No, We Don't Need Billionaires -- Or Gross Inequality -- For Prosperity And Progress

The Economist gave us a classically sloppy piece last week, telling us that we need the mega-wealthy types like Elon Musk and Mark Zuckerberg. The argument is largely tautological.

It points out that the mega-rich have been responsible for the diffusion of important technologies. There is considerable truth to that, but this is because we have structured the economy in ways that allowed people to get super-rich by gaining control of important technologies. If we had structured the economy differently, we wouldn’t have super-rich people responsible for tech's spread.

For example, who was the mega-rich person for the near-universal acceptance of the polio vaccine, not just in the United States but around the world? This vaccine has saved tens of millions of lives over the last 70 years. Its developer, Jonas Salk, never bothered to patent it, saying the knowledge belonged to the world.

There is a similar story with insulin. The developers, Frederick Banting, Charles Best, and James Collip, sold their rights for $1 each in 1923. Tens of millions of diabetes patients have been able to live relatively normal lives as a result of their discovery, but no one got rich from it. (This has not prevented drug companies from making huge sums by patenting various processing techniques and charging markups of several hundred percent.)

We don’t just have to look to medicine. There were great innovations in most areas attributable to people who did not get ridiculously rich. It was not Steve Jobs and Apple who invented the mouse, although they did popularize it. The invention was by Douglas Engelbart in 1963, a researcher at Stanford Research Institute.

There is a similar story with DOS, the Microsoft operating system that has been used in billions of computers around the world. This was not invented by Bill Gates and his team, but rather by Tim Paterson, a software engineer working for Seattle Computer Products.

And the Internet came out of a military project, the ARPANET for connecting computer systems. No one got insanely rich from this innovation either.

We have structured the system so that someone like Bill Gates can gain control over a technology like DOS and become ridiculously rich by popularizing it, but it doesn’t follow that DOS, or perhaps a better system, might not have been widely adopted in a comparable time frame without someone like Bill Gates getting very rich.

The Economist piece is just looking at the ridiculously rich people of the last century and a half and implying that the innovations they are associated with would not have taken place otherwise. That is a logical leap bordering on absurdity.

