Expert Warns That AI Bust Is Now Inevitable -- And Will Sink Trump's Economy

The Wall Street Journal and other industry observers keep saying artificial intelligence investment is the one thing “saving” President Donald Trump’s stock market time and again, as Trump’s economy plateaus or tanks other stocks. However, Asad Ramzanali, director of AI and technology policy at the Vanderbilt Policy Accelerator, says AI overinvestment and risky financial engineering have made an AI crash more likely.

“I started [my research] not assuming we’re in a bubble, but that if we are, we should be prepared. As I got deeper into this, I became convinced that we are in a period of overinvestment where the money going out the door in the industry, which is primarily for data centers and chips, doesn’t match the money coming in,” Ramzanali told Washington Monthly podcast senior editor Anne Kim.

Ramzanali said research shows “$2 trillion is what the annual revenue from AI will have to look like to recoup” all this investment — and that’s not what can happen in the real world. So, prep for the inevitable bust.

Companies that build data centers -- Amazon, Microsoft, Google, Meta, and Oracle -- are making estimates in the 2026 capital expenditures that promise “higher percentage of GDP than the Manhattan Project, the expansion of electricity, the Apollo space program, the building of the interstate highway system, the broadband build out in the ‘90s, everything but the Louisiana Purchase. This nets out to about $700 billion of investment this year,” said Ramazanali.

In other words, curb your enthusiasm. But tech companies now make up one third of the stock market, and banks are invested in those tech companies in big ways like private credit, structured finance and endless pools of capital all funneling into similar investments.“[W]hen you’re talking about something that is this large, this high of a magnitude of our whole economy, that’s where I start to get worried about the spillover effects into the rest of the economy,” said Ramzanali.

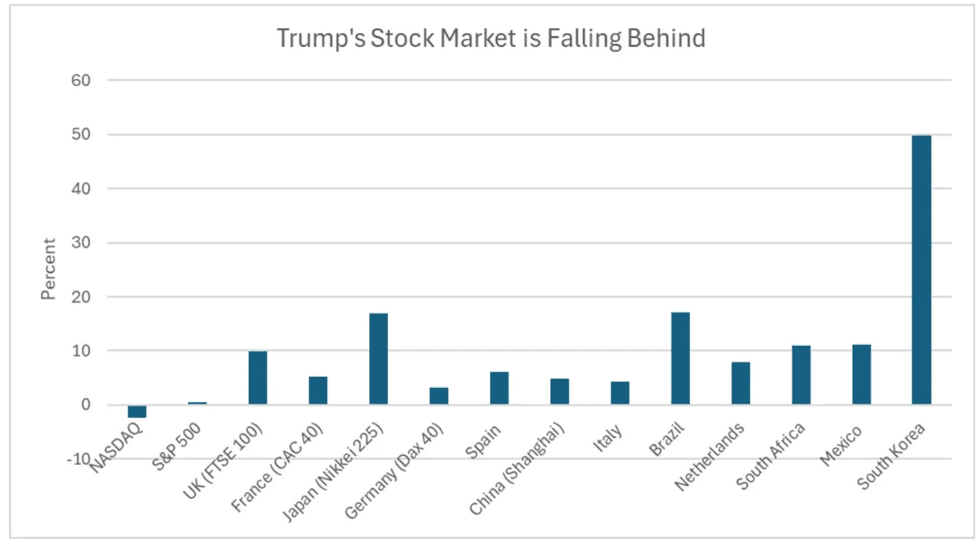

What this means for the Trump stock market — which is practically all Trump has left to brag about — is nothing good for Trump.

The New York Times reports Trumps largely steady stock market keeps assuming it “will always be saved” by the government and that markets are “not properly pricing risk, because they really don’t have to.”

“ … [But] the new rescuer investors are counting on — artificial intelligence — is vulnerable to the exact risks markets are ignoring,” reports the Times. “This has huge consequences. … This reliance on A.I. looks like an extraordinary concentration of bets” that the Times reports is “likely straining their cash cushions.”

Nobody will want to be president when the only stable stock buttressing Trump’s economy in a time of widely-fluctuating gas and grocery prices suddenly goes wobbly. And Trump has three more years for the wobble to hit him.

Source: Yahoo Finance

Source: Yahoo Finance