Will Surrendering To Iran Relieve Trump's Gas Pains? Alas, Probably Not!

Donald Trump’s rhetoric on Iran oscillates wildly from day to day, sometimes from hour to hour. But Trump has run out of military options that don’t involve huge war crimes, so we seem to be heading for a reopening of the Strait of Hormuz on Iran’s terms. And that includes the imposition of de facto tolls, whatever they are called.

There is no mystery about Trump’s surrender: He’s desperate to end the war because he is paying a steep political price for high gasoline prices, and the midterms are only four and a half months away.

But can Trump rehabilitate his standing with American voters by throwing in the towel? Probably not, for both economic and political reasons. I would argue that there are four points of slippage between Trump’s political goals and what is likely to happen.

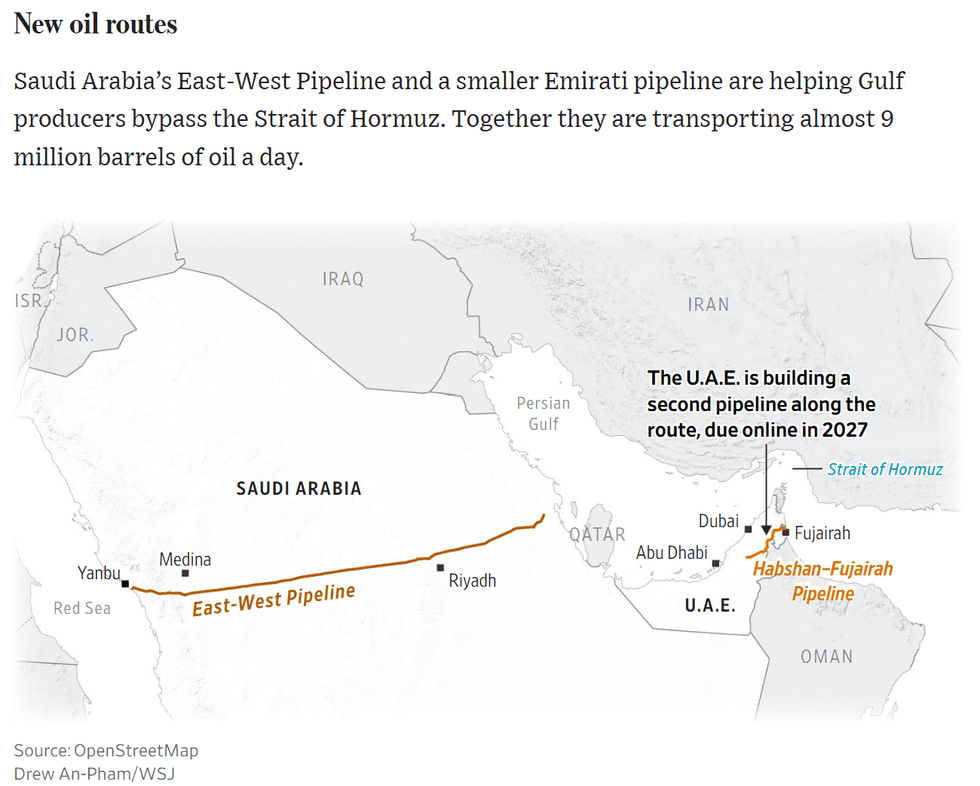

The state of the Strait: Even if the war is truly over, it will take time to return world oil supplies to normal levels. First, there has been substantial damage to the Persian Gulf’s infrastructure, which will take months, if not years, to repair. Second, many oil tankers are now in the wrong place and it will take weeks or months to move them. Third, some shipping channels are at risk from stray mines. Lastly, the world met the Hormuz crisis in part by running down oil inventories, which will now need to be rebuilt.