Capitalism Can Be Structured Differently

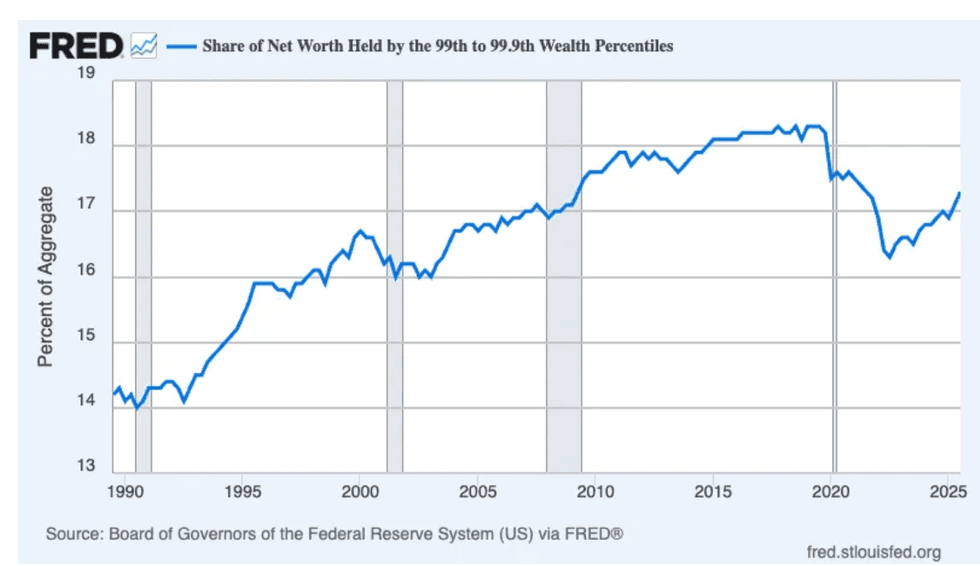

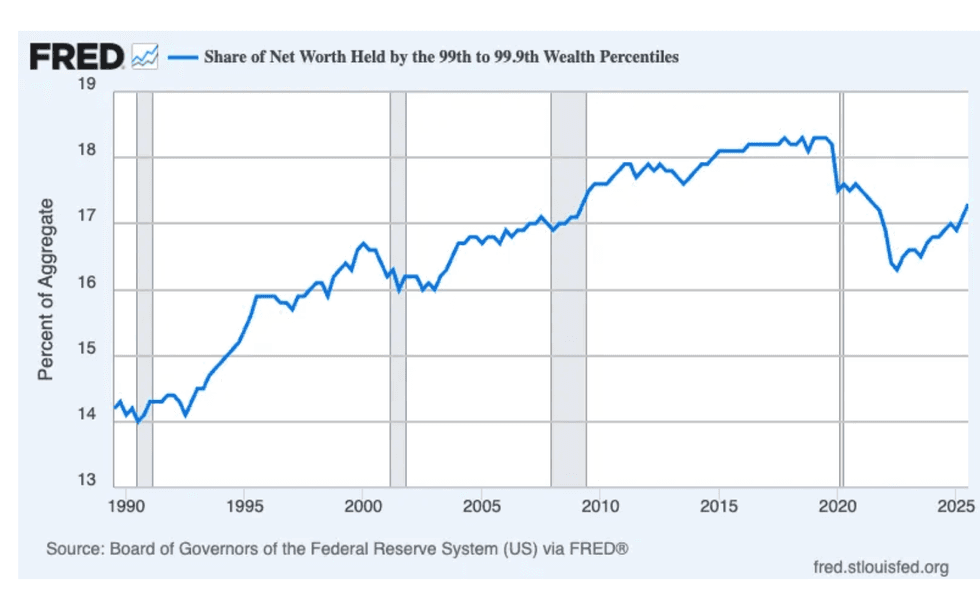

To be clear, this is not a question of whether or not we want capitalism. I’ll leave that one to others. But as I have argued repeatedly, capitalism is an infinitely malleable system. It can be structured in an endless number of different ways, some of which will lead to far less inequality. We seem to have structured it in a way to maximize inequality.

I’ll give some of my favorites below, but the list is far from comprehensive. I’ll also skip anti-trust for two reasons. First, antitrust policy is an important issue, but everyone talks about it. With some notable exceptions (e.g. the lawsuit against Microsoft in 1998), the watchdogs have largely been asleep for the last forty five years, but they did briefly awaken under Biden.

The other reason I am less fond of talking about antitrust is that it requires government action. (Actually, private actors can sue as well, but it’s difficult.) I like to focus on the ways in which the government actively structures the market to take money from everyone else and give it to the rich and very rich.

Government-granted patent and copyright monopolies

This one always leads the list, both because there is a huge amount of money at stake and these monopolies are so obviously the result of government action. Capitalism is still capitalism if the government doesn’t hand out these monopolies.

Patents and copyright monopolies are government policies to promote innovation and creative work, but there are alternative mechanisms that can be used. And even if it uses these monopolies, they can be shorter and weaker, transferring less money from the rest of us to the monopoly holders.

There is easily over $1 trillion a year in income at stake with these monopolies. That figure is over one-third of all after-tax corporate profits. The largest chunk is with prescription drugs and other pharmaceutical products, where we likely spend over $750 billion this year on items that would likely cost us less than $150 billion in a free market, a gap of $600 billion.

Software is another case where these monopolies matter hugely. Bill Gates and Larry Ellison are two of the richest people in the world because the government gives Microsoft and Oracle monopolies on their software.

The importance of these monopolies to both the economy and inequality should be obvious. And we can use alternative mechanisms, most obviously publicly-funded research. We used to support more than $50 billion in biomedical research through the National Institutes of Health.

We would have to triple or quadruple this to replace the research supported by patent monopolies. But publicly supported research would have the advantage that it could be open source. Taking away the patent monopolies would also take away the industry’s incentive to lie about the safety and effectiveness of their drugs, as they did in a big way in the opioid crisis.

We can also have more public funding in other areas, including for creative work. We may want to still use patents, but we can make accepting much shorter patents a condition of getting access to publicly funded research. (See Chapter Five of Rigged [it’s free] for an outline of this story.)

Let the Financial Industry Enjoy the Free Market

The billionaires of Wall Street like to pretend they are swashbuckling capitalists, at least until they sink themselves with their greed, when they run to the government and demand a bailout. They did in a huge way in the 2008-09 financial crisis, when they pushed the Big Lie that we would face a Second Great Depression if the government didn’t come to their rescue.

