'The Ideas Are There': Shutdown End Signals Renewed GOP Assault On Health Care

First they came for the federal employees. Then they slashed food stamps. And now that the Democrats have surrendered in their fight to preserve expanded Affordable Care Act subsidies and Medicaid funding, expect to see a full-blown attempt by the GOP to gut the individual market in December.

Fresh off their overwhelming victories in last week’s off-year elections, a handful of Democratic centrists decided the possibility of delayed Thanksgiving travel plans was the bridge too far when it comes to protecting millions of people from losing their health insurance.

I put the odds of the Democrats winning concessions in the promised December negotiations — if they actually take place — at about five percent. Why would the Trump-owned GOP agree to even a one-year extension of expanded subsidies when they are planning to offer their own plans for “lowering premiums” during next year’s mid-term election campaigns?

This morning’s Modern Healthcare reports GOP leaders are planning to reintroduce many of the same policies they floated but failed to pass in their many efforts to repeal Obamacare during Trump’s first term in office. They include rejiggering the original ACA subsidies so that people buying plans on the exchanges pay lower premiums but have higher co-pays and deductibles.

Also under consideration is expanding the amount of money people can put into health savings accounts to defray their out-of-pocket expenses. This is meaningless for most lower-wage workers — the ones hurt most when thrown into high-deductible plans. They can’t afford to take money out of their paychecks to put into a health care rainy day fund. Such policies are a gift to the well-insured upper middle class, not people in the bottom half of the wage distribution.

GOP efforts to pose as defenders of health care will also include a push to eliminate restrictions on short-term plans, which the Biden administration had limited to three-months duration. Such plans, which have none of the guaranteed coverage or cost controls included in ACA plans, were originally conceived as a bridge for people between jobs.

The Trump administration announced in August it wouldn’t enforce the Biden rule. At the time, it said it plans to promulgate new rules giving such plans a one-year duration and allow people to stay on them for three consecutive years. Passing a law would get that job done more quickly.

They also want to bring back association plans, where industry, religious, or other groups can set up cooperative insurance schemes that meet none of the consumer protections in the ACA. Those include guaranteed issue (where you can’t be denied coverage if you have an existing medical condition); caps on out-of-pocket expenses; and requirements that plans offer benefits deemed essential like mental health and substance abuse treatment; pregnancy, maternity and newborn care; and preventive and wellness services.

A suite of changes like that will give young, healthy workers without employer-based coverage numerous low-cost options that enable them to bypass the exchanges when seeking coverage. Brokers will gladly push such plans since they make huge and repeated commissions through their sale. This will drain the insurance pool of healthy workers, leave behind a sicker insurance pool, and thus raise premiums for everyone who needs more comprehensive insurance.

“We have discussions ongoing right now, and I think for any side to say the Republicans don’t have ideas for healthcare reform is to forget what we went through and almost got done,” House Education and Workforce Committee Chair Tim Walberg (R-MI) told Modern Healthcare in an interview. “The ideas are there.” (Editor's note: Another Walberg idea was launching nuclear strikes in Gaza to "get it over quick.")

And they’re moving to enact them. The Senate Homeland Security and Government Affairs Committee held a hearing last week to discuss a new insurance pool that would provide catastrophic health coverage for skimpy individual plans sold outside the exchanges. Numerous states tried this prior to passage of the ACA. In every case the plans were deemed inadequate and often foundered because of their high premiums, exclusions for pre-existing conditions, and annual and lifetime limits. Some states were forced to cap enrollment to limit costs.

Why the capitulation?

Some pundits are reporting that the Democratic capitulation “was all about the filibuster.” Others suggest the cutoff of food stamps was a larger issue. “Trump was purposefully making the shutdown hurt as many people as possible,” wrote Bill Scher of Washington Monthly. Yet “little in this deal is going to prevent him from inflicting further harm.”

The morning headlines in the Kaiser Health News daily feed said it all. “The Trump administration is telling states not to pay full November food stamp benefits, revising its previous guidance after winning a temporary victory at the Supreme Court on Friday,” Politico reported.

Iowa Public Radio reports the federal government ordered states to start enforcing a part of the One Big (Ugly) Bill that cuts off food assistance for refugees and many other types of immigrants with legal status. The Conversation reports the National 211 Hotline has seen calls for food assistance quadruple in recent days, to levels typically seen during natural disasters.

“Shockingly, President Trump and his allies were willing to cut off food assistance to children and fire federal public servants rather than to simply extend an existing tax credit to prevent a premium price spike of hundreds or thousands of dollars for millions of Americans,” Anthony Wright, executive director of Families USA, said in a statement this morning.

“While we are relieved to finally see an end to the longest government shutdown in history — getting federal workers back on the job and ensuring that essential safety net programs like the Supplemental Nutrition Assistance Program (SNAP) can continue — we must continue the fight to contain health costs,” he said. “Americans need a permanent extension of help for health care premiums, and a broader effort to address health care affordability overall.”

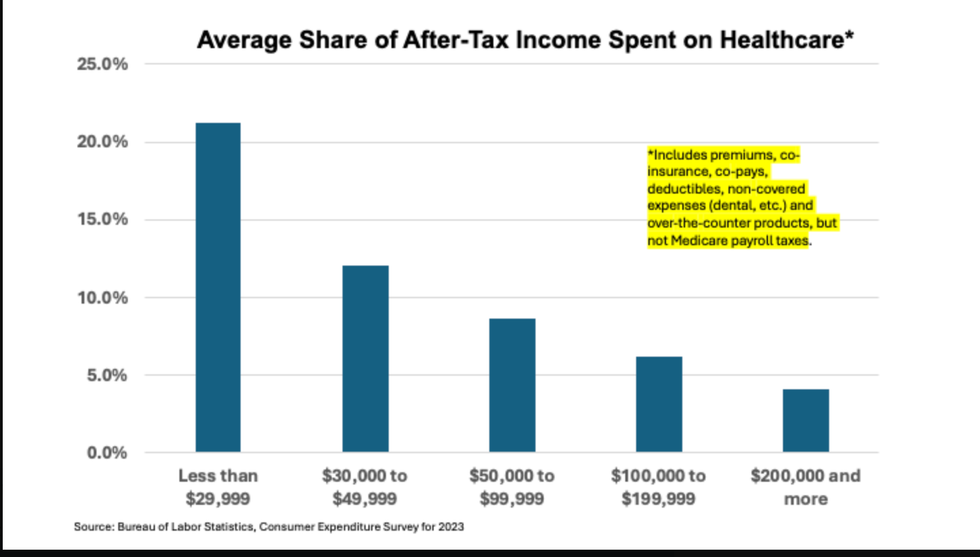

There is definitely a health care affordability crisis. It is being made worse by the Trump regime. I spent some time this morning looking at how out-of-pocket health care expenses are affecting different classes of Americans. Here’s what I found:

...

It’s time for the politicians to start coming up with real solutions to the affordability crisis that is hitting not just people on ACA plans or on Medicaid, but on the broader population. The Trump regime is only making things worse.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News