Fresh Warnings In The Government's First-Quarter Economic Report

There was a lot of news in the GDP report yesterday, in addition to the data from the day’s other releases. It took a little while to percolate, but here are my five major items:

1) GDP growth is worse than it looks;

2) Consumption is unbalanced and weak;

3) Inflation is worse than it looks;

4) The factory construction boom is going into reverse; and

5) There is no evidence of an AI productivity boom. (Our jobs are safe!)

I’ll deal with these in turn.

GDP Growth Was Driven by a Jump in Federal Government Spending

Spending by the federal government fell at a 16.6 percent annual rate in the fourth quarter of 2025. This was partly driven by the DOGE layoffs, most of which first took effect in the fourth quarter. However, it was also partly driven by the government shutdown at the start of the quarter, which continued until the middle of November. The contraction from the DOGE cuts is not being reversed, but the contraction from the shutdown was reversed. This explains the 9.3 percent growth in federal spending, which added 0.56 percentage points (PP) to growth for the quarter.

Pulling out federal spending, GDP growth was around 1.5 percent. That’s not disastrous, but not something to write home about.

It is common for economists to look at the growth in final sales to domestic producers as a sort of “core” GDP. This strips out the growth (or shrinkage) from inventories and net exports.

This is an especially bad approach to the first quarter data. The big jump in federal spending gets counted in the core even though absolutely no one expects it to continue. (Actually, the Iran War may sustain growth in spending, but that is a bit out of the ordinary.) In the fourth quarter, the reduction in federal government spending reduced the growth rate by 1.16 PP, which was the main reason for the weak 0.5 percent growth rate reported for the quarter. The move to a core measure would not have changed that picture.

The other problem with the core measure is that the imports it strips out directly contribute to the investment growth it counts. Computer investment rose at a 64.7 percent annual rate, while investment in software increased at a 22.6 percent rate, contributing 0.58 PP and 0.51 PP, respectively, to the quarter’s growth. This is the data center boom.

However, many of the items being picked up by this growth are imported. If there is a comparable rise in investment in the second quarter, there will be a comparable increase in the trade deficit. It doesn’t make sense to count the positive but not the negative. The direct effect of imports is to grow other countries’ economies, not ours. (Yes, the indirect effect is positive, but that’s not the question here.)

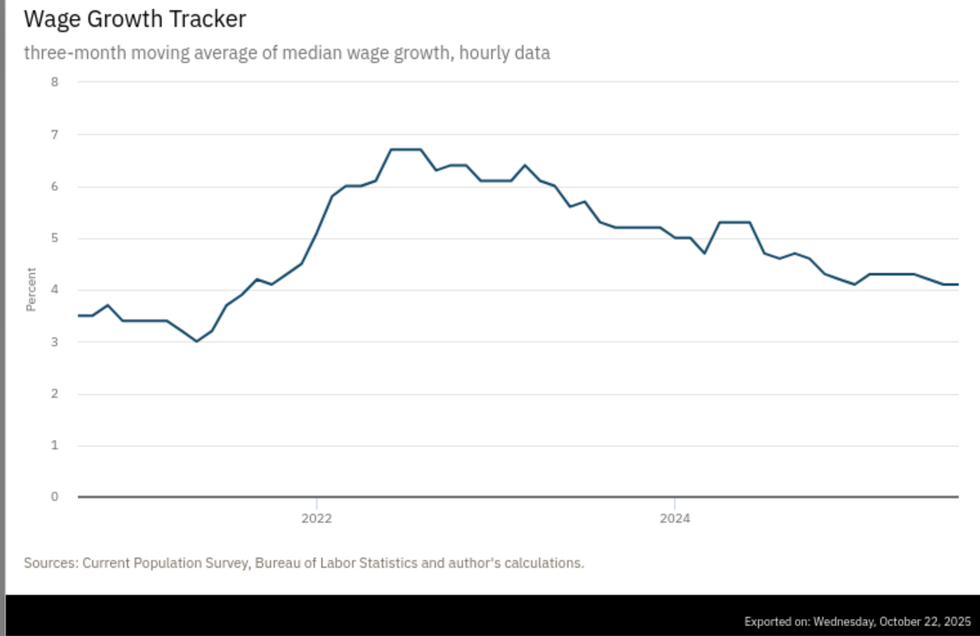

Consumption Growth Was Driven by Healthcare Spending

Consumption grew at a 1.6 percent annual rate in the quarter, which is fine, even if on the slow side. But the troubling part is the composition. Healthcare spending accounted for 47 percent of the increase in consumption, while financial services accounted for another 24 percent, leaving less than 30 percent for everything else.

Durable goods consumption was barely positive. It was only kept above zero by a surge in March car purchases, possibly by people trying to get ahead of price increases. Non-durable goods consumption actually fell slightly.

The pattern here is that most areas where consumption might be seen as discretionary, like recreational vehicles, hotels, and restaurants, had declines in real spending. That is not a good story.

The Jump in Inflation was Not Just Driven by the War

We all know that the shutting of the Strait of Hormuz sent oil and gas prices soaring. This is a big factor in first quarter inflation, but far from the whole story.

