Warning: Here's Why The Fed Can't Rescue Markets From AI Bubble

While everything feels political now – a kind of fin de siècle chaos politics – I want to take a brief break from the political today. Instead I want to talk about asset markets and the Fed.

We could say that the US economy in 2025 was schizoid. On the one hand Donald Trump abruptly reversed 90 years of U.S. trade policy, breaking all our international agreements, and pushed tariffs to levels not seen since the 1930s. Worse, the tariffs keep changing unpredictably. This uncertainty is clearly bad for business and is depressing the economy. On the other hand, there has simultaneously been a huge boom in AI-related investment, which is boosting the economy.

As many people have already noted, the AI boom bears an unmistakable resemblance to the tech boom of the late 1990s — a boom that turned out to be a huge bubble. The Nasdaq didn’t regain its 2000 peak until 2014.There’s intense debate about whether AI investment is similarly a bubble, which I would summarize as a shoving match: “Is not!” “Is too!” “Is not!” “Is too!”

While my personal guess is that AI is indeed in the midst of a bubble, I won’t devote today’s post to that debate. Instead, I want to talk about one recent aspect of market behavior that is very striking and carries strong echoes of the tech bubble a generation ago. Namely, AI-related stocks, like tech stocks back then, are reacting very strongly to perceptions about the Fed’s short-term interest rate policy.

Now as then, these strong reactions don’t make sense.

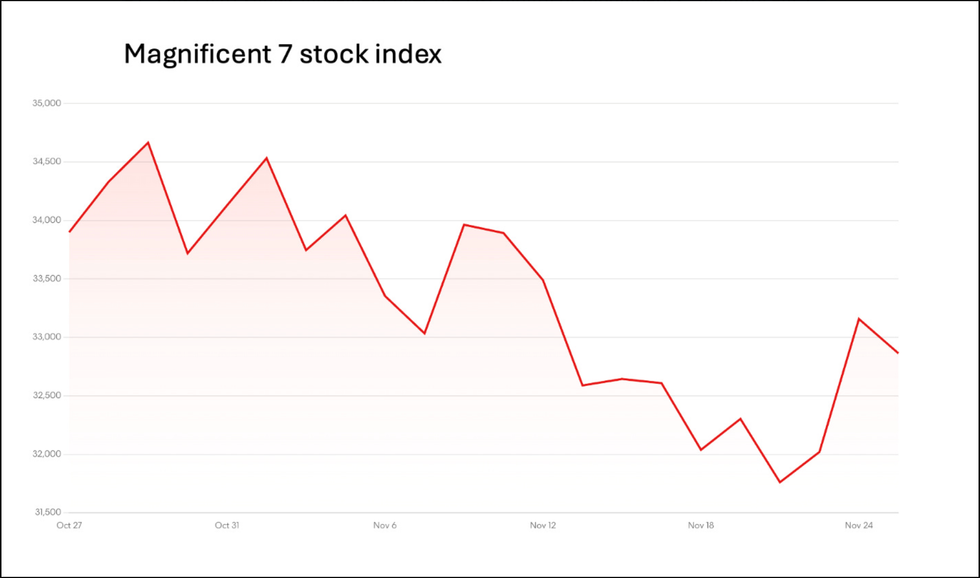

To see what I’m talking about, consider recent moves in stock prices closely related to AI. This chart shows movement over the last month of Bloomberg’s “Magnificent 7” stock index:

Source: Bloomberg News

Source: Bloomberg News

During most of that month, these stocks were falling, as concerns that AI is a bubble increased. But on Monday the Mag7 index surged, erasing a large fraction of the losses. Why? Analyst chatter about supposed causes of stock market swings should always be taken with many grains of salt. But it’s clear that this surge was catalyzed by remarks by Fed officials which the market interpreted as making a cut in the Fed Funds rate next month more likely.