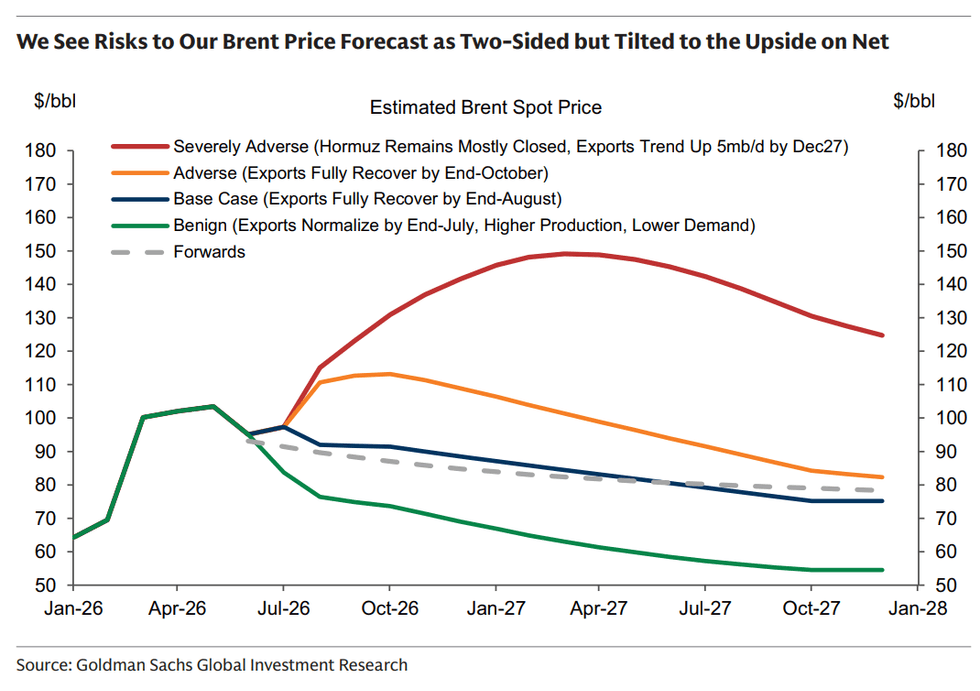

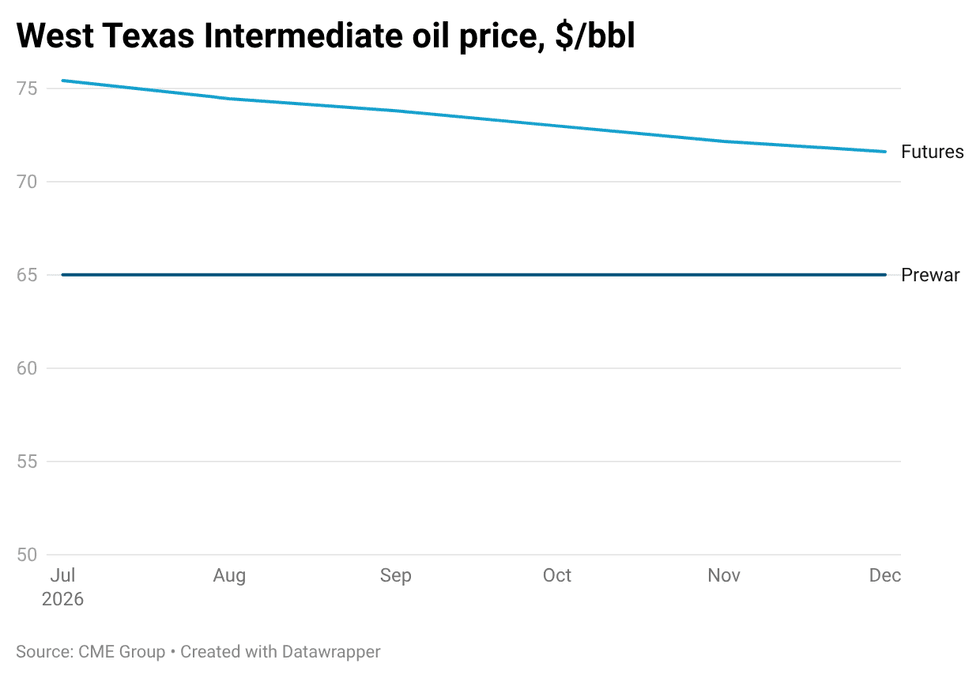

It’s true that a surge in Iranian oil exports has begun thanks to the lifting of the U.S. blockade. This will add to global oil supplies but will also strengthen the regime. But despite this surge of Iranian shipments, prices of oil futures — promises to buy or sell oil on specified dates — indicate that the oil markets expect oil prices to decline at only a slow rate for the rest of this year:

