Kevin Warsh had his confirmation hearing yesterday to chair the Federal Reserve once current chair Jerome Powell’s term ends in mid-May. I’ve got a few choice words for these confirmation hearings in general, as they’ve become a big waste of time and should either be scrapped or somehow reformed. They’ve devolved into a signaling exercise that has almost nothing to do with the substance of the nominee’s work. And I speak from experience, as I had to go through a Senate confirmation (wherein I prevailed by 50-49 baby, i.e., with room to spare!).

In that light, I couldn’t watch much of this one. Too painful. But I closely followed it and can report on what I think we might be getting, once the Tillis hold is resolved (you can read about that here) and Warsh takes the chair (once he’s out of committee, he’ll get a majority in the Senate).

Between his opening statement and back-and-forth with the senators on the Banking Committee, I listened carefully to try to discern two things. First, and most important, Warsh’s independence from Trump, and second, what sort of monetary policy he might favor. In both cases, the signals were highly jammed by the posturing and shape-shifting that has made these confirmations largely futile exercises.

For one, Warsh really wants this job—he’s not alone in that—and he knows Trump is listening to him. He therefore has three choices: speak truth to power, Trump’s wrath be damned; mush it up so no one knows what he’s saying; just tell Trump what he wants to hear.

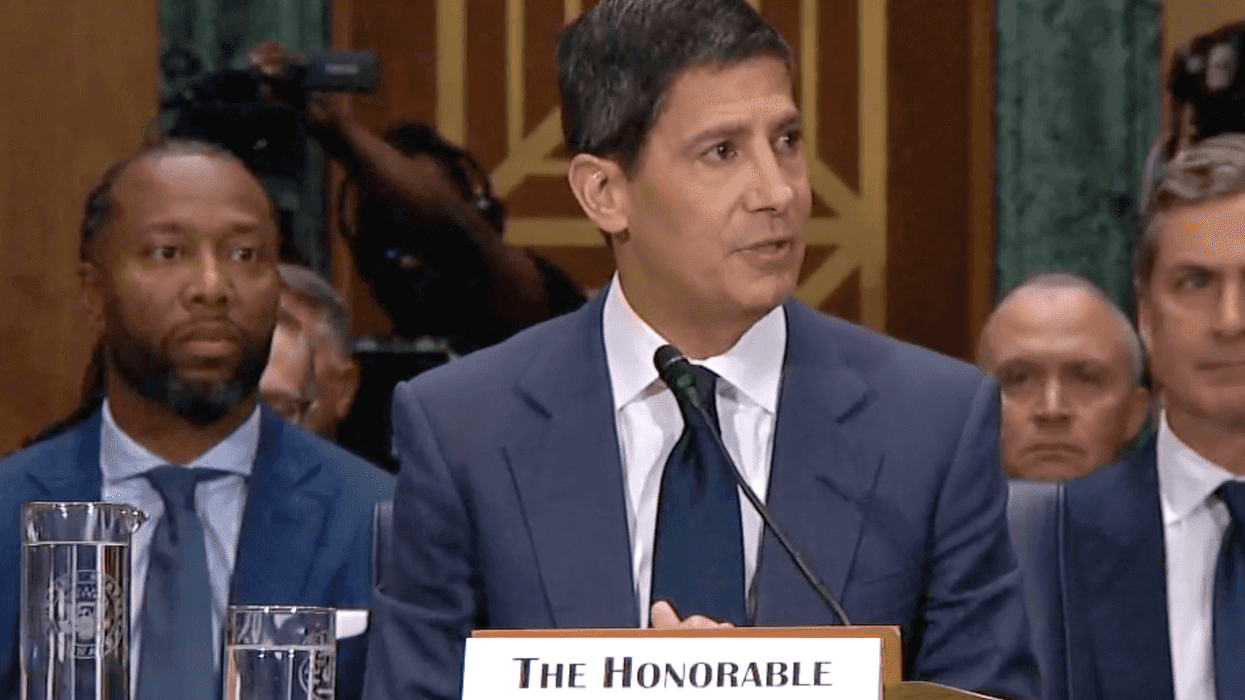

He largely chose the third path. This was no profile in courage. He wouldn’t say that Trump lost the 2020 election. He would not support either Lisa Cook or Powell against Trump’s attacks. More tellingly and substantively, Sen. Chris Van Hollen (D-MD) challenged Warsh on the case for Fed rate cuts, given the fact that inflation has been above the Fed’s target for five years, and that was before war-induced price pressures. His line of questioning asked if a Federal funds rate of one percent would be too low right now, which should be an easy softball as even Trump’s appointee Fed Gov. Stephen Miran is not suggesting such an aggressive cut. But Warsh refused to admit that given current inflationary pressures, one percent would be too low a rate.

