How Warsh May Infect The Federal Reserve With Trump's Rampant Corruption

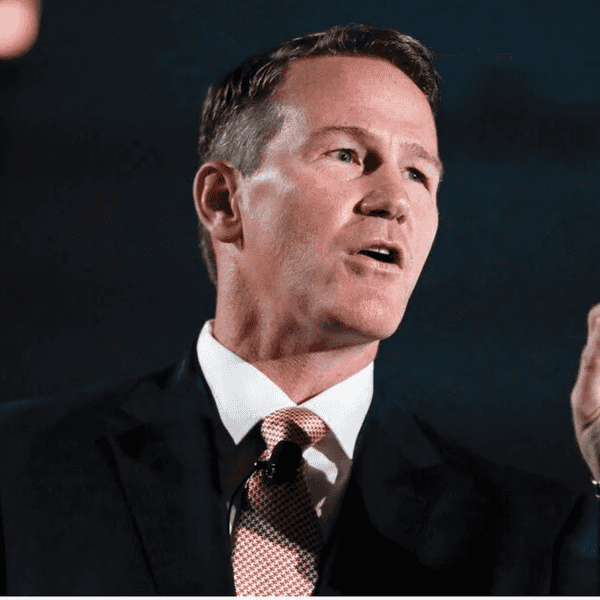

Federal Reserve Chaiir Kevin Warsh at press conference on June 17, 2026 in Washington, D.C.

This week was the first meeting under new Federal Reserve Chair Kevin Warsh of the Federal Reserve Boards Open Market Committee (FOMC). Warsh has promised to restructure the Fed, but it is still not clear he means by this.

Donald Trump very explicitly picked Warsh because he expected that he would lower interest rates. That goes against Warsh’s past history of being an inflation hawk. In his earlier tenure as a Fed governor during the Great Recession, Warsh was arguing against expansionary monetary policy even when the unemployment rate was close to ten percent. And he was concerned about hyperinflation when the actual inflation rate was near zero.

We still don’t know how Warsh plans to resolve these seemingly contradictory impulses. He has said that he wants to reduce the Fed’s balance sheet. This would mean selling off trillions of dollars of bonds that the Fed bought both during the financial crisis and more recently during the pandemic.

Selling off bonds would have the effect of raising the long-term interest rates that matter most for the economy, like car loans and mortgages. But it’s possible that Trump wouldn’t be bothered, since he probably doesn’t understand the connection between reducing the balance sheet and raising rates.

The other area where Warsh has indicated he wants to make a sharp departure from past practice is the amount of information that the Fed discloses to the public about its discussions. This reverses the trend toward greater transparency under the last three Fed chairs.

Under Alan Greenspan, the Fed was deliberately opaque. I remember walking to work one day in the mid-1990s, the day after Greenspan had given some big speech. Back then, we had newspaper boxes where you could buy a newspaper. I always glanced at the machines as I walked by. Half of the papers had headlines saying something to the effect of “Greenspan plans to raise rates.” The headlines for the other half were something to the effect “Greenspan to leave rates unchanged.”

Greenspan, who followed his press closely, was reportedly delighted. He had given a major speech, and no one had any idea what he was talking about.

Ben Bernanke, his immediate successor, wanted the Fed to be more transparent. He explicitly introduced the concept of “forward guidance” to Fed policy: the idea that the Fed would tell people where it expected interest rates to go in the near-term future. In their tenures as Fed chair, both Janet Yellen and Jerome Powell continued this policy. Their view was that they did not want the public to be surprised by the Fed’s decisions.

As an economic matter, this makes good sense. It is desirable to reduce uncertainty so that businesses and individuals can better make plans for the future. If a business is considering borrowing to expand, it may want to put its plans on hold if the Fed says it is likely to raise rates substantially in the near future. By sharing as much information as practical, businesses and individuals can be better informed about the likely future state of the economy and take this information into account in making their decisions.

Transparency is also important for combatting corruption. If anyone has inside knowledge of the Fed’s interest rate plans, they can make a huge amount of money, at the expense of others in the market, through their inside trades.

Wayne Angell, who served as a Fed governor from 1986 to 1994, began consulting at the rate of $100 a minute (roughly $220 in today’s dollars) after he stepped down from his position in 1994. Angell may have been an insightful observer of the national economy, but he was obviously being paid for his knowledge of his former colleagues’ views on interest rates.

If the Fed is fully transparent about its intentions, no one is going to get paid $220 a minute for their insights on what the FOMC is thinking. We don’t know how far Warsh will look to go with this move away from Fed transparency, but the further he goes, the more room there is for corruption.

And that is what makes Warsh a true Trump appointee. No administration in U.S. history has ever been as blatantly corrupt as Trump in his second term. Warsh seems intent on bringing that corruption to the Fed.

Dean Baker is a senior economist at the Center for Economic and Policy Research and the author of the 2016 book Rigged: How Globalization and the Rules of the Modern Economy Were Structured to Make the Rich Richer. Please consider subscribing to his Substack.

- Trump Lawsuits: Of All His Grifts, They Are By Far The Most Efficient ›

- UBS Libor Manipulation Merits A Death Penalty ›

- Fun Times Ahead! What Kevin Warsh Can Expect At His First Fed Meeting ›

- In The Fed Case, Justices Confront The Problem Of The Lying President ›

- 'Venezuelifying' America: Don't Cross The Dictator Or He Will Destroy You ›

- Nine Americans Who Actually Deserve Money From That Trump Slush Fund ›

- RIP Alan Greenspan: Why New Fed Chair Warsh Shouldn't Imitate His Cryptic Style - National Memo ›

- Will Surrendering To Iran Relieve Trump's Gas Pains? Alas, Probably Not! - National Memo ›

- Here’s how to fix the Fed’s ‘culture of corruption’ - The Boston Globe ›

- Elizabeth Warren, Rick Scott Warn of “Culture of Corruption” at the Fed, Call for Stronger Ethics Enforcement | United States Committee on Banking, Housing, and Urban Affairs ›

- In Bipartisan Letter, Warren, Scott Call New Federal Reserve Ethics Enforcement Policy “A Dismal Failure” | U.S. Senator Elizabeth Warren of Massachusetts ›

- In Speech, Warren Calls Out Culture of Corruption Among High-Ranking Federal Reserve Officials; Says Responsibility is with Powell | U.S. Senator Elizabeth Warren of Massachusetts ›