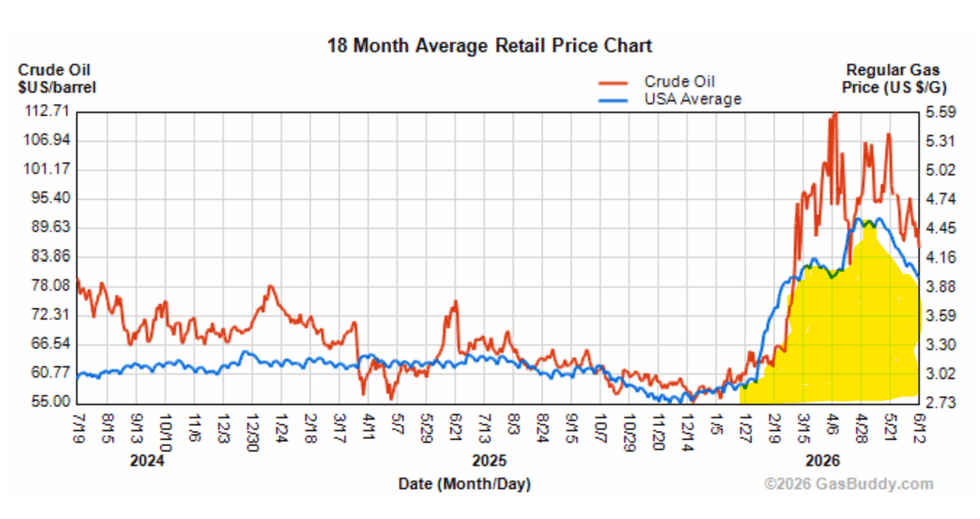

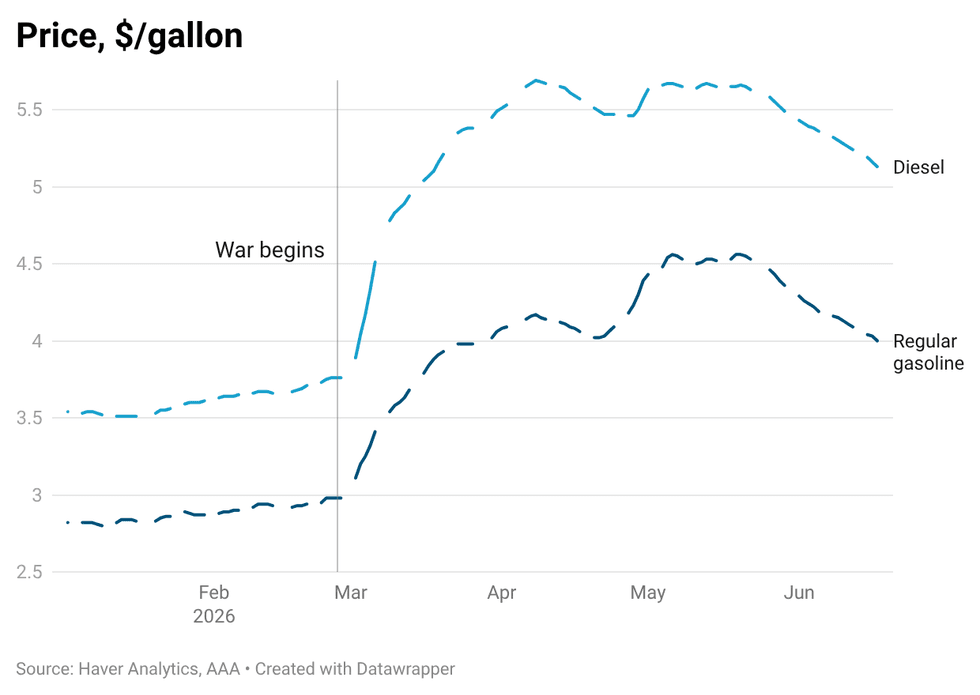

Rockets and feathers: There is a well-documented pattern to how the price of gasoline responds to changes in the price of crude oil. When there is a global shock that causes the price of crude oil to soar, gasoline prices rise like a rocket. But when the crisis is over and crude prices plunge, the price of gas declines only gradually — it drifts down like feathers.

