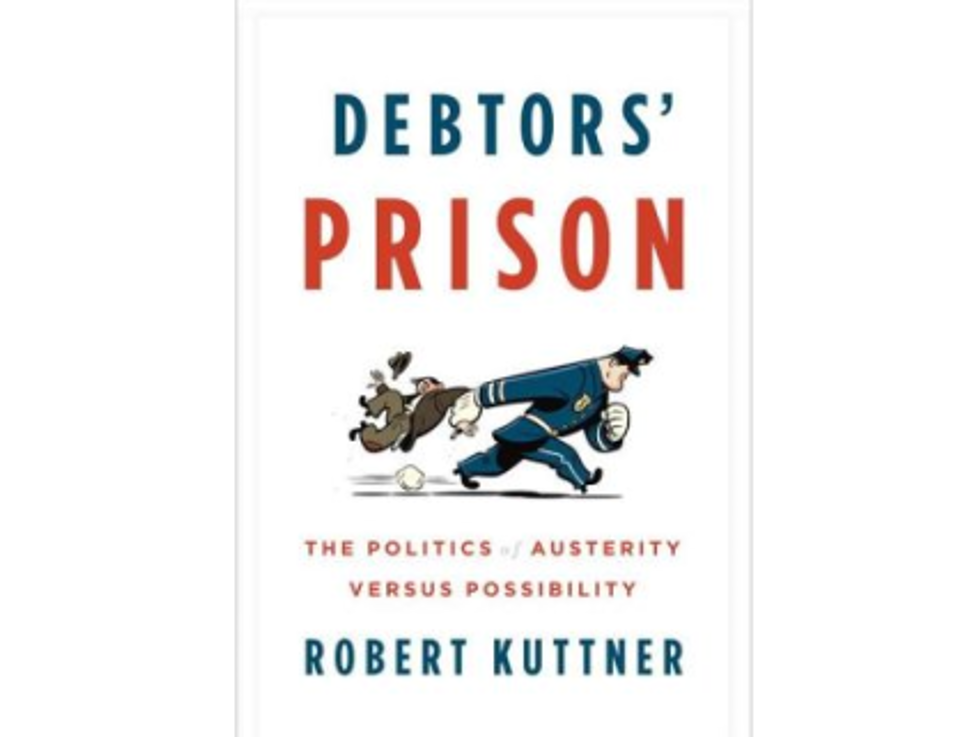

This week, Weekend Reader brings you an excerpt from Debtors’ Prison: The Politics Of Austerity Versus Possibility by Robert Kuttner. Kuttner, the co-founder and co-editor of The American Prospect magazine and a Distinguished Senior Fellow at Demos, argues a compelling case against austerity and outlines the implications this policy could have on Americans.

You can purchase the book here.

Austerity for All Seasons

The crusade for fiscal austerity has had three distinct phases. Deficits became a public issue in the mid-1980s after the “supply-side” tax cuts of the first Reagan term failed to deliver the promised revenue increases. The tax breaks, not surprisingly, reduced government income. Deficits, ironically, were disguised by the huge increases in payroll taxes of the 1983 Social Security reform, trillions destined for retirement trust funds—which were then borrowed by the rest of the government, lowering the consolidated government deficit.

Reagan’s budget imbalance was further exacerbated by a military buildup. Deficits averaged about 4 percent of GDP throughout the Reagan and George H. W. Bush presidencies, increasing the debt ratio from under 30 percent before Reagan took office in 1981 to over 50 percent at the time of the 1992 election. There were several attempts to put the budget on an automatic path to deficit reduction, using different versions of a “trigger” formula of automatic budget cuts sponsored by Representative Phil Gramm of Texas and Senators Warren Rudman of New Hampshire, both Republicans, and Senator Ernest Hollings of South Carolina, a fiscally conservative Democrat. Though trigger mechanisms were enacted, these efforts did not reduce deficits much, in part because an economic slowdown in the late 1980s reduced revenues. Bush, having sworn “Read my lips, no new taxes” in his 1988 nomination speech, infuriated supporters by signing a 1990 budget deal that included modest tax increases. But the debt remained on an upward path.

By the time of the 1992 election, more than twenty years ago, the rising debt and the political deadlock over how to address it had already become an emblem of dysfunctional government. Ross Perot, running as a third-party candidate, combined deficit reduction and economic nationalism into a weirdly populist crusade. To Perot and his supporters, failure to deal with the deficit symbolized the bankruptcy of the two major parties. For several weeks in the spring of 1992, polls that showed Perot was running ahead of both Clinton and Bush. In early 1992, Peterson founded the Concord Coalition as a lobby for balanced budget, joining with Rudman and Senator Paul Tsongas, a Democratic deficit hawk from Massachusetts. The coalition was substantially underwritten by Peterson.

