Ceasefire! What Might This Mean for the Strait, the Markets, and You

As I suspect you’ve heard, a two-week ceasefire appears to be in place in the war with Iran. That is unequivocally good news, though no one paying attention can breath anything like a sigh of relief, despite the relief rally going on this morning in equity markets, with West Texas Intermediate oil down ~$20 as I write this (which will have moved by the time you read this).

There are more questions than answers and for the (scant) details as we know them, go to any news source you trust. But here are my quick impressions. Hovering over all of them are “What was that for? What did thousands of people have to lose their lives for?”

Let me be unequivocal about this. I’ll be very happy if the parties in this conflict can find the offramp they appear to be seeking. But I fear this will be no occasion for celebration. Iran’s hardline theocracy remains in place, and worse, appears ready to continue their operation of turning the Strait of Hormuz into a tollbooth, which would be a massive cash cow for them. If you’re thinking “the U.S. would never let that stand!” you might be right, but that could well mean the ceasefire ends and the conflict restarts.

My top priority is that nobody else gets killed because of Donald Trump and Benjamin Netanyahu’s aggressions. But I don’t celebrate the arsonist who puts out the fire he started.

With that, a few impressions of where we are. They talk about the fog of war, but what I’m about to try to see through is the fog of this ceasefire, with an econ-more-than-a-geopolitical angle.

—Feeling the Blues in the Strait of Hormuz: A key Iranian condition for the ceasefire is that "safe passage through the Strait of Hormuz will be possible via coordination with Iran’s Armed Forces and with due consideration of technical limitations."

This is bad. To me, and to some press reports, it reads like they’ll ramp up their control of who transits (relative to pre-war), possibly with a cap on traffic, and with a toll (the number $2 million per vessel has circulated for a while).

We don’t know how private shippers will respond, but what choice do they have? At least in the medium term, there's nowhere near enough supply-chain alternatives to move product out into the globe. If this is broadly correct, and if this condition stands, it suggests that a new, post-war SoH transit premium will be added to the price of oil and other goods coming through the Strait, one that will continue to be passed forward to consumers.

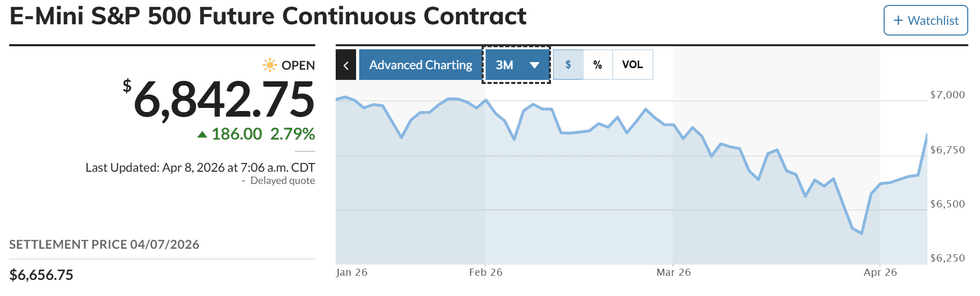

—The Way We Were: Will Markets/Oil Just Revert to Prewar Levels/Trends? Unknowable, but, at least re oil, not if the aforementioned premium kicks in. Equity markets, though they trended down toward correction territory, broadly expected Trump to back down, so the relief rally is solidly underway as I write this AM: Here’s the S&P pre-opening futures:

Gas is up this morning ($4.16/gal), and if the oil decline sticks, we’ll have a real-time test of the old rockets/feathers dynamic, where the gas price takes the elevator up and the stairs down.

I’m not in the biz of predicting where markets will go but if the result of this war, as some are predicting, is to crimp the existing supply chain of fossil fuels, it would raise prices and dampen global growth at some margin. But it could also stimulate new activity to find workarounds to this obviously dysfunction choke point, and put more wind power in the sails of renewable energy development. (You know my views on this: as I said to Shalanda Young yesterday, if I were in charge, I’d do the Canadian Shuffle and allow a nice bunch of Chinese EVs into the US, conditional on some degree of tech-transfer and joint production.)

—Will It Stick? I find the fact that the Trump administration is apparently allowing Iran’s 10-point plan to be a starting place for ceasefire negotiations to be very surprising and a symbol of how desperate Trump is for an offramp. He’s gone from promising to end their civilization at 8pm ET to “sure, we’re cool with sitting down to chat about you keeping your nukes and controlling the Strait.” You’ll see what I mean if you look their list.

I’ve been following Tobin Marcus from Wolfe Research on these matters, who writes this morning (with Chutong Zhu):

If the US were outright accepting Iran's 10 points as they're now being reported, this would be a huge surprise and a massive concession, with the US accepting various Iranian red lines and giving up on our own, including on the nuclear file. On the other hand, if defining the 10 points as a "basis for negotiations" does not imply acceptance of those points, then it's unclear how close the two sides really are in the ongoing negotiations. It's a little hard to believe that Trump is accepting anything like Iran's 10 points, and the WH seems to be telling Israel we're doing nothing of the sort, so we lean toward interpreting this as intentional wiggle-room to facilitate an offramp, which raises questions about the likelihood that the next two weeks of negotiations will actually culminate in a permanent deal.

In other words, there’s a tension between Trump’s usual play—break something, declare victory, move on to breaking something else—and accepting what should be unacceptable. And it is impossible to know at this point how that balances out. If you pushed me to take a side, I’d guess he’s more likely to mush up some version of pushing back on the most egregious Iranian conditions and turn tail outta there.

—What Does All This Mean For Regular Folks Just Trying to Go About Their Lives? As you know, this is always my touchstone up in here. Assuming the ceasefire sticks, Strait of Hormuz traffic picks up, and the oil price falls at least part of the way back to its prewar level, the gas price should slowly come down, much as we predicted here. That still cuts meaningfully into real disposable incomes, and, as I’ve been worrying about, lower real wage gains. I’m watching carefully to see how the March headline CPI, out Friday, compares to the most recent pace of mid/low wage growth of 3.4 percent.

But more broadly, for folks just trying to make ends meet, this misadventure in the Middle East is yet another Trumpian own goal kick in their faces. The Trump tariffs, the Trump budget, the Trump war—they’re all making life more expensive for people, which is especially ironic given that those people will tell you that their main economic concern is affordability.

And never forget the opportunity costs: if you’re spending all your time making things worse, you’ve squandered the time you could have spent making things better. Imagine that instead of negotiating a 10-point plan that gives the Iranian regime what they want, we were negotiating a 10-point plan for affordable housing, childcare, and healthcare.

I’ve said it before, including yesterday, so sorry—not sorry—for being repetitious. But any Democrat who seeks to retain and win office that isn’t working to operationalize that contrast needs to immediately get out of the way and make room for someone who will fight their a— off on behalf of these priorities.

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please consider subscribing to his Substack.

Reprinted with permission from Econjared.