European Commission President Ursula von der Leyen with President Donald Truump in Davos, January 21, 2020

This year, real GDP is expected to come in at around 2.5 percent, a perfectly healthy growth rate. Last seen, unemployment was 4.4 percent, higher than I’d like but still relatively low, and real wages were beating prices by about one percent, a respectable increase in paycheck buying power. Investment in American businesses are pretty robust, especially in tech (where bubble worries persist) and the S&P 500 is up 17 percent, year-over-year.

Oh, and the President of the world’s premiere superpower is aggressively and persistently threatening to take over the territory of Greenland, an entity controlled by our NATO ally Denmark. His latest rationale is that he was snubbed out of the Nobel Peace Price.

That would be laughable—the plot of a satirical comedy for which you’d have to suspend disbelief to enjoy—had we not learned by now that he’s not kidding. He may back down; he often does. But he may not. And much else that’s transpiring due to Trump and his regime’s reckless, illegal, hateful actions are as far from laughable as you can get. Innocent people are dying with no sign of accountability.

The problem is that these two phenomenon are inversely correlated. As long as the economy trundles along okay, Trump gets degrees of freedom to ply his crazy that he’d likely lack if the economy’s wheels came off. Remember, he lost in 2020 not because of his lousy governance over most of his term, but because he blew it on COVID.

Which raises the question of how both dynamics—Trump’s increasing untethered actions and a solid overall economy—can coexist.

Here’s how Ben Casselman gets into the conundrum outlined above:

For all the chaos along the way, President Trump’s first year back in the White House is ending with an economy that looks, by most conventional measures, much like the one he inherited. Unemployment is low, consumer spending is strong and inflation is stubbornly high but gradually improving.

Tariffs, Mr. Trump’s signature economic policy, haven’t set off the manufacturing renaissance he promised, but nor have they caused the surge in inflation that many forecasters feared. The stock market bobbed and weaved its way to a solid if not spectacular 16 percent gain. Analysts who began 2025 warning of the perils of uncertainty ended it by remarking on the U.S. economy’s surprising resilience.

There are sound economic reasons for this paradox of relative economic peace amidst presidential madness.

—As I recently discussed, outside of shocks to system, like a 100-year pandemic, presidents don’t have that much to do with near-term, macroeconomic outcomes. They can make a consequential difference to who benefits and loses—cutting health care and nutritional support to help offset the cost of tax cuts tilted toward the wealthy is a germane example. They can influence near-term distributional outcomes, but less so near-term growth outcomes.

—The U.S. economy is relatively insulated from the rest of the world. Our imports as a share of GDP are 11%; for Germany, that number is 30%. Our limited exposure doesn’t fully block the corrosive effects of Trump’s tariffs, which are clearly implicated in the difficulty our manufacturers are facing—they’re basically in a recession, with employment down 68,000 last year alone. But it’s one reason why the tariffs’ inflationary impact has been limited to around half a percentage point so far.

—Near-term boost, longer-term drags. The word “corrosive” above is operative. The deficit-financed tax cuts from big, dumb budget bill are expected to juice growth this year, but even long-term budget doves like myself worry that they’re already putting upward pressure on interest rates. And when you're carrying $30 trillion in debt (100 percent of GDP), each new point on the rate is $300bn in debt service.