This is all concerning in terms of independence from Trump, and in normal circumstances would disqualify him. But anyone in that seat is in a vise, and it doesn’t make sense for them to accept the nomination and antagonize Trump. By showing up, Warsh is basically saying “I’m going to say pleasing things to Trump in order to get the job. They may or may not be true.” In fact, I think they’re mostly not true—my call from a while back that he’s a monetary hawk imitating a dove is looking good after this hearing, but we’ll get to that.

Bottom line, based on this performance, we must be nervous about Fed independence under Warsh, as would be the case with any Trump nominee. He’s shown himself to be a politically motivated shape-shifter, which makes it hard to know how he’d actually handle the independence question. It’s analogous to those Supreme Court justice confirmations wherein they invariably say, “don’t worry—I’m just there to call balls and strikes” and then, in many cases, implement a strike zone that’s more ideological than balanced.

Turning to how he’d govern, even as he sold himself as a rate-cutting dove, I saw numerous signs to the contrary. Before I get to them however, read this Atlantic take from Roge Karma back in January. Here’s how I weighed in:

…Warsh is seen as an inflation hawk who will err on the side of higher, not lower, interest rates. During the 2010s, he became known within Wall Street and Washington circles as one of the fiercest critics of the Fed’s zero-interest-rate policy, to the point of warning about inflation when unemployment was still at 10 percent. “He’s a pretty stone-cold hard-money guy,” Jared Bernstein, who served as the chair of Joe Biden’s Council of Economic Advisers, told me. “It’s a peculiar choice for Trump, because the Fed that Warsh wants is very different from the one Trump wants.”

If you listen carefully to both what Warsh said and, more tellingly, didn’t say, you can see what I mean. His opening statement mentions the full employment side of the Fed’s mandate once in passing, focusing far more intensely on the inflation side:

…Congress tasked the Fed with the mission to ensure price stability, without excuse or equivocation, argument or anguish. Inflation is a choice, and the Fed must take responsibility for it. Low inflation is the Fed’s plot armor, its vital protection again slings and arrows. So, when inflation surges—as it has done in recent years—grievous harm is done to our citizens, especially to the least well-off. They lose purchasing power. Their standard of living falls. They may also lose faith in our system of economic governance, raising doubts whether monetary policy independence is all it’s cracked up to be.

Such passion! Such concern for the poor! And he’s not wrong about the damage from high inflation (though the “inflation is a choice” part is off—exogenous supply shocks happen). But, replace the word “inflation” with “unemployment” and “purchasing power” with income. You can and should listen for yourself—here’s the full video—but I saw and heard a hawk in dove’s clothing.

If so, his internal weighting of the two sides of the mandate would be different from that of Powell, Yellen, Bernanke, who all seemed pretty balanced to me, though of course, pre-pandemic, inflation tended to run below target so the low correlation between unemployment and inflation (flat Phillips Curve) gave them more leeway to pursue lower unemployment.

Two caveats re this hawkish contention of mine. First, there is an equally defensible view that Warsh is a dove when Republicans are in power and a hawk when there’s a Democrat in the White House. Back to Karma’s article:

The case against Warsh is this: What he wants seems to change depending on which party controls the White House. Warsh was a staunch inflation hawk during the Obama administration. Then Trump was elected, and he seemed to soften. In a 2018 Wall Street Journal op-ed titled “Fed Tightening? Not Now,” Warsh and his co-author, Stanley Druckenmiller, argued that, “given recent economic and market developments, the Fed should cease—for now—its double-barreled blitz of higher interest rates and tighter liquidity.”

“He’s someone who has repeatedly shown a willingness to change his positions on a dime when it’s politically convenient,” Skanda Amarnath, the executive director of Employ America, a Fed-focused think tank, told me.