This was an obvious lie since we learned the secret for getting out of a depression 70 years earlier: it’s called “spending money.” We did this in a big way with World War II, but spending on wars doesn’t magically affect the economy in a way that’s different from government spending on things like healthcare and solar panels. This is pretty simple stuff, but if you tried to say this back when Wall Street was demanding taxpayer dollars, you weren’t invited to the discussion.

And we don’t have to go back to the ancient history of the financial crisis. Just a few years ago, Trump crypto czar David Sachs was leading the charge for a bailout of Silicon Valley Bank, where his friends apparently parked a lot of cash. Capitalism is still capitalism if the government doesn’t bail out banks that put themselves into bankruptcy.

And we don’t have to exempt the financial industry from the sort of sales taxes most states impose on items like food and clothes. A modest sales tax on financial assets (e.g. 0.1 percent on stock trades and 0.01 percent on derivatives) would likely cut the size of the industry in half, eliminating an enormous amount of waste, as well as really big fortunes.

And since we’re talking about leveling the playing field, we should end the carried interest loophole that allows hedge fund and private equity partners, some of the richest people in the country, to pay the 20 percent capital gains tax rate instead of the normal 37 percent rate. The ostensible rationale is that they are paid on commission, like realtors or car salespeople.

Whack Private Equity: The Structure of Bankruptcy Laws Is Not Intrinsic to Capitalism

One of the big games for private equity (PE) firms is to strip assets from the companies they buy. They have the companies pay big dividends to the PE partners, often taking on debt for the companies (not the PE firm) to make the payment. They also sell off real estate or other assets and pocket the money themselves.

This puts the PE firm in a perfect win-win situation. If they can keep the company in business and then take it public again, they make a fortune, since they likely have already recovered most or all of their investment by stripping its assets. If the company ends up in bankruptcy, they just walk away, screwing its creditors, which can include suppliers, landlords, and workers with pensions.

One way to alter the equation is to restructure bankruptcy law to make PE companies that control other companies responsible for their liabilities. If a company that controls another company is responsible for its liabilities in bankruptcy, we still have capitalism.

Make Non-Compete Agreements Unenforceable

A non-compete agreement is a clause in an employment contract that prohibits a worker from working for a competitor or starting their own business in the same field. There is a limited rationale, for example, when top researchers have access to a company’s latest product designs. But non-compete agreements have proliferated in the last quarter century to the point that a sandwich chain was prohibiting its workers from being employed elsewhere.

The laws on this can be changed, as Biden’s Federal Trade Commission tried to do, so that most non-competes would not be enforceable. If anyone thinks that not enforcing all contracts is inconsistent with capitalism, think again. In most states, a contract that an employer signs with a union, requiring all workers to pay a union representation fee, is not enforceable. (They call it “right-to-work.”)

The government always sets boundaries on which contracts it will enforce. Those boundaries don’t have to be set in a way that hugely favors employers. There are many other issues with labor-capital relations where the rules have been written to favor employers. Again, these can be changed.

