Destroyed civilian buildings in Teheran after US bombing

Any commentary on the costs of this or any other war must begin by recognizing that paying more at the pump means nothing compared to the loss of thousands of lives, including civilian lives, that have occurred thus far. That is the true cost of war. And, in the case of this war, a war of choice we entered due to the terrible judgement of an unchecked president whose self-confidence is matched only by his ignorance of the history of the region, we can all be forgiven, once this is over, for asking the question, “for what?” Why did all those people have to die? What goal was served, beyond assuaging Trump’s whims?

The Human Rights Activists News Agency said at least 1,598 civilians had been killed, including 244 children, in Iran since the war began. Lebanon’s health ministry said that more than 1,260 Lebanese had been killed as of Tuesday, with more than 3,750 others wounded, since the latest fighting between Israel and Hezbollah began. In Iran’s attacks across the Middle East, at least 50 people have been killed in Gulf nations. In Israel, at least 17 had been killed as of Friday. The American death toll stands at 13 service members, with hundreds of others wounded.

It’s a big jump from these existential concerns to gas et al prices, but those matter too. They matter because people were already, pre-war, struggling with affordability issues, but they also matter for political reasons. Even if you have different answers to the questions I pose above, as I know some readers will, the information about the economic costs of the war must be promulgated, especially as the White House’s misinformation machine is always running at full tilt. With this administration, affordability voters—a decisive bloc—should be aware that Trump is here again pushing hard in the wrong direction.

I should note before I jump into the data that markets have been optimistic on Trump pulling out of the war. The thinking was that he would declare victory and spout off on how this is now Europe’s problem.

“You’ll have to learn how to fight for yourself, the U.S.A. won’t be there to help you anymore, just like you weren’t there for us,” Mr. Trump said. “Iran has been, essentially, decimated. The hard part is done. Go get your own oil!”

Whatever. Actions matter more than these addled words, and the sooner we’re out, the better. I’ll offer more thoughts on the next chapter at the end of this post.

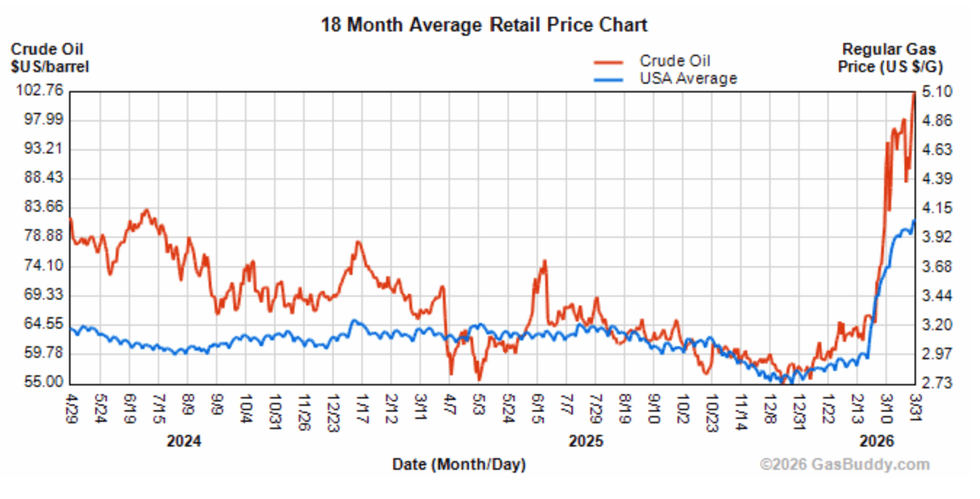

The figure below, from GasBuddy shows the well-known spike in oil and gas. The AAA national average gas price on Wednesday was $4.06, up from <$3 prewar.