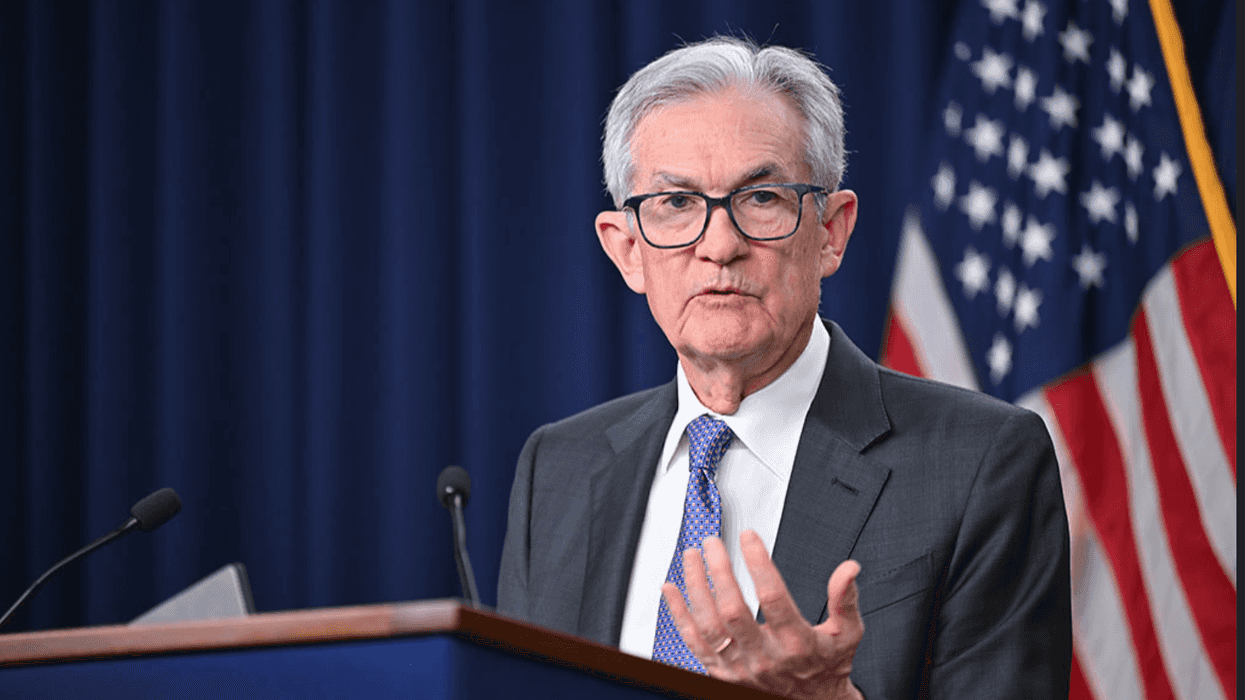

Caveat two is that whatever his true views are, he’s very likely to come out of the box sending rate cut signals to the White House. Yes, that’s the antithesis of Fed independence and the polar opposite of what we’ve seen from Powell, someone who consistently speaks truth to power with clarity and strength. But my point here is that it will take some time to see where Warsh really stands.

There was another part of his testimony that I found highly concerning. He made a weird and troubling distinction between monetary policy, which he correctly argued should be independent from politics, and the Fed’s regulatory oversight role in banking and financial markets, which he incorrectly argued should be open to political pressures. This is a terrible idea, one that raises the risk of the White House pushing to let markets rip—what president doesn’t want a booming stock market?—and thereby underpricing the systemic risk that excessive financial deregulation never fails to deliver.

In a similar vein, Warsh, who made his $100+ million in markets, was also far too sympathetic to the idea of integrating cryptocurrencies into the banking system, a view that placates the powerful crypto lobby at the expense of ordinary Americans and the stability of the broader economy, given the riskiness and volatility of this asset class.

There were other ideas both bad—something about having the Fed work with the statistical agencies to derive a new inflation measure; that raises all sorts of potential conflicts, especially with Trump looming in the wings— or irrelevant—focusing on median or trimmed inflation measures, which of course the Fed staff already does—or good—dialing back excessive Fed communications, press conferences when there’s nothing much to say, and “dot plots” that get over-interpreted by obsessive Fed watchers.

All his stuff about how AI was going to raise the economy’s potential growth rate and thereby allow for lower rates was also misguided (and again, given my framework argued above, was just a tactic designed to please Trump and give his dovishness a penumbra of substance). First, all the capital equipment expenditures associated with AI investment will put upward pressure on rates (to be fair, I think he may have conceded that point) but more importantly, when it comes to productivity gains, you have to see them to believe them, and it takes at least five years to see them.

All told, as you see, I’m nervous about this guy as Fed chair, but he’s better than some of the alternatives, and I’m definitely going to give him a chance. I believe he’s capable of rising to the occasion and filling the shoes of some of the great chairs who came before him, but I’ll be watching closely. Most of what I heard yesterday was not inspiring in that regard.

Which brings me to my final point. These confirmation hearings are awful. They reveal nothing about the nominee except how good he or she is in bending themselves into a pretzel to avoid saying anything of substance (to be fair, there are exceptions; the Van Hollen example above was a smart, substantive question that Warsh flubbed). The members spend their time mostly signaling to their constituents that they’re either harassing or supporting the president’s picks, and then the votes proceed along partisan lines. There’s got to be a better way.

It would be better to have a hearing wherein D and R witnesses, excluding the nominee, discuss the nominees work and his/her positions. At least that way, the public could learn more about what the nominee really believes.

Anyway, much more to come on this, though only if Trump can get out of his own way and let Warsh move ahead.

Jared Bernstein is a former chair of the White House Council of Economic Advisers under President Joe Biden. He is a senior fellow at the Council on Budget and Policy Priorities. Please consider subscribing to his Substack.