Trump And His Senate Enablers Push Economy Over A Cliff

I'll explain that troubling nexus, but first, let's understand the awful reality that Trump and Radical Republicans in the Senate have created and why it can only make our economic disaster worse.

Because of Trump's mismanagement, America has been in economic freefall since March as the Grim Reaper roams freely.

Thanks to Trump's denial of science and idiotic ideas about the coronavirus, the pandemic grows worse and worse even as Europeans and others are tamping down the pathogen.

Because of Trump's mismanagement, America has been in economic freefall since March as the Grim Reaper roams freely.

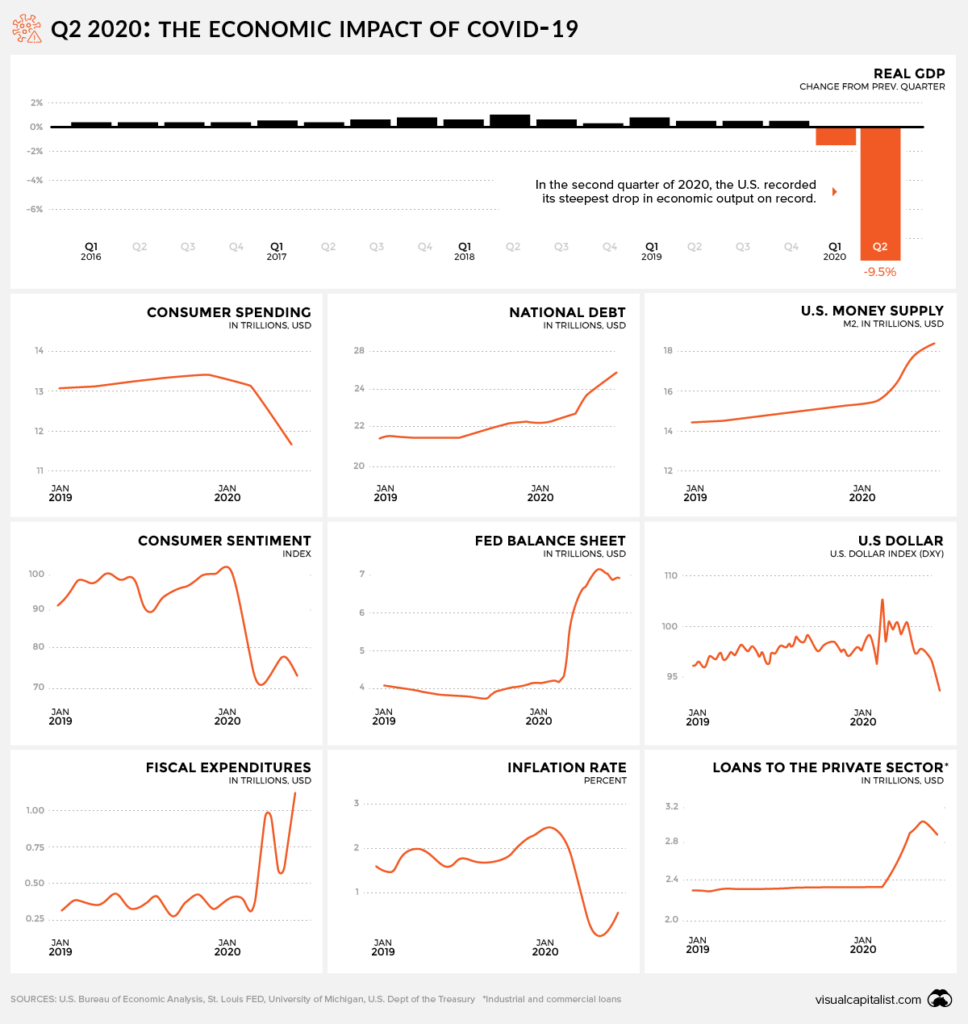

In the second quarter, from April 1 to June 30, the economy shrank at a rate never before seen, not even during the Great Depression or the horrible economic panics of the late 19th Century.

The economic impact of COVID-19 in the U.S.

"Real gross domestic product (GDP) decreased at an annual rate of 32.9 percent in the second quarter of 2020," the Commerce Department announced Thursday.

During the Great Depression, the economy decreased by 36 percent. But that was after more than three years while the Commerce Department announcement was about a one-year rate.

If our economy continues contracting at its current rate in three years, we'll have the economy when Jimmy Carter took office in 1977. That would be a 60 percent smaller economic pie to be split among 50 percent more people. For most people, the slices would be very thin, too thin for a decent life.

Trump and his Radical Republican allies are accelerating our economic collapse by cutting off, effective today, the $600 of weekly relief payments going to 17 million people without jobs.