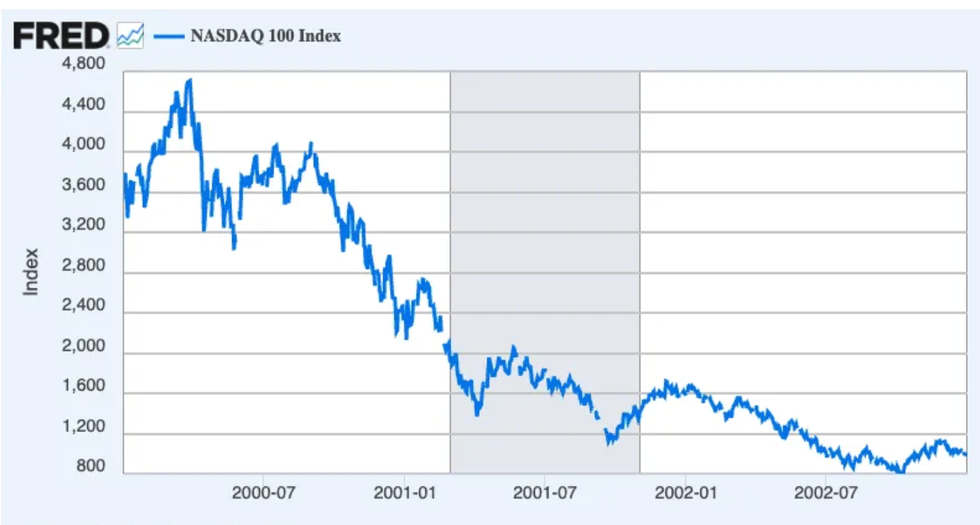

Some of us have seen this movie before. For those who haven’t, there is a pervasive view that the deflation of the 90s tech bubble was something that happened all at once — a Wile E. Coyote moment in which investors looked down, realized that there was nothing supporting those high valuations, and the market plunged. In reality, however, it was a long, drawn-out process, punctuated with some significant dead cat bounces along the way. Here’s the Nasdaq 100 over the relevant period (the gray bar represents the 2001 recession):

Source: NASDAQ via FRED/St.Louis Federal Reserve (stlouisfed.org)

Source: NASDAQ via FRED/St.Louis Federal Reserve (stlouisfed.org)

Measured against the awesome scale of the ultimate tech-stock decline, the temporary rallies along the way don’t look that big. But they were actually huge compared with normal stock movements. Let’s look at a closeup:

Source: NASDAQ via FRED/St.Louis Federal Reserve

Source: NASDAQ via FRED/St.Louis Federal Reserve

What drove these temporary bouts of optimism? At the time the conventional wisdom was that they were the result of Fed interest rate reductions and the prospect of further cuts. In fact, many observers used to argue that the stock market was underpinned by the “Greenspan put”: Don’t worry about a crash, Uncle Alan will ride to the rescue.

And after Monday’s stock price spurt, it’s clear that belief in a “Fed put” has made a modest comeback.

Indeed, the graph below shows the numerous rate cuts as the tech bubble burst:

But while these rate cuts did create brief bouts of, well, irrational exuberance, they did nothing to prevent the tech bubble from eventually deflating.

Why couldn’t Greenspan rescue tech stocks? To answer that question, think about why interest rates matter for asset prices: Lower interest rates reduce the rate at which investors discount expected future returns. A dollar delivered to you X years from now has a higher “present value” (that is, a higher current value) if interest rates are one percent than if they’re six percent. How much higher depends on X, the number of years until you receive it.

For example, a house can last for generations, and it delivers value to its owner in the form of a place to live over the years. That stream of housing consumption over the years is worth more – has a higher present value -- when the interest rate is one percent than when it is six percent. Or to put it another way, if you can make six percent on your money in a bank deposit, you may be better off renting rather than buying. That’s why the demand for houses is strongly affected by mortgage rates.

Interest rates matter much more for the value of assets that will still be yielding returns 10 or 20 years from now than they do for assets that will only yield returns for a few years.

That is, the value of assets that have a short economic life is much less affected by interest rates. Not surprisingly, economists have consistently had a hard time finding evidence for any effect of interest rates on business investment.

Moreover, investments in digital technology tend to have an especially short half-life, precisely because rapid technological progress quickly makes equipment and software obsolete. How valuable will data centers currently under construction be 5 years from now? Will they be worth anything 10 years from now? A realistic answer to these questions surely implies that the Fed’s interest policy should have little to no impact on Mag 7 valuations, or the sustainability of the tech boom.

As we saw on Monday, however, Fed policy and rumors about future Fed policy can sometimes affect AI-stock prices in the short run. But by the straight economics, these movements are more the result of market psychology than of any objective assessment of future returns.

So as doubts about AI creep in, I’m hearing growing chatter to the effect that the Fed can and should save the industry. But the lesson from the last big tech bubble is that it can’t. In fact, I have doubts about whether the Fed can head off a broader recession if the tech boom collapses — but that’s a topic for a future post.

For now, my point is that if you’re worried about an AI bubble, don’t expect Jerome Powell or his Trump-appointed successor — rumors are not encouraging — to come to the rescue. They can’t.

Paul Krugman is a Nobel Prize-winning economist and former professor at MIT and Princeton who now teaches at the City University of New York's Graduate Center. From 2000 to 2024, he wrote a column for The New York Times. Please consider subscribing to his Substack.

Reprinted with permission from Paul Krugman.