Trump Accounts Are A Sick Joke, Not A Replacement For Social Security

Many of the Trump crew seem to be delusional about Trump accounts. They claim to believe that they will replace Social Security. It shouldn’t be a surprise to us that many supporters of Trump are out of touch with reality, but that is not a reason for the rest of us to take their nonsense seriously.

Let’s keep our eyes on the ball. This is not three-dimensional chess; it is an account for newborn kids in which the government deposits $1,000. Parents or other relatives can add to it each year, like they can add to an education savings accounts in most states. The amount people contribute to the account is deducted from their taxable income. Also, the money accumulated in the account is not taxed until it is withdrawn.

Some people take advantage of these accounts; most don’t. The reason is that most people don’t have an extra $1,000 or $5,000 or whatever to contribute to a Trumo account. Furthermore, the tax benefit is not a very big deal to most moderate and even middle-income people.

The overwhelming majority of households are in the 12 percent bracket or below. More than a fifth are in the zero bracket, meaning they pay no income tax and would get no benefit from tax-advantaged accounts.

Furthermore, even if they wanted to put money in a tax-advantaged account, why would they choose a Trump account rather than an education savings account or an IRA? Money in existing tax-advantaged accounts can be withdrawn, albeit with a penalty. Money in a Trump account can only be accessed by the kid when they turn 18.

This brings us to the sick joke part of the Trump account story. Trump and Congressional Republicans have been gleefully cutting Food Stamps, housing assistance, Medicaid, and the subsidies in the Obamacare exchanges. As a result, tens of millions of people will be denied benefits that they previously depended upon.

Many of these people will end up hungry, homeless, and/or unable to obtain needed medical care. This means two or three years from now, there are likely to be tens, or even hundreds, of thousands of kids with $1,000 in their Trump accounts who are living on the streets, going hungry, or unable to get necessary medical care because Trump has cut the programs their families depend upon.

This will make for great photo ops. Maybe Trump can have some homeless kids over to the White House, or even Mar-a-Lago, and they can talk about living in the streets of Chicago in winter, or the needed surgery that they can’t afford, but they still have $1,000 in their Trump account. Then Trump and his entourage can all say how great that is!

The other part of the story is the nutty illusion about how rapidly these accounts will grow. The Trump gang likes to say they will grow 10% a year. Amazingly, many who are not on Team Trump are prepared to accept this nonsense.

The 10% rate of return is based on looking at the past, where stocks have yielded somewhere close to a 10% rate of return over the last eight decades. But this is a case of incredibly bad induction, sort of like the person who falls off an 80- story building and says as they pass the 60th floor, the 59th floor, and the 58th floor, “so far so good.”

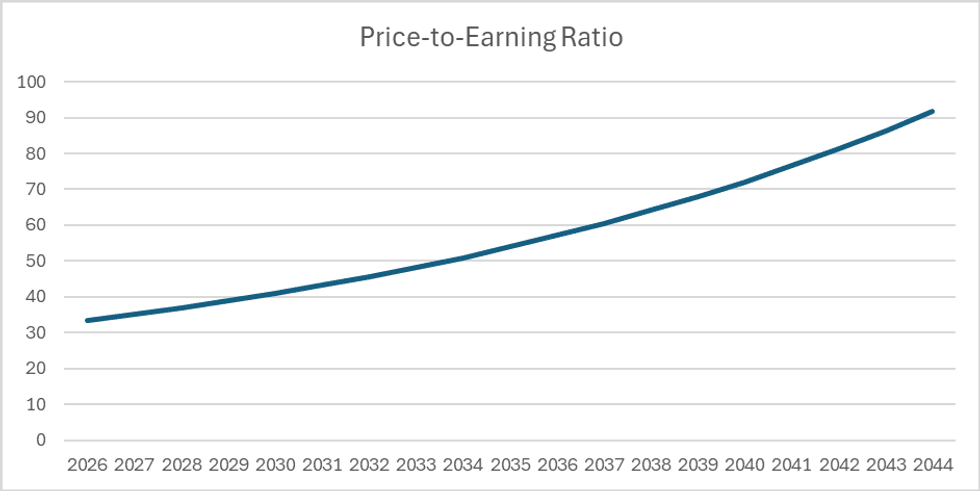

The simple and obvious point that people who make this inference miss is that the stock market was valued far lower relative to corporate earnings in prior decades than is the case today. Through most of the decades of the 40s, 50s, 60s, and 70s, the price-to-earnings ratio (PE) was generally in the low teens and often considerably lower. When the PE is low, and the economy is growing relatively rapidly, it’s possible for the stock market to generate 10 percent nominal returns, or seven percent real (inflation-adjusted). That’s somewhat oversimplifying the inflation story, but it doesn’t affect the argument.

Today, the PE is over 30, and the economy is projected to grow roughly 2.0 percent a year going forward. In that world, the only way to generate the historic seven percent real rate of return is with an ever-rising price-to-earnings ratio.[1]

The Trumper’s story gives us a PE of almost 92 when today’s newborns turn 18 in 2044.[2] If we want to ask what happens if they hold their money until they hit the Social Security normal retirement age of 67, the PE will be over 2000. A Trump administration economist may be able to make this sort of projection with a straight face, but not many other people could.

Is there a way around this story? Well, the after-tax profit share of GDP could rise further, as it has been doing for the last quarter century. This would be a bleak story for the rest of us, since it would likely mean wages are shrinking. It would also have to almost triple in the next 18 years to keep the PE constant. This is close to unimaginable and a truly horrible story, even if it were. For what it’s worth, the Congressional Budget Office projects the profit share will fall in the next decade.

People could invest their Trump accounts overseas. China is having far more rapid growth than the United States, so perhaps people can get closer to 7.0 percent real returns there. Maybe this is what the Trump gang has in mind.

If we look at the actual returns that people can expect in their Trump account, it will be close to 3.0 percent a year in real terms, assuming that they are not ripped off badly on fees by one of Trump’s Wall Street friends. That will give today’s newborn $1,700, adjusted for inflation, when they turn 18.

Somehow, I don’t think this will lead people to discard Social Security. But I could be mistaken.

[1] I wrote about this issue in a paper with Brad DeLong and Paul Krugman 20 years ago in the context of the Bush Social Security privatization drive.

[2] The data for after-tax corporate profits Bureau of Economic Analysis, National Income and Product Accounts, Table 1.12, Line 15. The data for the valuation of the stock market comes from the Federal Reserve Board’s Financial Accounts of the United States Financial Accounts, Table L.2, Line 38, plus Table l.108, Line 20. The 2.0% GDP growth projection is from the Congressional Budget Office’s Long-term Budget Projections. The projection assumes that companies pay out 60 percent of their profits as either dividends or share buybacks, and the rest of the seven percent real return is made up through capital gains.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.