Unrig The Bankruptcy Laws That Privilege Super-Rich Private Equity Oligarchs

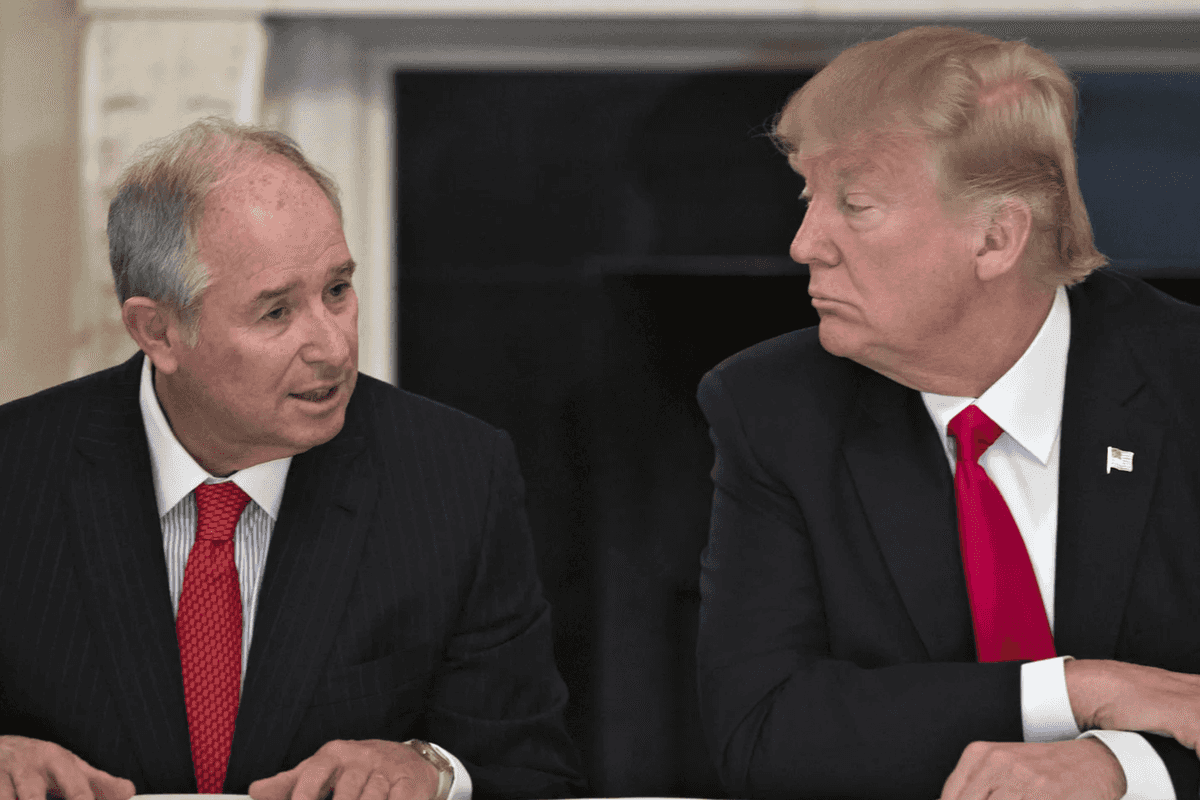

Blackstone CEO and Trump adviser Stephen Schwarzman with President Donald Trump

In 2017, Toys R Us, the nationwide toy store chain, filed for bankruptcy. It had $800 million in unpaid bills: money owed to lenders, suppliers, and workers. While Toys R Us didn’t have the assets to make good on these debts, the private equity (PE) firms that owned it, Bain Capital and KKR, had plenty of money. But because of the way we structure the bankruptcy laws, the assets of the PE firms could not be touched by the creditors of Toys R Us.

The story of this bankruptcy is not unusual. While it is larger than most, bringing companies to the edge of bankruptcy, and often over the edge, is the standard way PE companies operate. They routinely strip the assets of companies they take over, typically selling any real estate they own, including the buildings that a store, restaurant, or hospital operates in. They also pay out dividends to the PE firms from any cash that the company has on hand. And they will often have the company issue new debt to pay dividends to the PE firm.

The asset stripping and dividends paid from new debt often is sufficient to fully pay back the PE firm for their initial investment. At that point, the PE firm is in a no-lose situation. If the company is still viable, the PE firm can take it public and make a healthy profit. If it’s not viable after the asset stripping and new debt, the PE firm just puts the company into bankruptcy and walks away. Its debts are not the problem of the PE firm.

There is nothing natural about this arrangement. We could make PE firms that control other companies liable for their debts. (Massachusetts Democratic Sen. Elizabeth Warren proposed doing this in a bill a couple of years back.) This is not a government intervention in the market; it is simply changing the rules on how the government structures the market. The current bankruptcy law is no more natural than a law that makes PE firms liable for the debts the companies it controls accrue. It’s just more friendly PE firms.

We can change the bankruptcy laws for corporations just like we did for individuals a couple of decades back. At that time, the law was made harsher for debtors. Not only did this hurt many struggling families, but there was so little concern for the “natural workings of the market,” that Congress had no problem applying the new rules retroactively. People who borrowed under the less punitive bankruptcy regime were required to repay their loans subject to the more stringent rules Congress put in place in 2005.

Bankruptcy law is not the only place where Congress has structured the law to be friendly to PE. Most of the pay of PE partners is taxed at the 20% capital gains rate, instead of being taxed at the 37% rate for normal income for high-income earners. This is because the partners classify their earnings as “carried interest.” This is essentially commission pay, sort of like what realtors and shoe salespeople get, except those workers have their commission pay taxed at the same rate as ordinary wages.

People concerned about inequality should be paying attention to the way we structure the market to redistribute money to PE partners. Many of the richest people in the country got their money from PE. Steven Schwarzman, the CEO of Blackstone, is estimated to have a fortune of around $40 billion. George Roberts, the co-founder of KKR, is estimated to have $15 billion, as is Leon Black, the co-founder of Apollo Global Management.

There are efforts in the United States and elsewhere to impose wealth taxes to get back some of this money. Perhaps they will be successful, but these people are pretty good at using legal loopholes and hiding their money. In any case, it seems a much better route to not structure the market to give the rich enormous fortunes in the first place. That can be done, if anyone cares.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.