Centrist Democrats Versus Insurgent Socialists Is A Fight Not Worth Having

Whenever I encounter a person, media report, or podcast that’s wound up about socialists taking over the Democratic party and thereby winding down capitalism as we know it, I find myself somewhere between puzzled and eye-rolly.

The main reason for my response is that our economy has always existed on a continuum between pure free markets and deep market interventions by the public sector. There’s Social Security, an intergenerational transfer program that is highly valued by those who identify as die-hard capitalists. Those same capitalists are generally comfortable with Medicare, public infrastructure, laws that protect their property, health, and safety, rules that structure markets, and so on. Taken together, expenditures on Social Security and Medicare amount to about nine percent of GDP. When it comes to such “socialism,” we’re more than a little bit pregnant.

Where we locate on that continuum is a dynamic process driven by the general degree of comfort with the status quo. And today, there is—as there should be—great discomfort among the vast majority with the status quo, in which case we should expect movements along the continuum.

But why move left vs. right? Surely, because of the obvious failure of Trump’s right-wing, faux populism. He ran on making life more affordable than under Biden but to the extent that he’s done anything in the affordability space, he’s pushed hard in the wrong direction. He’s exacerbated inflation, leading to higher interest and mortgage rates than would otherwise prevail, cut taxes for the rich, and partially offset the resulting debt costs by cutting health coverage and nutritional supports for economically vulnerable families. Last week he refused to sign a bill to help, at the margin, increase the supply of affordable housing, because his Republican allies have been unable to pass a vote to rig forthcoming elections (not that they didn’t want to, to be clear, but that they couldn’t get the votes to override a filibuster).

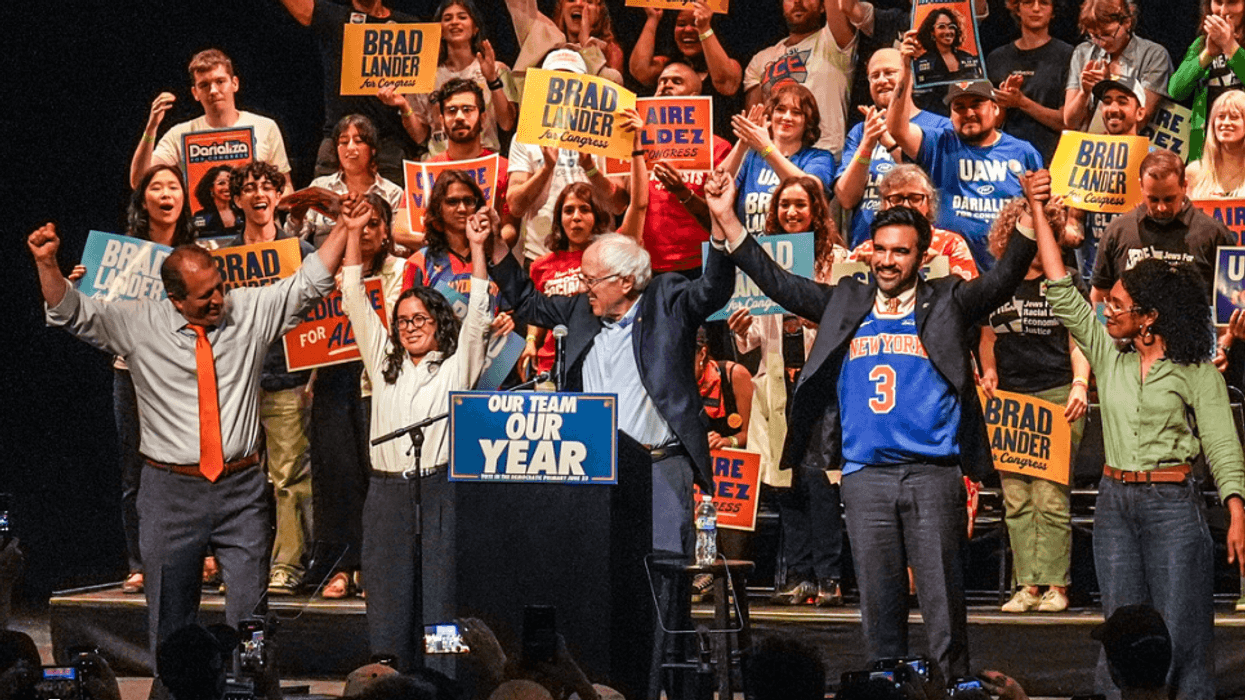

So I don’t think anyone should be surprised that the move along the continuum away from the status quo has been to the left. At the same time, I see no reason for Ds to overreact to this. Mamdani, to take exhibit A in this faux war, didn’t run on socializing the means of production or getting rid of market-based pricing. He ran (in part) on more affordable child care and housing, paid for by higher taxes on the rich.

The Wall Street Journal teed the issue up thusly:

They described the “insurgents” as “[r]unning on a tax-the-rich platform that would provide more services to working Americans, as well as on calls to separate the U.S. from Israel and “abolish ICE.”

