With System's Looming Implosion, Health Care Could Dominate 2026 Elections

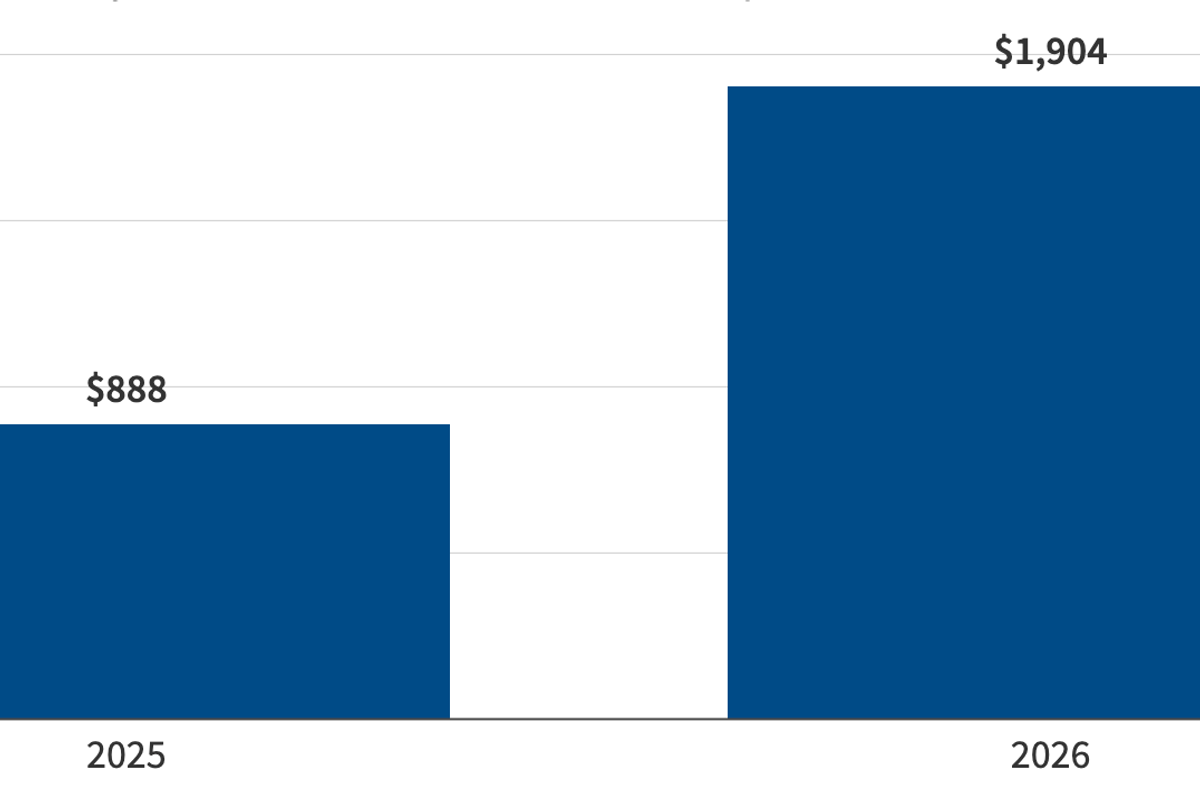

Under GOP budget, ACA monthly insurance premiums are expected to more than double next year

The GOP Congress’ failure to extend the premium subsidies for ACA plans is just the tip of the iceberg set to rip a massive hole in the nation’s private health insurance market in 2026.

As I’ve reported several times in the past several weeks, private insurance premiums for employer-based plans, which cover 165 million working age adults and their families (half the population), are expected to rise nine percent on average next year — the most since passage of the Affordable Care Act. According to the well-respected Mercer survey, employers plan to reduce that increase to six percent by increasing the co-pays and deductibles in their plans.

In other words, employers plan to shift more of the overall health care cost burden onto employees and their families.

Over the past several decades, employers on average picked up about three-fourths of the the total premiums on their plans. Individual employees picked up the other 25 percent. If that ratio remains the same, employees will see the amount of money taken out of their checks each pay period rise by at least six percent, which is more than twice the inflation rate. And that’s before the increase in their higher deductibles and co-pays.

The high cost of high deductibles

How will workers cope with these increases? More will opt into the high-deductible plan option offered by their employers, which usually come with cheaper co-premiums. About half already take that option.

The young and healthy are more likely to choose that path. They are more concerned about upfront co-premium costs than deductibles or co-pays for health care bills that they are less likely to face over the coming 12 months.

This ongoing movement into high-deductible plans has shifted an increasing share of the overall health care cost burden onto the chronically ill, who are less likely to choose high deductible plans. They are the ones who routinely use health care because of heart disease or arthritis or their ongoing battles with cancer or diabetes. They invariably wind up paying every dime of their deductible, whether it’s high or low.

This ongoing shift into high-deductible plans also affects co-premiums on comprehensive coverage. Since it is the sickest people choose the plans with lower out-of-pocket costs, the rates for those plans usually go up even faster than the average as more and more younger, healthier workers opt into high deductible plans.