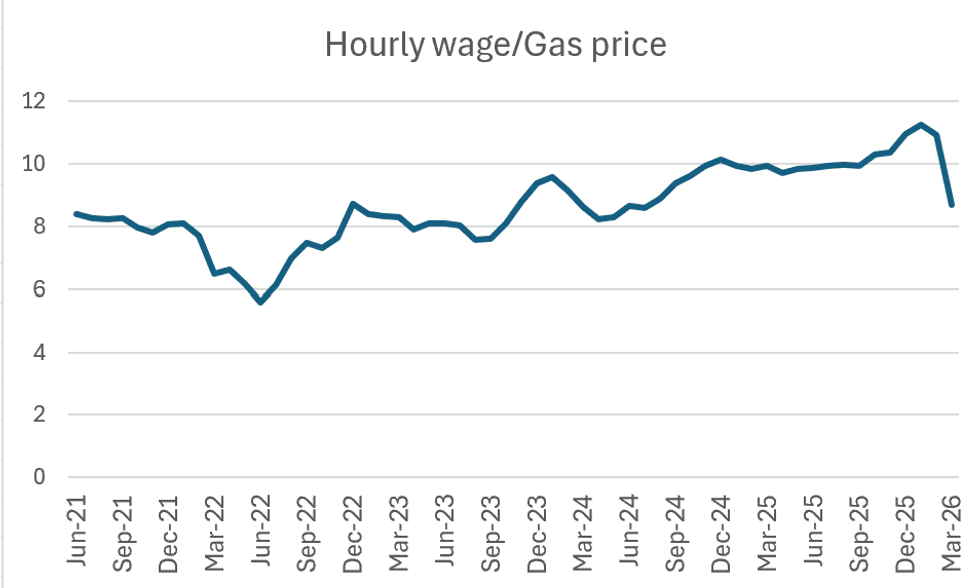

Here’s another way to look at this, one I think is instructive re how folks experience such spikes. It’s the hourly wage for mid- and low-wage workers divided by the price of a gallon of gas (I estimated the March wage so as to capture war gas-price effects—we’ll know the actual wage rate on Friday). It thus shows how many gallons you can buy for an hour of work. It’s back down to around where it was a few years ago, as energy (and food) supplies were recovering from the Ukraine shock.

Negative spikes like that are tough on budgets, though this metric remains in a familiar range. The question then becomes should we expect the decline in after-tax, including this war tax, income to ding consumer spending going forward.

In fact, real consumer spending was already getting a bit weaker, up at a sub-two percent rate on a six-month annualized basis. And this gas tax won’t help. Neither will the fact that the job market continues to soften, as yesterday’s JOLTs data featured yet another dip in the hiring rate.

My forecast has the nominal wage of mid-wage workers growing at 3.6 percent, year over yaear, right now, down from four percent a few months ago. With the gas price spike, headline inflation could come close to the wage rate, meaning less paycheck buying power. The GS Research team is thus marking down their forecast: “Spending headwinds from higher inflation due to the recent energy price surge are likely to weigh on spending growth for the rest of the year, however, and we now forecast below-consensus real PCE spending growth of 1.3 percent in 2026 on a Q4/Q4 basis (vs. 2.1 percent in 2025).”

Same for real incomes, especially among less well-off households (my bold): “…higher headline inflation due to the recent rise in energy prices is set to erode household spending power, particularly among lower-income households that spend a larger share of their budget on energy goods. As a result, we now forecast only 1.7% real income growth in 2026 on a Q4/Q4 basis, with growth of just 0.4 percent among households in the bottom income quintile.”

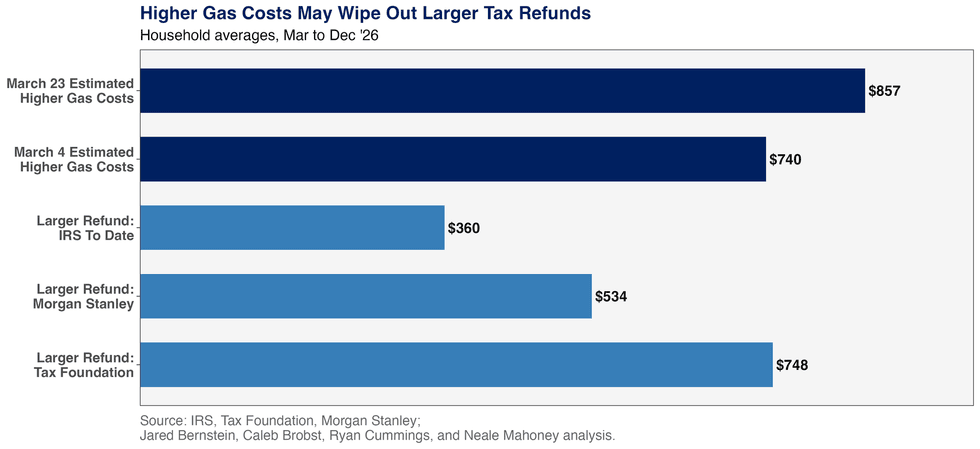

Keep in mind that many of those same families are getting hit with Medicaid and SNAP (food stamp) cuts, so this is a perfect storm for them. Won’t they get higher tax refunds from last year’s budget bill? Nope. Families in the bottom fifth tend not to have federal tax liabilities so refunds won’t help them.

But as my Stanford Institute for Economic Policy Research colleagues and I have shown, for higher income households that do get a higher refund, the gas tax is likely to eat it:

While oil/gas get a lot of attention, spillover costs are equally important.

