While everyone’s fishing with clickbait these days—it’s an e-jungle out there—the highly experienced economic journalist Neil Irwin doesn’t make bold claims without some backup. So, when I read this Axios headline from him on Monday, I said “hmmmmm.” I stroked the chin. I furrowed the brow. I asked myself, “is that right?” I answered, “it could be!”

I mean, the economic problem of the decade is surely what Trump is in the process of doing to global economics, but where I go with Neil’s assertion, as you’ll read below, is more about whether something structural (vs. cyclical, as in the business cycle) has changed in how inflation is generated in the U.S. and other advanced economies. In fact, there’s an interesting new Fed Note on the topic which I’ll also highlight below. Like I said, my read of the evidence is maybe (re upward, structural change) but the fact that inflation’s been buffeted by a series of identifiable shocks means that it still may settle back into something closer to its pre-pandemic pattern.

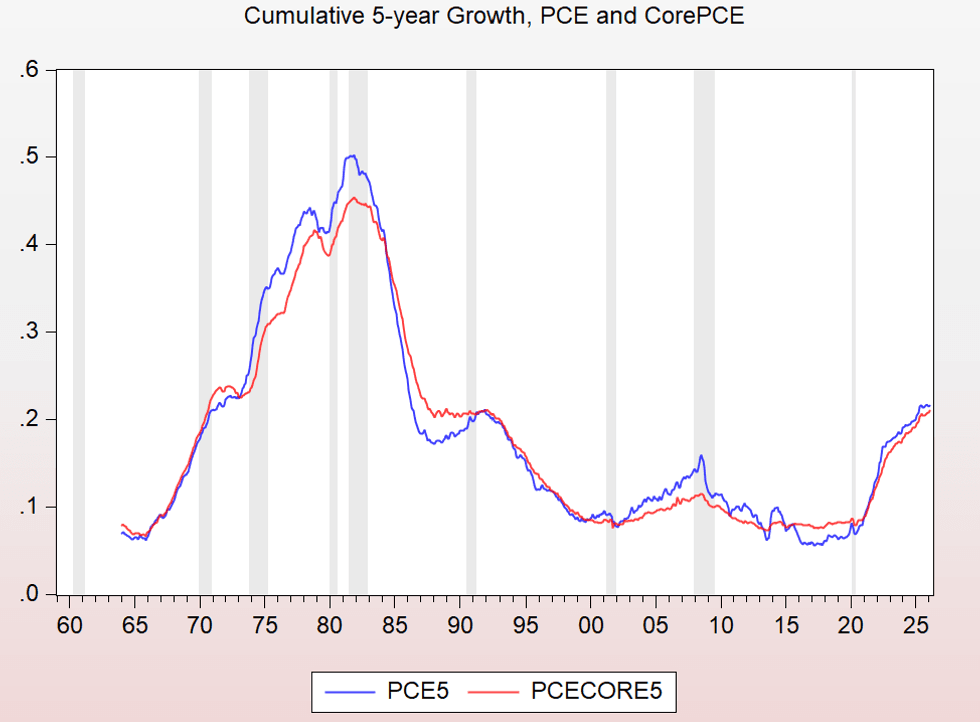

Lurking behind this is the observation that the Fed’s preferred inflation gauge, the PCE, has been above its 2% target since April of 2021, as in five years ago. I show the core PCE in the figure below, taking out energy/food spikes that the central bank can’t do much about. That persistent miss has gotta mean something, right?

A simple but not-too-far-off read of the figure above is that policymakers lost control of inflation in the 70s, Volcker lowered the boom, other inflationary forces, like oil shocks and wage-escalation clauses, became less common, and the central bank went in on “anchoring inflationary expectations,” i.e., convincing price setters it would do what it takes with its monetary policy tools to keep inflation around its 2% target.

But what then explains the not-the-70s-but-still-highly-noticeable rise at the end of the above series?