Will that happen this time? Gasoline and, to a lesser extent, diesel, have fallen considerably in price from their peak:

They are, however, still well above their prewar levels, and by more than you would expect given the commonly used rule of thumb:

$10 on price of crude = $0.25 on price of gasoline

Crude oil prices are $10-$15 a barrel higher than they were prewar, which would point to gasoline prices $0.25-$0.37 higher per gallon. Yet gasoline is currently almost $1 a gallon higher than it was before the war.

So if the “rockets and feathers” pattern continues to apply, gasoline prices will be elevated for months to come, thwarting Trumpist hopes of quick political relief from capitulating to Iran.

Prices beyond gasoline: As you can see in the chart above, the war on Iran sent the price of diesel fuel soaring by significantly more than the price of gasoline. Unlike gasoline, which is mainly purchased by consumers, diesel is mainly used by businesses, for trucking and industrial uses. So the surge in diesel prices led to a surge in business costs rather than a direct burden on consumers.

True, businesses do eventually pass higher costs on to consumers. The key word, however, is “eventually.” This means that there is probably substantial Iran war-induced inflation still in the pipeline.

Nor were soaring prices of diesel the only cost the war imposed on businesses. The Persian Gulf is normally a key supplier of many chemicals, whose prices soared when the Strait of Hormuz was closed. For example, the price of urea, a key fertilizer with industrial uses as well, temporarily rose by 75 percent when the Strait was closed. Again, some of the effect of these cost shocks still hasn’t hit consumer prices.

Moreover, the economy is delivering inflationary shocks independent of the war. Notably, the AI/datacenter boom has driven a rapid rise in electricity prices and huge increases in the prices of memory chips, which are used in almost all consumer electronics, from smartphones to laptops to game consoles. The AI boom has also pushed up interest rates on mortgages and consumer loans. Oh, and Trump’s cuts to Obamacare subsidies are causing many Americans’ health insurance costs to soar.

So while consumers are getting some relief at the gas pump, they’re facing persistent sticker shock on many other goods. It’s safe to predict that consumers won’t be in a celebratory mood on D-I [defeat by Iran] Day. Instead, they are likely to feel that any claims of victory are Pyrrhic at best.

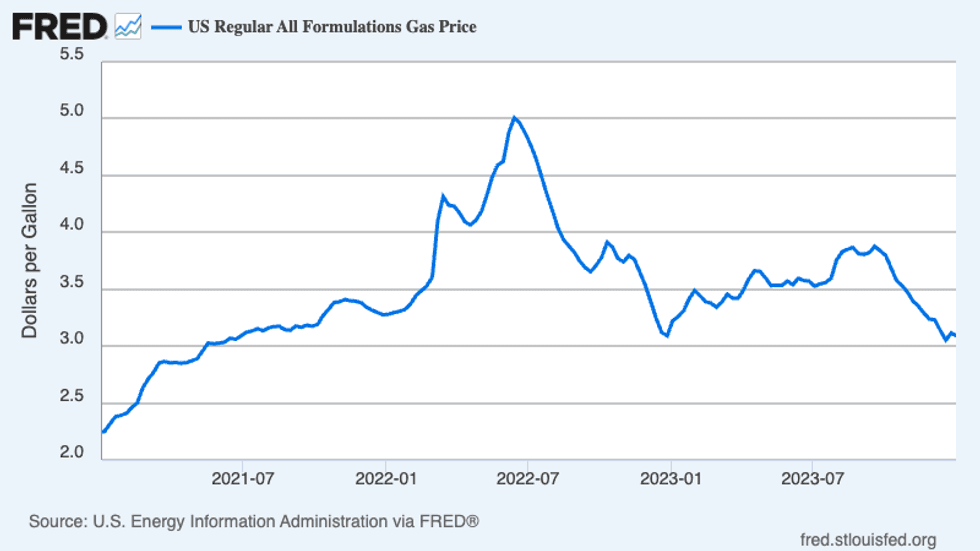

The cost of broken promises: We have just endured the second big gasoline price shock of the past five years. The previous shock, during the Biden years, briefly sent average prices of gasoline above $5 a gallon. Like the recent price spike, the 2022 run-up in gas prices was largely caused by a war — the war between Russia and Ukraine. That wasn’t a war that the U.S. president launched on a whim. Regardless, the price of gasoline fell rapidly after June 2022:

