Don't Expect Foreign Nations To Pay Trump's Tariffs (They're Still A Tax On You)

As we all know, Donald Trump likes to play the tough guy. Unfortunately, he often does it in really foolish ways, and this time I’m not talking about his war against Iran.

I’m talking about Trump’s tariffs. From the way he talks, he seems to think that foreign countries are sending us checks equal to the tariffs he has imposed on U.S. imports from them. Donald Trump’s mind can be a scary place, so it’s not worth trying to tease out his thought process, except to point out that the idea that foreigners are sending us checks is absurd.

The tariffs are collected here when the goods show up at a customs office. The party paying the tariff most immediately is the importer. The importer could be a wholesaler who may resell it to a retail store, manufacturer, or other business. Or in many cases, it will be a larger retailer like Amazon or Walmart, who arrange for the imports directly.

Either way, it is someone at this end who is most immediately out the money for the tariff. Some of what they pay will be passed on to their customers. To some extent, they will be forced to eat the tariff and make lower profits. (The evidence is that most is passed on.) But in both cases, consumers or companies here are paying the tariff.

The only way that foreign countries would pay the tariff is if the price of the goods they export to the United States falls as a result of the tariff.

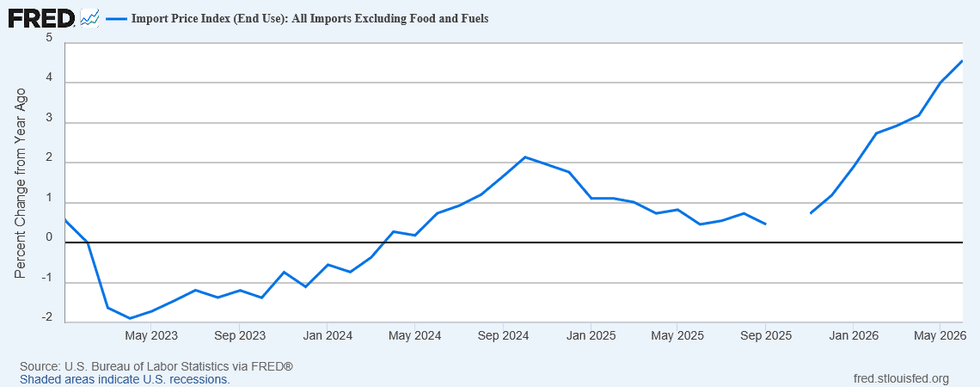

We got new evidence on that story on Friday, as the Bureau of Labor Statistics released data on import prices for June. The release showed non-fuel import prices were up 0.4 percent in June and 4.2 percent year-over-year (YOY).

Just to be clear on what these numbers mean, these are prices before any tariffs are applied. That means if the average tariff rate is 10%, then we are paying 14.2 percent more for our imports in June of 2026 than in June of 2025. That doesn’t look like a story where exporters are eating the tariffs.

It is worth noting that this is a change from past patterns. Import prices were actually falling in 2023 and rising slowly in 2024. There are a variety of factors affecting the price of producing goods elsewhere, including Trump’s war in Iran, but in any case, the story with import prices looks worse than before Trump took office, even before we consider the impact of the tariffs.

Looking across countries, it is hard to find evidence that anyone is eating Trump’s tariffs. The price of imports from the EU is up 3.7 percent YOY. The price of imported manufactured goods from Canada is up 10.3 percent. And the price of goods from China is up 1.3 percent.

While the story should have already been clear, the new data just further shore up the case. When Trump threatens countries with big tariffs, he is threatening the American people with big taxes.

This point should be made more clearly in reporting. For example, it is misleading to say that Trump is threatening to hit Brazil, Canada, or whoever with new tariffs. He is threatening to impose taxes on goods that Americans import from these countries. That would make it clear what is at stake.

We may never know, or care, what is in Trump’s head, but we have never seen a president who is so happy to raise people’s taxes.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.