Federal Reserve Chair Kevin Warsh with President Donald Trump at the White House

I found the new Fed chair’s debut to be fascinating, comforting, and worrisome. Which is in itself interesting because Chair Kevin “Taskforce” Warsh (“Task” for short) talked a lot but said very little of note. Here are my takeaways.

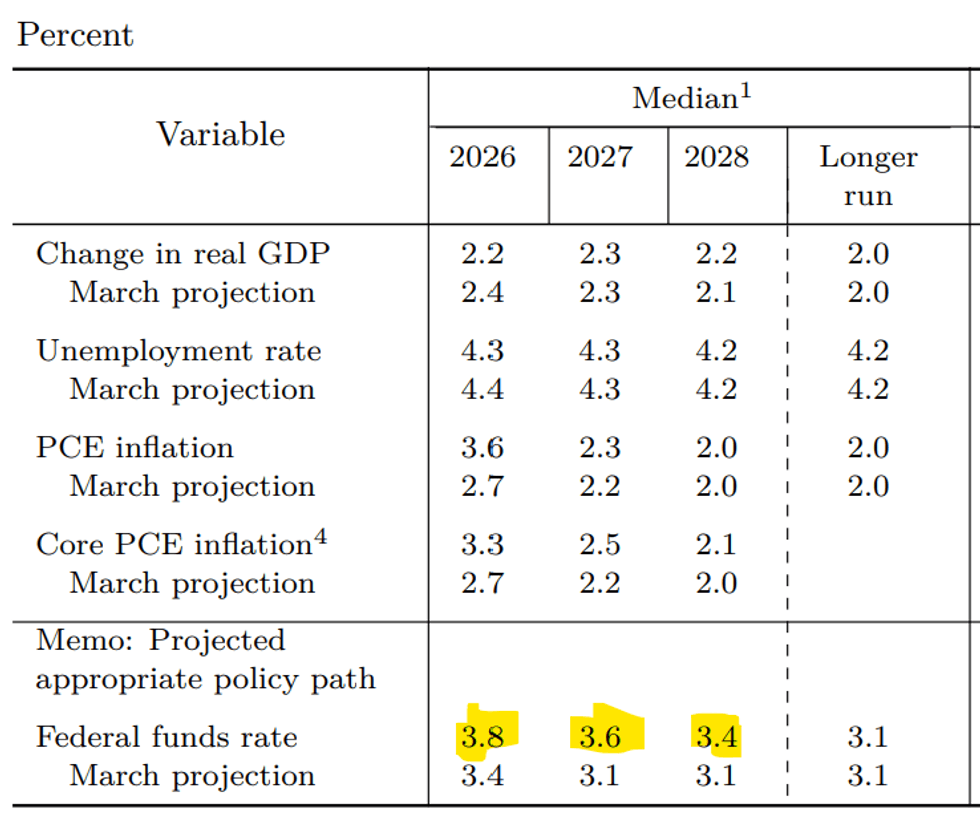

What did the committee do? Not only did they hold rates steady, as expected, but there was a more hawkish tilt to their expectations re future rates. Compared to their last meeting, the committee expects the interest rate they control to be higher both this year and next.

This change can be seen in the “dot plot” wherein the 19 committee members anonymously say where they think rates will need to go. Except there were only 18 dots for ‘26 and ‘27 and 17 for ‘28. Chair Warsh told us he’d abstained and someone else apparently joined him for ‘28.

I’ll have more to say about his abstention in a moment, but this hawkish tilt takes me to my next point.

I said “worrisome” above. Why? The theme of the statement, the dots, and Warsh’s presser were all, quite reasonably in my view (this was part of the comforting part), about how the economy and labor market are doing pretty well, but inflation remains high and sticky. Even with Trump looking over his shoulder, Warsh would have been hard pressed to oppose the committee’s neutral/tightening bias. That’s just where the inflation data are right now.

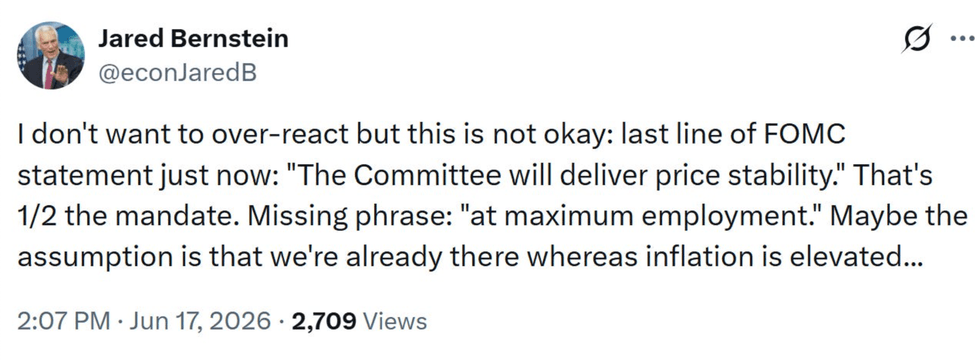

But “Task” isn’t new to this neighborhood, and I’ve long argued he just played a dove to get the job. That’s why I was struck—and maybe kinda over-reacted—to the FOMC statement a few minutes after its release:

