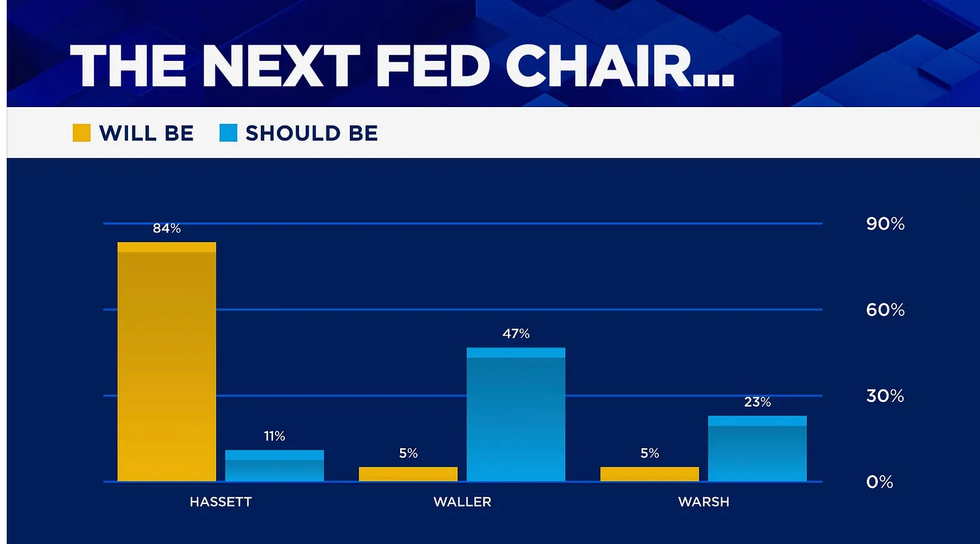

Housing Finance Chief Pulte Instigated Subpoena Threat Against Powell

Multiple news reports show that Federal Housing Finance Agency Director Bill Pulte, who has long participated in Fox News' and President Donald Trump’s pressure campaign to encourage Federal Reserve Chair Jerome Powell to cut interest rates, played a prominent role in the Trump administration’s decision to send subpoenas to the Fed and threaten Powell with criminal indictment on Friday.

Powell has called the investigation a “pretext” and said the real reason for the subpoenas and threats is his clashes with the president on interest rates.

Pulte began pressuring Powell via social media to lower interest rates beginning last May and repeatedly called for him to resign. Pulte also claimed that Powell had lied in his Senate testimony when questioned about the costs associated with renovating the Federal Reserve Board Building in Washington, D.C., and called for a congressional investigation into Powell. Last summer, Pulte even reportedly drafted a letter for Trump to fire Powell.

Pulte also urged the Justice Department to investigate other targets of Trump’s ire, including Fed board member Lisa Cook, who was perceived to be an opponent of Trump’s interest rate agenda, as well as Sen. Adam Schiff (D-CA) and New York Attorney General Letitia James, who had both investigated Trump. Fox News was a major platformer of Pulte’s attacks against Trump’s targets. After Pulte’s attacks against Cook apparently crumbled, he disappeared from Fox for several weeks.

On Sunday, Bloomberg News reported that Pulte “was a driving force” behind Friday’s subpoenas targeting Powell. From Bloomberg’s report:

Federal Housing Finance Agency Director Bill Pulte was a driving force behind the Trump administration’s decision to subpoena the Federal Reserve, according to people familiar with the matter, intensifying pressure on the central bank as President Donald Trump prepares to pick a new Fed chief.

…

The head of the typically staid FHFA has been a vocal force within the administration, pushing controversial housing policy ideas and investigating Trump’s foes for mortgage fraud. Pulte submitted a criminal referral to the DOJ about Fed Governor Lisa Cook that is at the root of Trump’s push to fire her. The Supreme Court is set to take up the Cook case later this month.

The next day, Politico reported that backlash to the threat to indict Powell has ironically led to some Trump administration “officials and allies again calling for the ouster of” Pulte, whom they “suspect” is “behind the latest inquiry.” Politico additionally reported:

Pulte, who spent months last year lambasting Powell on social media and on television, recently pitched Trump on ousting Powell, going so far as to bring “wanted” posters of the Fed chief along with him, according to three of the people familiar.

Indeed, Axios also reported that the day the subpoenas were served to the Federal Reserve, Pulte said to reporters outside of the White House: “We do need to get rid of Jay Powell. He's a disaster.” Pulte reportedly added: “What he's caused with the building is a disgrace to the Fed. The Fed has no credibility as a result of him.”