Capitalism Needs to be Restructured to Produce Less Inequality

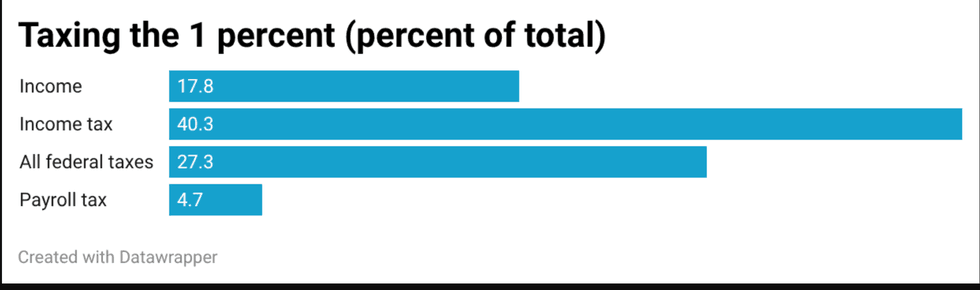

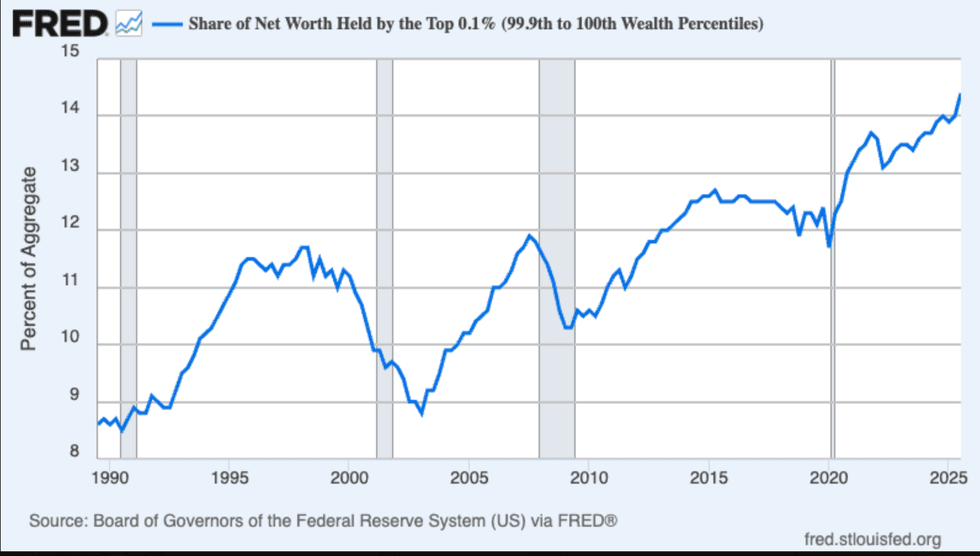

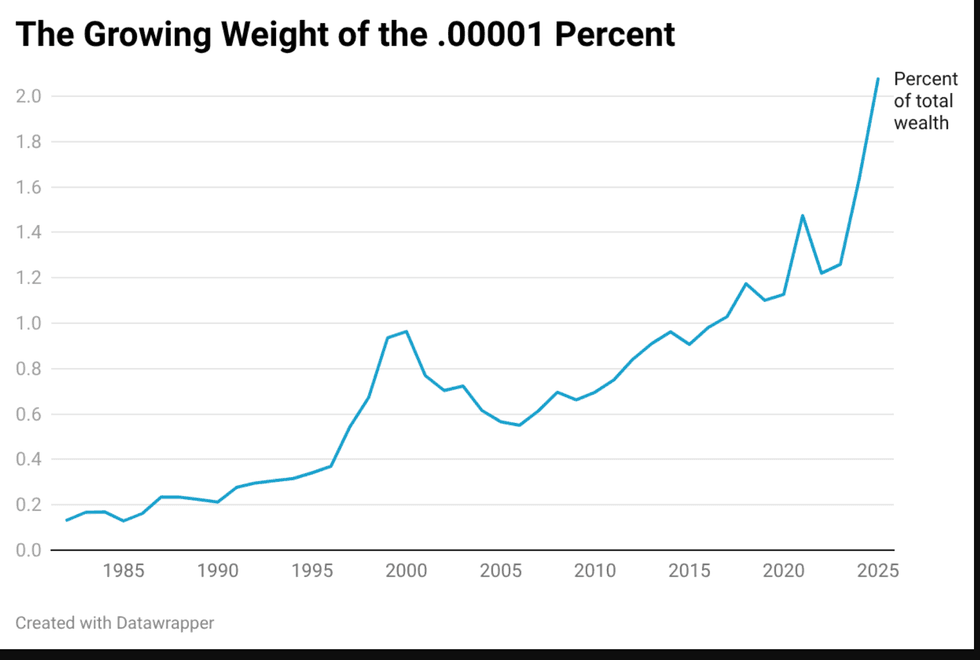

It is incredibly lazy to treat the massive inequality we see as the natural outcome of capitalism. It is understandable that the people who benefit from this inequality would make that claim, but it is bizarre that the people seeking greater equality would as well. It’s fine to try to tax back some of the wealth that we have handed to the billionaires, but the much better solution is to not give it to them in the first place.

Getting back to The Economist’s basic argument, maybe a greed-crazed billionaire will lead home computers or social media to spread slightly faster than would otherwise be the case, but so what? Would we have suffered enormously if we all got our first PC a year later than we did?

And the flip side of this story, apart from handing enormous wealth and power to a tiny group of people, is that the billionaires are often total jerks. We don’t have to look back to ancient history to see examples of mega mistakes by the mega-rich. Mark Zuckerberg threw over $80 billion in the toilet, pushing his “Metaverse,” which went nowhere. We can survive just fine without such nonsense.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.

Reprinted with permission from Dean Baker.