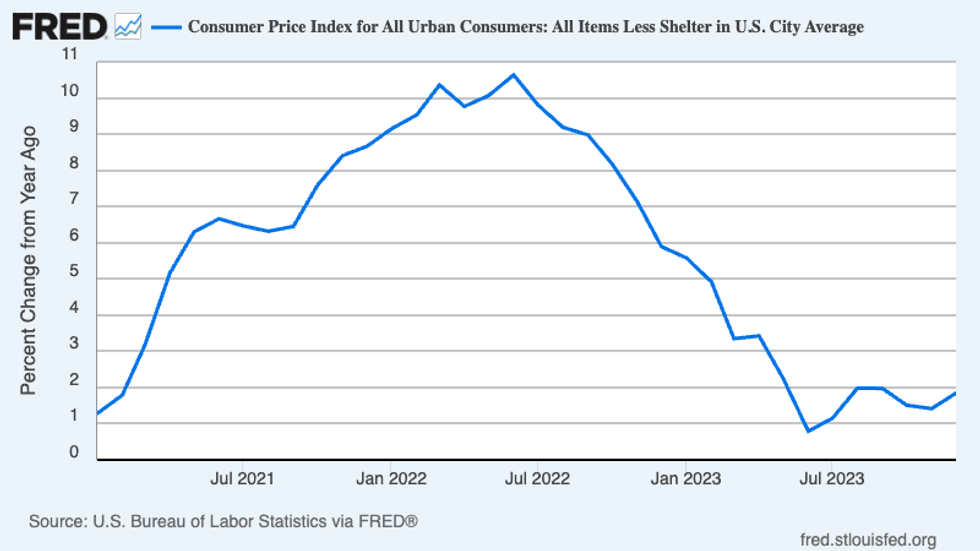

Inflation also fell rapidly, especially if you exclude the price of shelter, which as measured tends, for technical reasons, to lag far behind market prices:

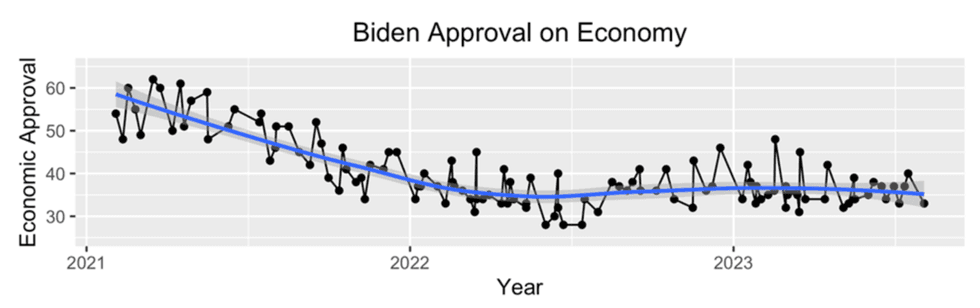

So what did cheaper gas and rapid disinflation without a recession do for perceptions about President Biden’s handling of the economy? Almost nothing. The Roper Center published an analysis of trends in Biden’s economic approval rating, and found hardly any improvement when gas prices and overall inflation plunged:

You may argue that this was unfair because Biden was punished for a global inflation shock that wasn’t his fault. Furthermore, his overall economic management was in fact very good. In fact, that’s what I have argued, and a majority of Americans now say that the economy was better under Biden than under Trump. However, that argument is beside the point for analyzing the effect of the Trump surrender. The point, instead, is that once a leader has lost the public’s economic trust, that trust doesn’t come back just because gasoline prices have receded.

I would add that it may be especially hard for the Trumpists to make the case that things have turned around when they were never willing to admit that anything was wrong in the first place, insisting even as prices soared that we were living in a “golden age.”

So will Trump’s surrender to Iran rescue him and his party from a blue wave in November? It’s very unlikely. I suggest they find themselves some lifejackets.

Paul Krugman is a Nobel Prize-winning economist and former professor at MIT and Princeton who now teaches at the City University of New York's Graduate Center. From 2000 to 2024, he wrote a column for The New York Times. Please consider subscribing to his Substack.

Reprinted with permission from Paul Krugman.