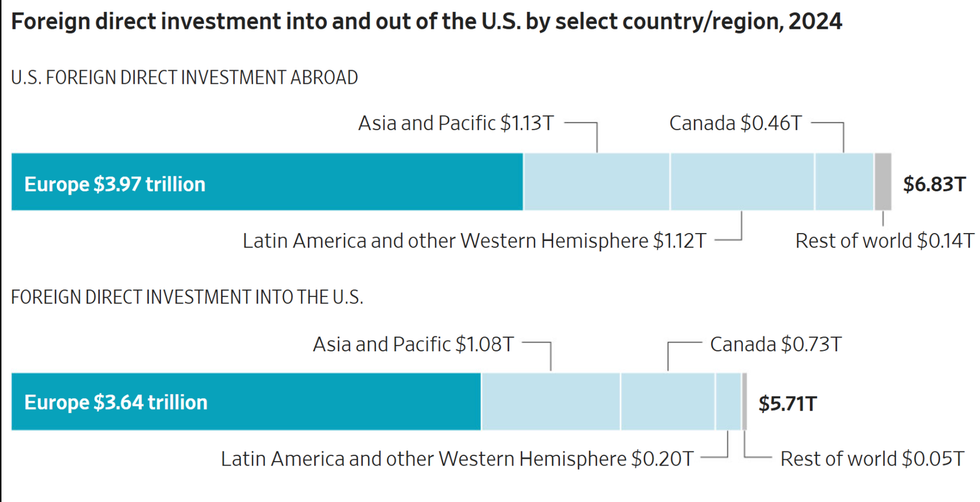

—Another source of longer-term corrosion is, of course, the deterioration in America’s relationship with the rest of the world. As you probably know, Trump is threatening more tariffs on those EU countries who have stood up to him on Greenland, giving rise to talk of EU retaliation. In fact, the European bloc is our largest trading partner, the destination for most of our foreign investment as we are the same for them. They purchased almost $300bn in US services exports in ‘24, making them the largest contributor to the US service-trade surplus. These are just the economic costs of Trumpian isolationism, but the point is that while these cross-border investments and trade flows don’t shift on a dime, they can and do shift.

Source: US Commerce DepartmentChart by Andrew Barnett/WSJ

Source: US Commerce DepartmentChart by Andrew Barnett/WSJ

—It is still too soon to tell if Trump will be able to undermine the independence of the central bank, which has continued to perform important technical work in the background, helping to support the economic expansion (I’ll be paying close attention to the Lisa Cook case argued in SCOTUS tomorrow). Should he get the power to implicitly takeover the Fed (by loading it up with those who will do his bidding), longer-term growth will suffer.

For what it’s worth, which ain’t nothing, global financial markets appear to be waking up this AM to the fact that Trump may be serious about trade-war escalation. Bond selloffs in Japan are now hitting here as well; the 10-year yield is back up to 4.3 percent, its highest since last September. Equity markets are poised for a big negative open. Trump himself is on his way to the Davos Economic Summit, where global elites meet to schmooze in the Alps. Awkward, right??!!

There are at least two big questions posed by these current events. First, can the damage this presidency is creating be stopped before the broader negative outcomes kick in, and two, is the damage repairable?

I have more faith in question two than one. There are simply no grownups in Trump’s immediate orbit, in no small part because they’re not allowed in the room. Republicans are useless; they not only fail to constrain his actions, but they happily turn over the keys. I don’t see how they face their constituents, at least the non-MAGA ones, or for that matter, how they can accept their paychecks with a straight face. They’re not doing anything other than violating their oaths of office.

But history tells us repair is possible. Our nation has come back from worse than this. That said, such history is only valid if the center holds, meaning democracy remains intact enough to have elections that banish the barbarians from the castle. As I see it, that’s our only way out of this mess, and there is a lot that can happen to threaten that existentially important outcome between now and then.

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please consider subscribing to his Substack.

Reprinted with permission from Econjared.

- 'Trump Slump': Tariffs And Imperial Attitude Are Killing Tourism Industry ›

- Worse Than Fascist: What Is The Word That Describes Trump's Conduct? ›

- Vought's 'Aggressive' Gutting Of Government Enrages GOP Senators ›

- 'The Apprentice' Producer Regrets Helping To Create 'Monster' Trump ›

- The Impotence Of Drill, Baby, Drill: Why Oil Prices Soar Despite Domestic Supply - National Memo ›

- Surprisingly, Even (Some) Republicans Understand Trump Deficit Peril - National Memo ›

- Donald Trump's return to office: Ten consequences | Centre for ... ›

- Trump's Executive Orders Mean Real Damage to U.S. Economy ... ›

- Trump's Ukraine summit was a European damage control operation ... ›

- Trump's threatened tariffs projected to damage economies of US ... ›

- President Trump's First 100 Days: Attacks on Human Rights, Cruelty ... ›

- Tracking the Trump Administration's Harmful Executive Actions ... ›