This is exactly what Republicans are proposing for the individual and family policies being sold on the exchanges. The GOP plan calls for replacing premium subsidies (which lower costs for everyone based on income) with small health savings accounts (HSAs), whose size will be far below the out-of-pocket deductibles in the lowest cost (bronze) plans on the exchanges.

According to news accounts, the Republicans propose giving everyone purchasing individual or family plans on the exchanges a $1,000 HSA ($1,500 if you’re 50 and over). The typical bronze and silver plans have deductibles of $7,500 and $5,000, respectively, according to the Commonwealth Fund.

If you are young and healthy, that’s an attractive option. What’s not to like about the government putting a grand into a personalized HSA when you don’t worry about getting sick? That will leave the silver and gold plans with the sickest people, and send their premiums soaring. This dynamic is why the unsubsidized individual market with accompanying high-risk pools (established by some states) failed prior to passage of the Affordable Care Act.

A little over a year ago, Donald Trump rode a wave of popular anger about rising prices into the White House. In 2024, the average cost of an employer-based plan rose just four percent, new data from the University of Minnesota’s State Health Access Data Assistance Center shows. That was less than half of what is expected during 2026, Trump’s second year in office.

What’s behind those higher costs?

Venal politicians and employer greed aren’t the root cause of rapidly rising health care costs. Their tactics reflect how powerful people, whether in Washington or the C-suite, ensure their favored constituents (the rich and stockholders, respectively) bear as little of the burden as possible.

For most health care economists, the standard explanation for rising costs sounds like a description of the various peaks of a distant mountain range in a landscape painting. They include:

- Rapidly rising drug prices and utilization, especially for pricey weight-loss drugs;

- Incessant price increases demanded by hospitals and physician practices, which they blame on labor shortages made worse by the immigration crackdown; higher prices for medical supplies and equipment, some of which is tariff-induced; and higher wages for their employees, who themselves are being hit with higher prices for everything they buy;

- The rising prevalence of chronic conditions diabetes, cardiovascular disease and obesity;

- Demographics (an aging population); and

- Consolidation and monopolization of hospital and insurance markets.

But once you climb onto any one of those mountain peaks and look around, you find that every sector of health care operates like a special interest whose incessant pursuit of higher revenue drives up costs. No one takes responsibility for creating a more efficient, more effective and less costly system.

- The drug industry abuses patent monopolies on new therapeutics to delay entry of generics and biosimilars. It charges insanely high prices for new drugs that are barely more effective than previous therapies that are now generic. Its legitimate breakthroughs, like the new gene therapies or targeted cancer drugs that were largely invented in government-funded labs, have prices that threaten to bankrupt the entire system.

- Hospitals operate inefficiently. They refuse to rein in overuse of pricey procedures. They are larded with administrative waste and overpay senior executives.

- The lowest paid physicians in the U.S. are paid more than their European or Japanese colleagues, while high-paid specialists like orthopedic and cardiovascular surgeons earn three times what primary care physicians — the ones who can prevent people from needing joint replacements and heart operations — earn. Their specialty societies and lobbyists prevent increasing the scope of practice for physician assistants and nurses.

- Insurance companies, including pharmacy benefit managers, have largely failed to add value for their 15% add-ons to underlying costs. Insurers largely ignore care coordination and fail to prevent overuse of unnecessary care other than through imposing onerous prior authorization processes that alienate physicians and angers patients. They burdens the entire system with excessive administrative costs.

The Trump administration and the GOP Congress have offered next to nothing to address any of these issues. Drug price negotiations — the one arena where it has taken some steps — simply carries out the legislation that was passed during the Biden administration.

Last week, I offered a bold plan to reform payment policy in the U.S. It was designed to cut through the Gordian knot of those special interests by adopting a single-pricing system tied to global budgets, while at the same time providing instant relief to families suffering the ill-effects of excessive health care costs. It would establish a firm cap of eight percent of income on what households can spend on health care in any given year.

Given the harsh reality that millions of U.S. households are facing when it comes to inflation in general and health care costs in particular, I am mildly optimistic that we will see some people running for office next year including some or all of that plan’s components in their campaign pledges.

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News

- Democrats Must Address Looming Cost Spike In Private Health Insurance ›

- A Decent Slice: The Affordability Crisis Isn't Only About Prices ›

- As Insurance Costs Surge, GOP No Longer Pretends To Support Universal Coverage ›

- 'The Ideas Are There': Shutdown End Signals Renewed GOP Assault On Health Care ›

- Republicans Push Skimpy, Unaffordable Health Coverage As Costs Keep Rising ›

- Gallup Poll: Public Satisfaction With Health Care Costs Hits New Low - National Memo ›

- Dumping Casey Means, Trump Nominates A Fox Covid-19 Misinformer As Surgeon General - National Memo ›

- Fresh Warnings In The Government's First-Quarter Economic Report - National Memo ›

- Why Democrats Must Bring A Fresh VisionTo Debate Over Health Care - National Memo ›