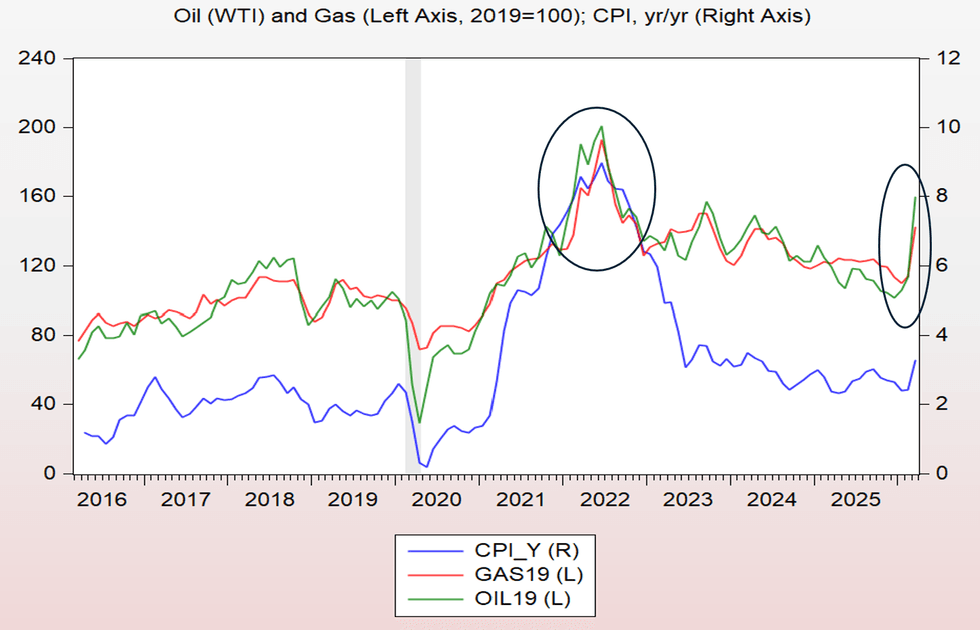

While it’s true that we’re less exposed to oil shocks, we’re clearly not immune, and we’ve had two in recent years, one of which is a big own-goal-kick by the Trump admin, in which we’re still ensconced. The other was Putin’s doing. (If you want to pause here and think about the causal linkages between authoritarian leaders and higher inflation, be my guest.) The figure shows the retail gas and oil prices (both indexed to 2019) on the left axis, and CPI yearly inflation on the right (the last data point there is the 3.3% March rate we learned of last week).

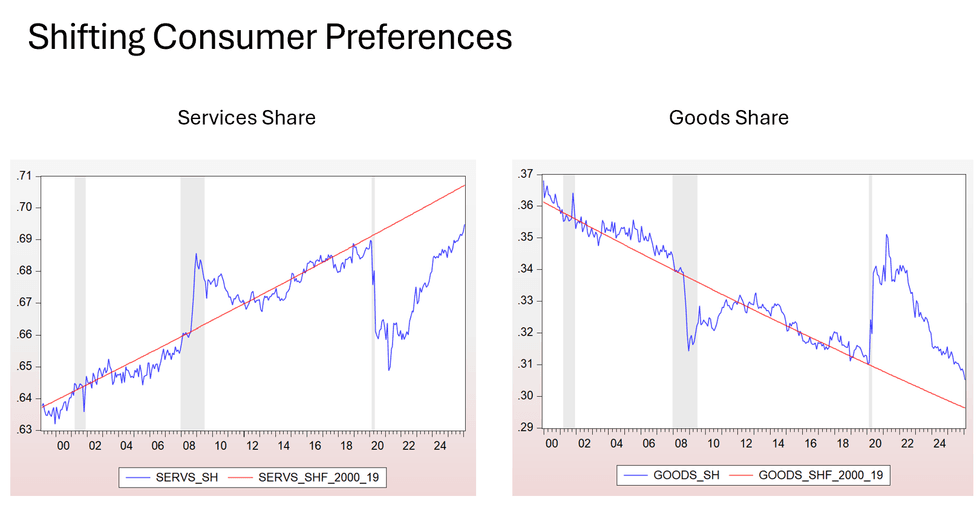

This is Neil’s piling-on point re supply shocks. Of course, the pandemic is on that list, which was a supply shock in many dimensions. Locked in by COVID, consumer preferences shifted sharply away from services and towards manufactured goods (see figure below), right at the time supply-chains were snarled, sending goods prices through the roof (I’m giving a talk this week on all this stuff, which is why I’m shoving all these slides down your throat).1

Next, enter the Orange Menace with a spate of supply shocks of his own. His and Stephen Miller’s anti-immigration actions have combined with aging boomers to take the growth of labor supply down to a drip. And again, his war is the latest supply shock, one that I do not believe will disappear anytime soon, regardless of the resolution of the ongoing negotiations.

On the demand side, I’d add Trump and Republicans' deficit-financed budget. The fact that historically large deficits stimulate the economy in both bad times (as they should) and good times (as they shouldn’t) doesn’t help in this regard.

