Do Musk's Record-Breaking Losses Signal The AI Bubble Is About To Burst?

SpaceX’s stock fell another 7.2 percent last week. At its 115 Friday close, SpaceX was 15.0 percent below its issue price and down more than 45 percent from its peak the following week. Those who got out early did quite well, while those who bought in the week after the IPO probably aren’t feeling too good just now.

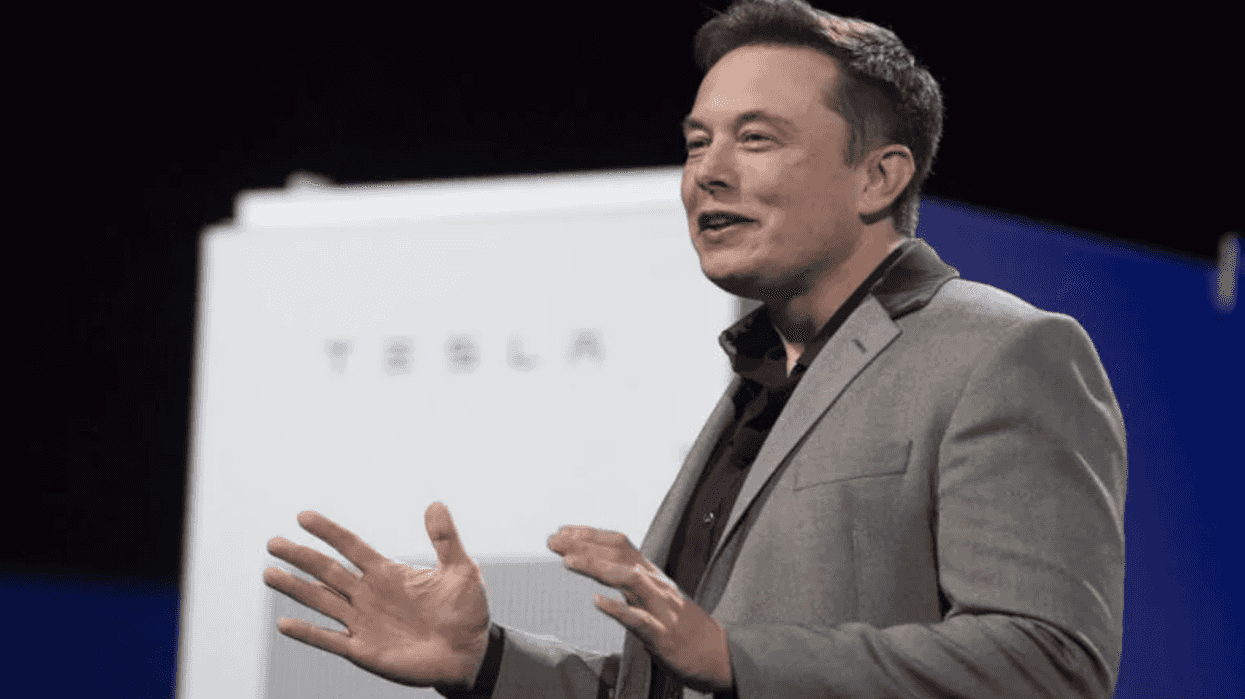

Tesla, Musk’s other big company, did even worse last week, shedding 17.8 percent of its value. That corresponds to a loss of $218 billion in market capitalization. With SpaceX losing $116 billion in value, Musk has likely set a record for losing more money in a single week than any person in history.

But it wasn’t just Musk who had a bad week; the hyperscalers also were not doing very well. Alphabet and Amazon both lost 7.8 percent of their value last week. Amazon lost 6.0 percent, while Microsoft’s stock was down 3.0 percent. Apple managed to almost break even, losing just 0.2 percent of its value.

The big factor in these drops is likely the higher than anticipated capital investment the companies seem to be planning. The increase in spending, coupled with the strong performance of the newest Chinese AI releases, makes it more questionable that the hyperscalers will be able to recover their investments.

The slump of the hyperscalers seems at odds with the strong showing of chipmakers last week. To a large extent, this was just reversing their downturn from the previous week. At the end of the day, if the hyperscalers run into trouble, it’s hard to envision a scenario in which the chip makers aren’t also hard hit. They may still be large, profitable companies, but the massive bonanza their investors now seem to envision will not materialize without a serious AI boom.

It’s always difficult to know the extent to which market movements are based in reality. If you want to see a story of how things are likely to end badly for the hyperscalers and their funders, read Ed Zitron’s Substack. (See also my Mostly Economics interview with him.) He examines at some length how the hyperscalers have created special purpose vehicles (remember Enron?) so as to keep data center- related liabilities off their books.

Ed draws a very bleak picture of a massive bubble of debt that cannot possibly be serviced based on plausible revenue projections from the two major AI companies, Anthropic and OpenAI. I’ll throw in that Ed doesn’t even bring Chinese AI into the picture. That seems to me a very big deal, since Chinese AI companies are already eating up a large and growing share of the market. And even insofar as the U.S. AI companies can hold onto a substantial market share, they will be forced to lower their prices to be competitive.

The layers of finance that Ed describes can be confusing. He compares them to the complex derivative instruments that the financial wizards of the subprime era used to ostensibly minimize risk. For those with the time and energy, it’s worth reading through Ed’s story to get the full picture.

But there is a simple shortcut. If the creation of Special Purpose Vehicles is not a way to hide liabilities, why do it? If Meta, Google, Microsoft, and the rest are confident their bets will pay off, why not just keep them on their own balance sheets like any normal investment? Perhaps there is a benign explanation for going through all these financial hoops, and spending a lot of money to do it, but I am not sufficiently sophisticated to imagine what it could be.

One part of this picture that jumped out at me in reading Ed’s account is that the ability to support this web of debt is likely to be highly sensitive to interest rates. The 10-year Treasury rate was hovering near 4.0 percent when Trump and Netanyahu attacked Iran at the end of February. It is now close to 4.7 percent and more likely headed higher than lower if the war escalates. Trump’s latest round of tariffs is also likely to push interest rates higher.

It would be an interesting irony if Trump’s war and his tariffs proved to be the proximate causes of the crash of the AI bubble.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.