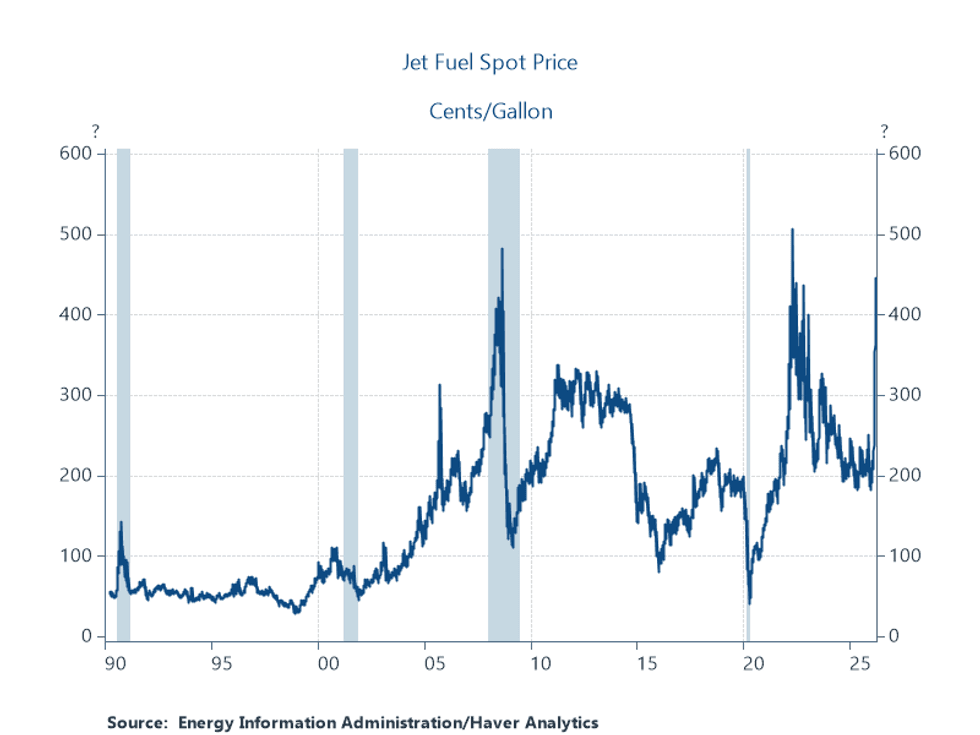

Based on the sharpest jet fuel spike in recent history…

…airfares are climbing and the Wall Street Journal reports forthcoming surcharges, some of which will add over $100 to tickets.

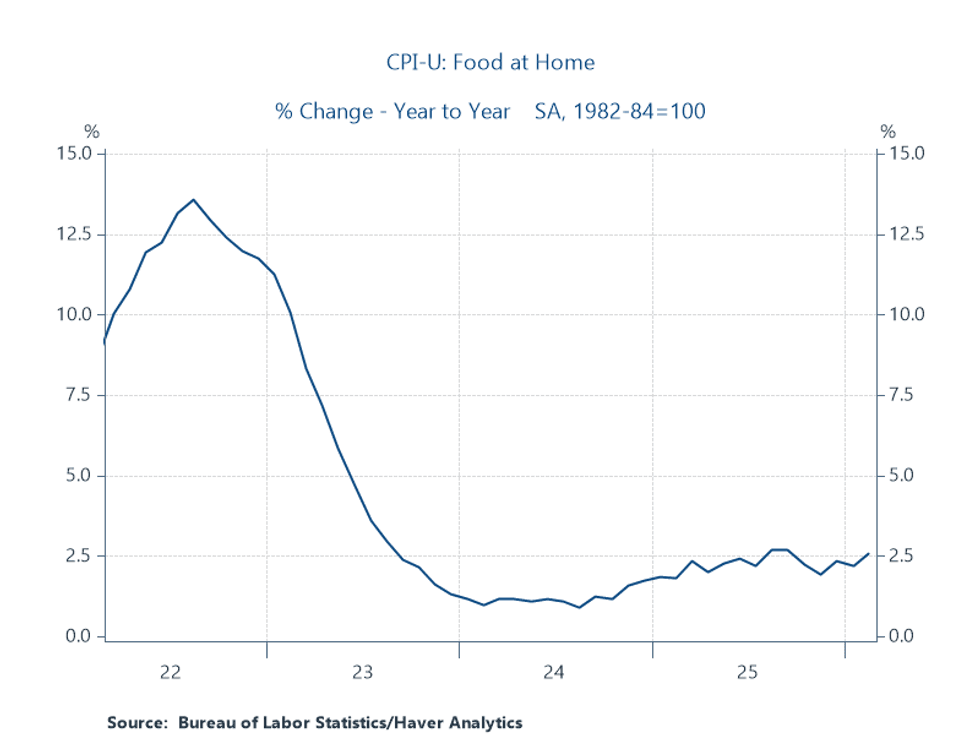

I’ve talked before about food costs spillovers, noting the about a third of fertilizer transits the SoH, along with nat gas that’s used to make it. Our food supply chain is already getting hit, though we’re more insulated than some less developed countries that could experience serious shortages.