On January 13, The Wall Street Journal reported: “In recent weeks, one administration official who lobbied for a probe was Bill Pulte. … Pulte had previously argued in favor of opening an investigation into Powell in private conversations with the president and senior administration officials.”

An editorial from the Journal noted that “our sources say Bill Pulte of the Federal Housing Finance Agency wrote a report that made its way to Jeanine Pirro, the U.S. Attorney for Washington, D.C.,” whose office sent the subpoena.

The editorial also called for “firing Mr. Pulte before he can cause any more embarrassment” to the administration.

Amid all the reporting of Pulte’s key involvement in the subpoena against Powell, he turned to Fox Business anchor Maria Bartiromo for her softball treatment in an apparent effort to control the damage. Even though Bartiromo had expressed her own reservations about the threatened indictment against Powell earlier, she pressed Pulte on this news for less than one minute, during which he denied involvement, and let him ramble about other topics for the remainder of the interview.

Reprinted with permission from Media Matters

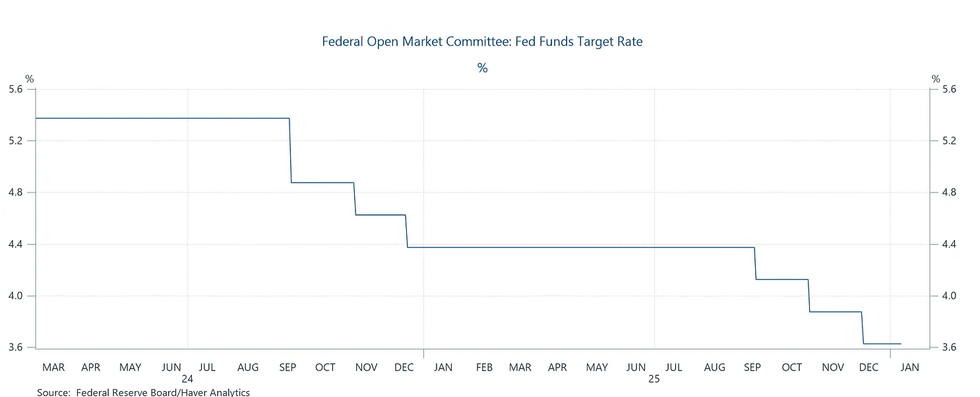

Source: Federal Reserve Board/Haver Analytics

Source: Federal Reserve Board/Haver Analytics

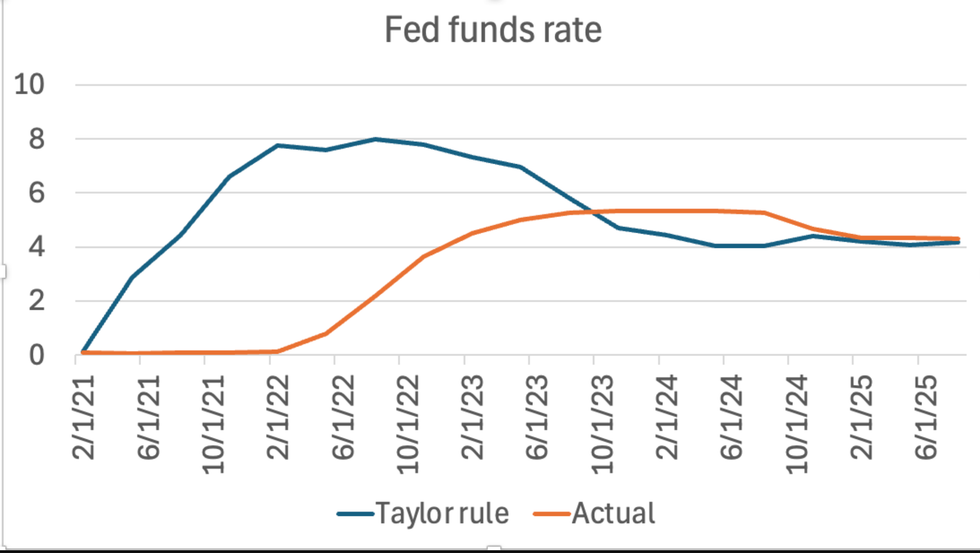

Source: Version FOMCTaylor93UR

Source: Version FOMCTaylor93UR Sources: Board of Governors of the Federal Reserve System, New York Federal Reserve, St. Louis Federal Reserve

Sources: Board of Governors of the Federal Reserve System, New York Federal Reserve, St. Louis Federal Reserve