Inflation was picking up even before the start of the war. The PCE deflator rose 0.3 percent in January and 0.4 percent in February. The core deflator rose 0.4 percent in both months. This pace is far above the Fed’s 2.0 percenttarget. March was considerably worse, with the overall rate rising 0.7 percent for the month. The annual rate for the quarter as a whole was 4.5 percent, the highest since the third quarter of 2022.

If the war ends quickly and the Strait is reopened, oil and gas prices will head back down, but according to the analyses I have seen, it will take much longer going down than going up. And many of the negative effects from the closing, like the shortage of fertilizer for planting, won’t be seen for months down the road.

It is also important to note that the data center boom is causing considerable inflation in other areas. The annual rate of inflation in computers and related equipment was 18.5 percent in the first quarter. This is likely to increase if the AI bubble continues to grow.

Factory Construction is Going Down Fast

There was an unprecedented boom in factory construction in the recovery from the pandemic. At its peak in 2024, real construction was going on at more than twice the pre-pandemic pace.

This has gone in reverse, and the decline is accelerating. Factory construction fell at a 22.7 percent rate in the quarter and is now down 21.7 percent from its peak in the third quarter of 2024. At the first quarter pace, we will be back to the pre-pandemic rate of factory construction in a year and a half.

No Evidence of an AI-Driven Productivity Boom

While the media are filled with stories about AI taking all the jobs, the data apparently have not gotten the message yet. Value-added in the non-farm business sector, where productivity is best measured, grew at a 1.5 percent annual rate. It looks as though hours will be close to flat for the quarter, although data revisions could change this story.

That would imply a 1.5 percent rate of productivity growth. That’s not a bad rate, but it’s down some from last year’s 2.5 percent. Everyone should know that the quarterly productivity data are highly erratic and subject to large revisions, but it’s safe to say that AI does not seem to be taking all the jobs just yet. Maybe we will have a different story next quarter.

War Is the Big Uncertainty

The economy was not looking great going into the war. To be clear, we were not looking at a recession or runaway inflation, but we were seeing weak growth, modest real wage growth, and at least moderately accelerating inflation. The war is making the inflation picture worse, and the longer it goes on, the worse the picture gets.

The additional military spending will provide a boost to growth, but it is not the sort of boost that anyone would want, other than military contractors. A quick peace deal will lessen the damage but will not make it all go away.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.

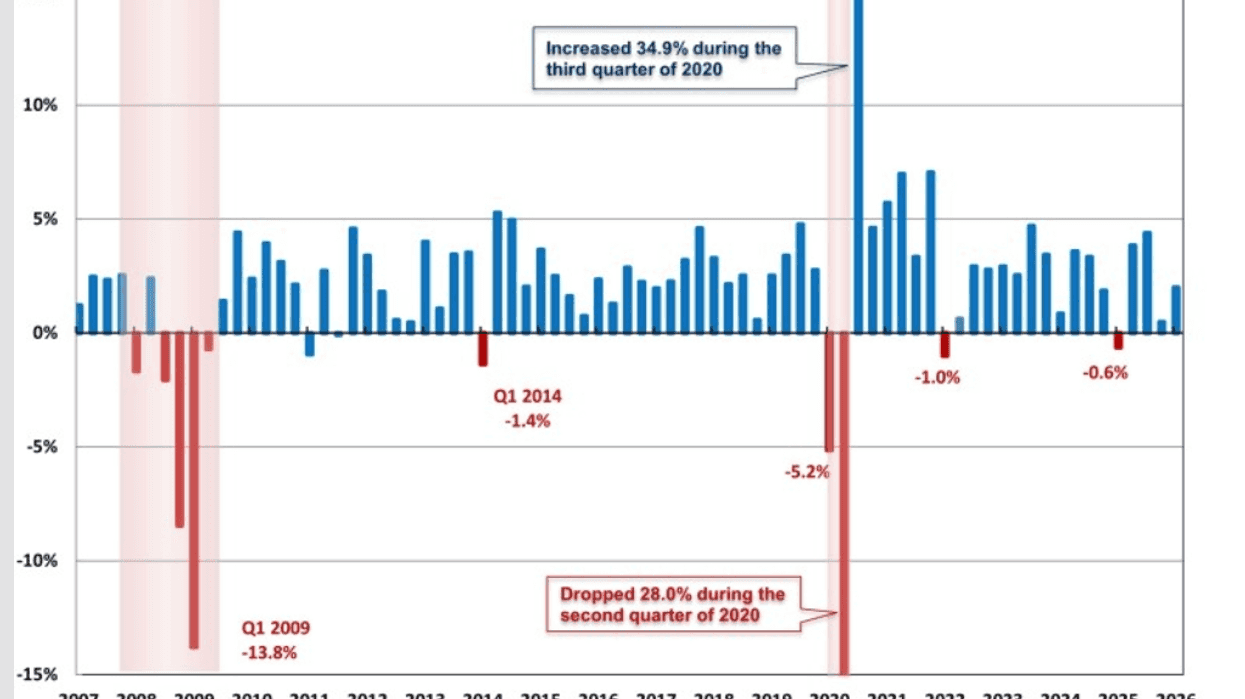

Source: Atlanta Federal Reserve

Source: Atlanta Federal Reserve