Pushing the other way is the fact that productivity has accelerated over these very same five years, from about 1.5 percent to 2 percent—a big deal if it sticks—with potential further productivity juice to come from AI. This is a positive supply shock, typically associated with lower inflationary pressures. But that just means that half-mountain (or maybe just a foothill for now) at the end of the cumulative figure above would be steeper without this force pushing the other way.

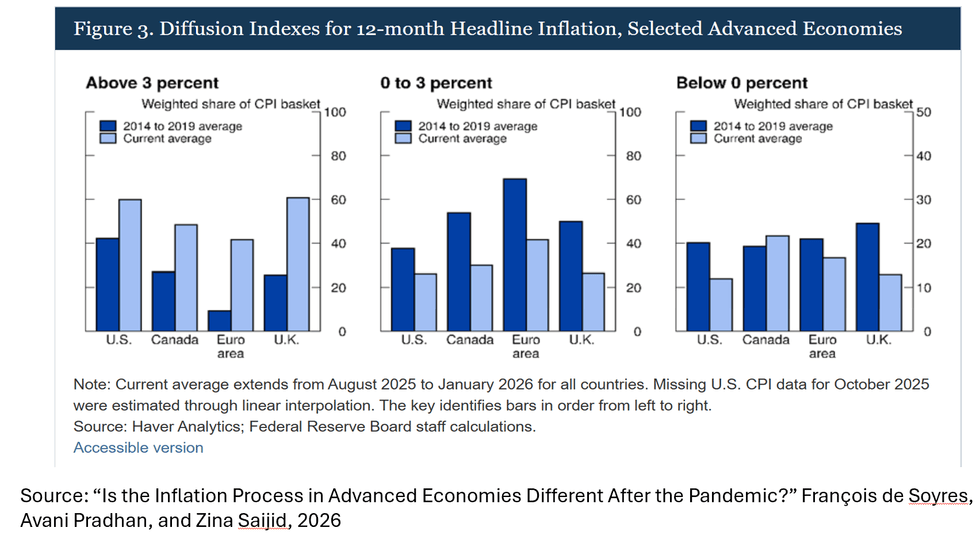

I mentioned this Fed Note that asks: “Is the Inflation Process in Advanced Economies Different After the Pandemic?” It’s a quite clear and intuitive exposition; if all this interests you, give it a read. But here’s one of its key findings:

Each bar represents the share of components within the inflation indices of the different countries that are rising >3 percent (pretty fast), 0-3 percent (pretty normal), <0 percent (deflation). As you see, more market-basket components are growing faster, and especially in the US and UK, there’s less deflation (third panel).

Case closed, right? Nope. Tariff-induced goods inflation is in play in the U.S. and housing prices, which are heavily weighted in our data, were also on a tear but have recently eased. It’s an excellent note, but it doesn’t allow us to yet conclude that we’re in a new world re higher, stickier inflation versus we’re slowly getting back to something resembling pre-pandemic inflation dynamics.

Okay, that’s a lot of data points. What does it all mean? Here’s my take:

—Inflation has been elevated since the pandemic and is currently stuck well above the Fed’s target.

—But there are bespoke reasons for that: the spate of shocks and ongoing political-economy malpractice.

—That fact means we cannot conclude that something has changed in the economy’s inflation-generation function. For what it's worth, market-based expectations of where inflation is headed are only a bit elevated.

—But we should all be worried about this. It wouldn’t be terrible if inflation settled in at ~3% instead of ~2%, assuming real wages kept up. But if, instead, the businesses, investors, and employers that set the prices of goods, services, labor, and assets think inflation is on a roll, there’s a risk of de-anchoring expectations.

In that case, the little (half-)mountain/foothill above at the end of the cumulative slide could start to look uncomfortably like the bigger 70’s mountain.

Finally, as far as American humans are concerned, as I’ve argued ad nauseum, it’s not so much inflation—the rate of price changes—that’s gotten deeply under their skin. It’s the elevated price levels, which only grow higher whether inflation is at its two percent target or elevated due to shocks or structural shifts. That said, let’s not over-torque on this blazingly insightful insight of mine (that’s self-directed snark, to be clear; “people don’t like high prices” ain’t exactly the stuff of Nobel prizes). Faster inflation pushes the price level up faster, and, as we can observe in real time, that’s pushing our econ vibes from bad to worse.

[1There’s a different interpretation of this that is compelling: it’s not that supply chains broke; it’s that this demand shift required an almost immediate widening of the pipe through which goods flow, and that didn’t happen.]

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please consider subscribing to his Substack.