![]()

But an economic boom and President Clinton’s politically brave tax increase on the richest 2 percent of Americans nearly put the austerity lobby out of business. In 1993, Clinton struck a famous deal with the chairman of the Federal Reserve to trade smaller deficits for lower interest rates. The two policies had no logical connection, except in Alan Greenspan’s ideology. Projected deficits were in fact having no effect on interest rates, which were the province of the Federal Reserve. Cutting the deficit was thus a political imperative, not an economic one. But after the 1993 budget raised taxes, cut spending, and reduced the deficit, Greenspan delivered on his part of the deal. With lower interest rates, growth rebounded throughout the 1990s.

After the strong economic performance balanced the budget in 1999 and endless surpluses were forecasted, the Concord Coalition took down its clock at Times Square that displayed the escalating national debt. Peterson’s book Facing Up had in 1993 gravely predicted a $300 billion deficit by 2000. That year, the actual budget was in surplus by $236 billion.

Higher growth and reduced unemployment also increased payroll tax receipts and moved the Social Security accounts further into the black. Deficit hawks were fond of pointing to estimates by the Social Security trustees projecting that at some point in the 2030s or early 2040s Social Security would not be able to meet all of its anticipated obligations. The 2012 Trustees’ report put the program’s long-term deficit at about 1 percent of GDP—something easily solved by modest tax increases on high-bracket wage earners, or better yet, by raising wages.

Social Security is financed by taxes on wage and salary income. It is at risk of incurring a modest shortfall three decades from now only because wages have not kept pace with productivity growth. If wages tracked productivity, Social Security would never be in deficit. In one three-year span during the booming 1990s, the date of Social Security’s projected shortfall was pushed back by eight years—from 2029 to 2037—because a high-employment economy meant more payroll taxes coming into the Social Security trust funds. At that rate of improving solvency, Social Security would soon be in perpetual surplus. All it took was decent economic growth with fruits shared by wage earners. The budget hysteria lost its credibility, and the austerity crusaders went into temporary eclipse.

What saved the budget hawks crusade were two new sets of entirely gratuitous deficits. These were produced first by the tax cuts and wars of the George W. Bush administration and then by a financial collapse created on Wall Street. The budget went moderately back into deficit in 2002. By fiscal year 2008—the last of the Bush presidency—the deficit had increased to 3.3 percent of GDP, enough to give Peterson and company a second wind.

In 2007, David Walker, still head of the GAO, and Robert Bixby, executive director of the Concord Coalition, set out on a Fiscal Wake-Up Tour, which was underwritten by the Peterson Foundation. In 2008, the foundation paid PBS to air its film, I.O.U.S.A, covering the same tour. In other words, the foundation paid public TV to treat its own event as news. In the film, David Walker warns, “We suffer from a fiscal cancer. It is growing within us, and if we do not treat it, it could have catastrophic consequences for our country.” The movie was also shown in some four hundred theaters and broadcast as part of a CNN special on the fiscal crisis that Peterson’s people coproduced.

![]()

In a depressed economy, fiscal tightening turns deeply perverse. But as the economy went into a debt deflation, the austerity lobby did not alter its message at all. It simply treated the economy’s new woes as an ideological windfall, demonstrating the urgency of deeper cuts in a now-larger deficit. In I.O.U.S.A., headlines of a crashing economy are ominously juxtaposed with statistics on rising deficits, as if the deficits had caused the crash, rather than vice versa.

The financial collapse, predictably, caused a sharp deterioration in the nation’s fiscal picture. The federal deficit swelled from 3.3 percent in fiscal year 2008 to 10.1 percent in 2009, then declined slightly to 9 percent in 2010 and to 8.7 percent in 2011. Of the projected increase in the deficit between 2010 and 2020, only about 9 percent is the result of deliberate federal stimulus spending.

Nonetheless, the growing deficit was taken as vindication of the hawks’ earlier claims, even though that inverted the actual cause and effect. Through some alchemy, progress on long-term deficit reduction would supposedly restore business confidence and thus economic growth—as if entrepreneurs were basing their investment decisions in 2013 on deficit projections for 2023. The economist Paul Krugman aptly termed this wishful claim “the confidence fairy.”

Excerpted from Debtors’ Prison by Robert Kuttner. Copyright © 2013 by Robert Kuttner. Excerpted by permission of Knopf, a division of Random House, Inc. All rights reserved. No part of this excerpt may be reproduced or reprinted without permission in writing from the publisher.