIAS).

CREDIT CARD, n. A thin slab of plastic that enables a person to feel pleasure today by incurring pain tomorrow.

DATA, n. The raw material from which Wall Street fabricates distortions for marketing purposes.

DAY TRADER, n. See IDIOT.

DODD-FRANK ACT, n. A financial-regulation law, enacted in 2010, that sought to prevent financial institutions from becoming “too big to fail” but succeeded mainly at being too long to read, too complex to understand, and too convoluted to implement.

POTENTIAL CONFLICT OF INTEREST, n. An actual conflict of interest.

REGULATOR, n. A bureaucrat who attempts to stop rampaging elephants by brandishing feather-dusters at them. Also, a future employee of a bank, hedge fund, brokerage, investment-management firm, or financial lobbying organization.

RUMOR, n. The Wall Street equivalent of a fact.

SELL, v. What Wall Street analysts say investors should almost never do, regardless of a stock’s price or market conditions. See also BUY.

—

Excerpted from The Devil’s Financial Dictionary by Jason Zweig. Reprinted with permission from PublicAffairs. Copyright © 2015 Jason Zweig. All rights reserved.