The problem for American consumers is that they were already facing higher grocery inflation, partly due to tariffs. Grocery inflation can be seen drifting up, pre-war; 2.5 percent, the most recent print, is historically high for this component. This is a key e.g. of what I mean when I say Trump’s pushing hard in the wrong direction on affordability.

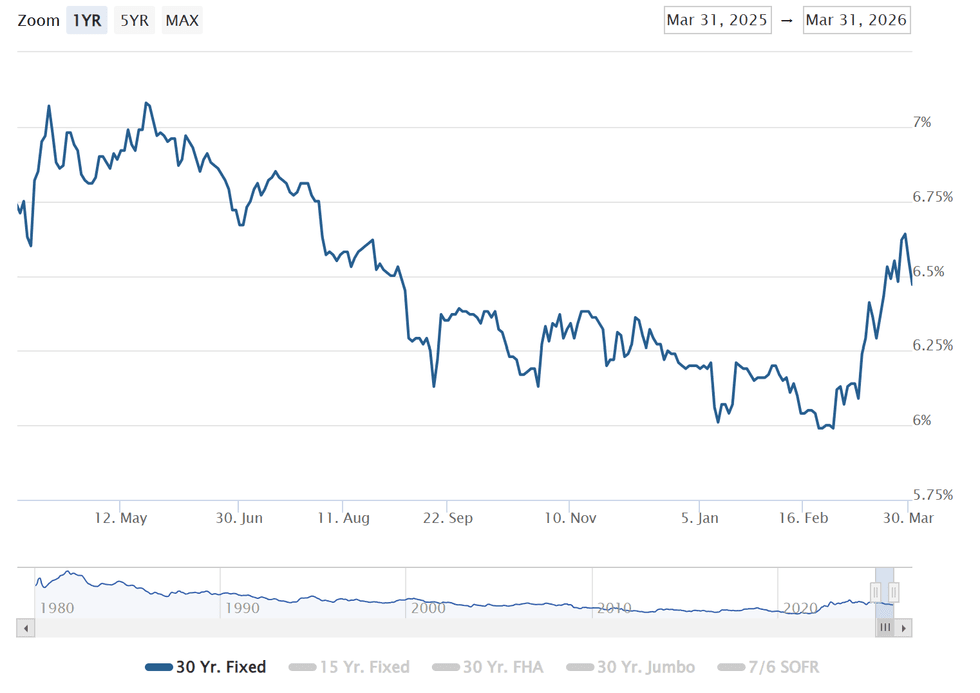

Then there’s interest rates and the Fed. The rate on 30-year mortgages has eased a bit, and will probably ease further if we de-escalate, but that’s a tough spike you see at the end of the figure below, and not just for homebuyers but for the many more who were contemplating refinancing when the rate dipped below six percent prewar.

All of this has led to the Fed being a lot less likely to lower the interest rate they control any time soon. Prewar, markets assigned a 75 percent chance that the interest-rate gang would hold at the current range of 3.5 percent -3.75 percent and a 23 percent chance of a 25 basis-point cut. The current probabilities for the April 29 meeting are 99.5 percent for hold and zero for cut.

That’s a lot to digest but in sum, it’s a helluva a lot of damage over a very short time. The justifiably much-vaunted U.S. macroeconomy has been incredibly resilient to bad policy, but it’s not impenetrable.

What happens next? We’ll see what Trump says tonight but I strongly fear and strongly predict that chaos ensues. After detailing our great victory—11,000 targets hit! (the fact that these people can’t distinguish target-hits from regional strategy is mind-blowing)—I suspect he'll rattle off some mushy, incoherent plans about de-escalation and gradually reducing our presence in the region.

I doubt that changes much in terms of the near-term economics documented herein. Iran knows it holds a very powerful card in shutting down the SoH and could decide to continue to play it, or the regime could ramp up their $2 million/vessel toll fee, which maybe isn’t quite the regime-change outcome we had in mind.

Trumpian policy mush, as with tariffs, is never great. But in this case, it’s especially harmful. There’s just no escaping the fact that he inherited a strong economy and he’s been abusing it even since. The resulting costs are making life considerably less affordable and that’s before you consider the opportunity costs of prosecuting this terrible war, running a violent deportation program, etc…instead of, you know, figuring out how to deliver more affordable housing, healthcare, and child care.

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please consider subscribing to his Substack.

Reprinted with permission from Econjared.

- How Trump Republicans Cut Down The Child Tax Credit And Drove Up Child Poverty - National Memo ›

- Is Trump's Promise To Slash Prices Working Out For You? No? I've Got Receipts - National Memo ›

- Trump's War Delivers A Spike In The Consumer Price Index - National Memo ›

- Following Biden Boom, New Factory Construction Keeps Falling Under Trump - National Memo ›