First, I challenge you to find a Democrat of any stripe who doesn’t want to provide “more services to working Americans,” and the majority, left and center-left, would raise taxes on the wealthy to offset the costs. Mainstream, centrist Democrats complained bitterly, and justly so, when Trump and the Republicans extended their tilted, regressive tax cuts. Given the actions of the Netanyahu government, that part of our historical status quo must also change, something we’re hearing a lot more from moderate Democrats (and moderate Republicans).

The ICE call is trickier because for many voters, it suggests opening the borders to undocumented immigration in ways to which most Americans, and most Democrats, object. But it is clear to me and anyone else paying attention that we must abolish the unchecked, murderous power of this corrupted agency. I doubt there are many Americans (to be clear, I know there are some; in fact, a nontrivial minority) who are comfortable with the fact that the killers of Alex Pretti and Renée Good—and the killers’ enablers—have come nowhere close to being held to account.

I don’t mean to downplay the socialism label, which is surely notable. And I do think it expresses a frustration with current day, U.S.-style capitalism, a system that is currently and massively rewarding tech oligopolists who blithely pronounce that their latest and greatest invention is going to dis-employ large swaths of the workforce. Would you expect a regular, not-particularly-ideological person, struggling to make ends meet, whose grown kids can’t afford a home, while the deeply corrupt president takes equity shares in private companies, to stand up and applaud today’s capitalism? Or might you expect them to be open to a different offer?

So, let’s talk about that offer. Because this, not the label, is what will ultimately matter. If Mamdani and the other new-wave Democratic Socialists can deliver on the affordability and social justice agenda where status-quo purveyors—in both parties—have come up short, then they should and will win. If they fail, they’ll be kicked to the curb like every other incumbent these days.

In this regard, there is solid logic to the idea of collecting more tax revenues from those who’ve benefitted most not just from market forces (often juiced by regulatory protections—see Baker’s work on patents and monopoly power) but from decades of high-end tax cuts, and use some of those resources to offset the affordability crisis facing middle and low-income families.1

Rent control, on the other hand, sounds good to stretched renters and is a rare housing policy that helps people today vs. years in the future when affordability policies (like those in the ROAD Act) finally lead to added housing supply. But it has a track record of doing more harm than good. A lot of landlords are also stretched, and the rent freeze will make it harder for them to maintain upkeep. Worse, evidence shows rent control to lead owners of rental units to get out from under the freeze by converting to condos.

Still, good for Hizzoner for delivering on his campaign promises, in this case a two-year rent freeze on 40 percent of New York City apartments. I worry this one will have unintended consequences, and if I’m right, his administration should unwind it early.

That last part seems important to me. Again, forget about the names and labels. The future of democracy and the potential for getting back to functional governance requires a lasting political coalition, and that can only be built by delivering help to the people who need it the most. If you ran on a rent freeze, that go ahead and try a rent freeze. But if it backfires, quickly explain to your constituents that it isn’t working, you’re ending it, and you’re moving on to plan B, followed by, if necessary, plan C (see CAP’s plan for direct rent relief; it’s a federal plan, but aside from Trump, there’s actually bipartisan interest in addressing the shortfall in affordable housing).

Remember what Roosevelt said in 1932, another period when capitalism’s flaws were blatantly transparent: “The country needs and, unless I mistake its temper, the country demands bold, persistent experimentation. It is common sense to take a method and try it: If it fails, admit it frankly and try another. But above all, try something."

One last point about this alleged internal attack by socialist insurgents. As I’ve said, I see no such thing but instead see earnest politicians, and in Mamdani’s case, a highly skilled politician, recognizing that the status quo is broken and reaching for alternatives.

But we do not live in a political vacuum and the right will use the socialists’ wins to try to scare the broad electorate. Their leader posted this on social media:

The Communists are finally making their move. I’ve been waiting and preparing for this for a long time. It’s easy to be a Communist—All you have to do is say, ‘I’ll give you everything,’ but that means you’re taking it away from others that have earned it.

I’m not a political advisor, so take what follows with a shaker of salt. But there is, I believe, a way to break this attack. It starts by recognizing the obvious point that what works in New York City won’t work in most other places. But if it stops there, we’re sitting ducks. Remember, the fact about contemporary Republicans is that they’re awful at governing but a lot better than Democrats at getting elected, largely through fear tactics and pitting people against each other, a strategy as old as politics itself.

The key to winning in this period of unaffordability, chaos, fear, and heightened inequalities is not for Democrats to fight over the socialist, capitalist, centrist or leftist labels, but to connect with voters on how we’re going to help them and equally importantly, on how the other side has failed to do so and still has no idea what to do other than to try to scare people away from new, younger faces with bold, new ideas.

Trump and his reckless, corrupt, and inept enablers promised they’d help people, but clearly they lied, and now, when they’re not engaging in self-enriching grift and graft, they’re name-calling to try to distract us from their blatant failures.

But we know who the enemy is. It is the status quo. The polling, both electoral and consumer sentiment, couldn’t be clearer on this. And to shout “commie!” or “socialist!” at someone with potentially credible ideas on how to wield public policy to help solve real problems is to defend the status quo. Full stop.

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please subscribe to his Substack, from which this is reprinted with permission.