The rest says: “...so no need to got there. But knowing Warsh's proclivities in this regard, I don't like it.”

Here’s why we should be nervous that Warsh will consistently down-weight the full-employment side of the mandate relative to the price-stability side:

—He’s long been a hard-money guy who worries more about inflation eroding asset values than unemployment eroding bargaining power and paychecks.

—He barely referenced the employment side of the mandate in his confirmation hearing.

—He hired Paul Winfree to be a temporary adviser as he settles into the new gig. This is the guy who wrote the (generally bonkers) Fed chapter in Project 2025, which calls for getting rid of the full employment part of the mandate.

Like I said, this concern isn’t new, and I tend to overreact when I think someone is threatening full employment conditions—a personality flaw for which I emphatically do not apologize. But this potential bias bears close watching.

What else did I find comforting? That would be the fact that Warsh didn’t come out swinging, going off on his colleagues for their tightening bias, signaling Trump, as Stephen Miran did, that he would push for cuts, regardless of the data. He praised his FOMC colleagues and the staff, and was generally highly diplomatic.

Now, if readers who know my proclivities conclude that my comfort should be Trump’s discomfort, I agree. This was a hawkish meeting, more so than expected, and Warsh went along with it. If Powell did that, Trump’s thumbs would have been spewing fire on social media, but he held his fire yesterday.

I took this as a win for Fed independence, but it’s way too soon to conclude that we’re safe in that regard. Still, you know my mantra: A bad day for Trump is a good day for America.

Anything else from the debut? Yeah, a few things.

—I’ve argued in recent posts that I take Warsh’s point how an excess of Fed communication isn’t helpful and can be harmful, leading markets and Fed watchers to overreact to stray voltage. But after yesterday, I’m worried he will push that too far, providing too little information in ways that could lead to unnecessary volatility and the return of the Fed-guessing-game that “forward guidance” was designed to end.

The statement was too bare bones, I thought, and Warsh wouldn’t answer any questions about where he thought things were headed, providing us no information on his “reaction function,” meaning how he and FOMC are processing the data with regard to rate movements. Whenever he was asked a question about this, he told us that he’d be setting up a taskforce to look into that. It became a comic tag line.

I doubt I was the only one who missed Powell’s plain speaking, his earnest efforts to clearly explain how he and his colleagues were thinking about things. In a word, Warsh was really quite opaque, and if that continues, it will generate problems born of insufficient communication.

—I’ve been to this taskforce rodeo many times, and have even led one or two. The majority of taskforces do little; they’re set up to give the appearance of doing something about a problem for which you don’t have a tractable solution. Some, however, yield important, actionable results. My prior in this case is that most of the many taskforces that Task announced yesterday won’t change much, with the exception of the communications/forward-guidance one.

That’s enough for now, and we’ll have ample time to scrutinize the new chair. I’m glad he didn’t come out swinging and I appreciate the seriousness about getting inflation back to target, especially with Trump lurking in the background. But I’ve got serious concerns that warrant close watching.

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please subscribe to his Substack, from which this is reprinted with permission.

- Warsh's Answer About The 2020 Election Disqualified Him As Fed Chairman ›

- Warsh Case Scenario: A Bad Heir Day For The Federal Reserve System ›

- Fed Chair Confirmation Hearing Raises Grave Concerns About Nominee Kevin Warsh ›

- Fun Times Ahead! What Kevin Warsh Can Expect At His First Fed Meeting ›

- Behind Tomorrow's Federal Reserve Decision, A Delicate Economic Balancing Act - National Memo ›

- Here are the five big takeaways from Kevin Warsh's first meeting as Fed chairman ›

- Fed meeting recap: Warsh announces task forces to overhaul major Federal Reserve operations ›

- Fed leaves interest rates unchanged but signals higher rates are ahead | CNN Business ›

- Fed Holds Rates and Leans Toward Fighting Inflation With Future Increases - The New York Times ›