Collectively those out-of-work Americans will lose $10 billion of income next week and another $10 billion the week after that and on and on.

This will force overall spending in America to drop by about 2.5 cents on the dollar, a severe new constraint on the economy.

This cut off of relief money is not just a disaster for those without work. It means that grocery stores, hardware stores, utilities, and landlords will collect $10 billion less per week. In turn that will force more layoffs and will push some small businesses into bankruptcy, not to mention the adults and children who will go hungry.

Adding to this Trumpian misery, the CARES Act moratorium on evictions ended last week. That means landlords can throw families into the street starting Aug. 24. Where landlords will find new paying tenants is a mystery. What we know for certain is that mass evictions will overwhelm local governments, social services agencies and charities.

Next, on Oct. 1, the airlines will be free to start layoffs. Congress gave $58 billion in coronavirus relief to the airlines on the promise that they keep people employed through the end of September. Even with that, Delta says it persuaded 17,000 workers to retire or take buyouts.

More than 60,000 workers are expected to lose their jobs at just two airlines, American and United, come October. In all more than 100,000 airline workers are likely to get the boot just before the Nov. 3 presidential election. That, in turn, will mean even less spending and thus pressure on more small businesses to fold, causing those fired small business workers to need relief.

And, atop this, Trump wants to get rid of the United States Post Office, throwing its 496,000 staffers into the unemployment lines.

And why is this happening? What's behind this economic injustice of throwing the economy off a cliff during the deadliest public health crisis in a century? The answer lies in the Washington cult of corporatism and its mantra of freedom from accountability.

Mitch McConnell believes that the civil courts simply are not just. The senate majority leader fears that workers who are hired back and then contract COVID-19 will sue their employers and then collect huge jury awards.

So, McConnell says, there will be no jobless relief or help for small business until Congress grants corporations absolute immunity from coronavirus litigation. Never mind that there is no evidence to support his fear, that the courts have made lawsuits much harder to file, especially class action lawsuits, and that McConnell has packed the federal bench with Trumpians.

On one level this is part of the long-term trend in America of giving corporations more and more power while simultaneously requiring less and less accountability.

Trump has slashed all manner of environmental and other regulations, pretty much stopped enforcing job safety laws and made it much more difficult to file complaints with regulatory agencies, which even when a complaint is successfully made do next to nothing.

Giving corporations a pass on coronavirus litigation would encourage the worst business practices. Many companies act responsibly. Regulations exist to protect us from the worst operators. Awful employers would benefit from McConnell's position, which is the soulless idea that being American means you enjoy the right to behave badly, especially if you are rich enough to own a business.

In the immoral world McConnell favors, and Trump has lived in since birth, businesses are not privileged creatures of the state allowed to exist so long as they operate thoughtfully. No, to these two men and their confreres, controlling an American corporation means being free to act dangerously while the state protects you from accountability for your bad deeds.

Why spend money on personal protection equipment for workers during a pandemic? Why slow the production line for disinfecting? Why widen distances between workers when you can just pack them close enough so they breathe one another's droplets? And when those droplets are laced with coronavirus, causing workers to get sick and die, why should widows and orphans be able to sue?

This is the perverse place where Trump, McConnell and Senate Republicans meet Black Lives Matter.

The Black Lives Matter movement doesn't trust the justice system, either. But its concern runs in the opposite direction. The Black Lives Matter people want to remove the institutional, legal and cultural shields that protect violent police officers. They don't trust the system to hold police accountable and provide recompense to innocent victims like Breonna Taylor, shot to death by Louisville police who broke into her home March 13 with a no-knock warrant.

Even if the House Democrats wilt and give McConnell the corporate favor he wants, the Kentucky senator says he won't allow the $600 weekly relief payments. He wants the benefit cut by at least two thirds to $200 per week.

The tragedy of the Trump and McConnell position is that this goes far beyond their shared contempt for the 51 million Americans—roughly one of every three workers—who have filed for unemployment benefits in the last 17 weeks.

Trump and McConnell are so eager to concentrate economic power even more than today that they will make millions suffer. And it's not just the jobless today, but those who will be laid off as the lack of relief payments forces more business to tighten up, shut down and even file for liquidation in federal bankruptcy court.

One last, and troubling, note…

Even if McConnell folds soon and agrees to resume relief payments, the money will not flow smoothly or swiftly. Only 14 of the 50 states have modernized their systems for paying jobless benefits.

In California it will take as many as 20 weeks to restart payments and add new people to the relief roster, Sharon Hilliard, who heads California's Employment Development Department, told a legislative committee Thursday.

That means some of the unfortunate who have or will lose their jobs due to the coronavirus can expect their next federal relief the week before Christmas, assuming they still have an address and we still have a Post Office.