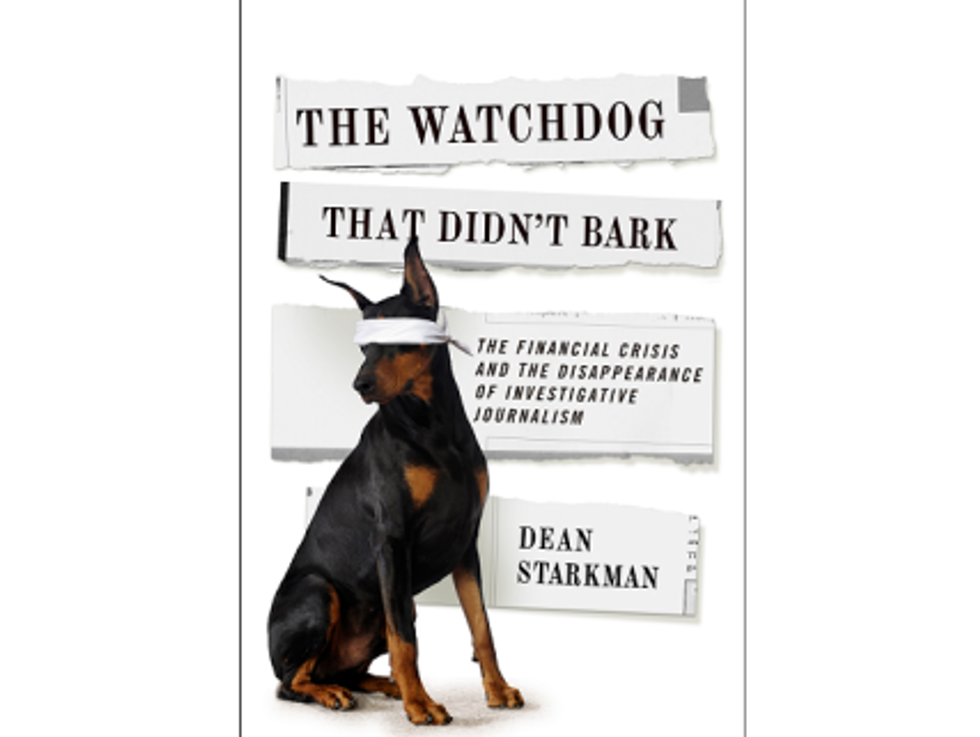

Today the Weekend Reader brings you The Watchdog that Didn’t Bark: The Financial Crisis and the Disappearance of Investigative Journalism by Dean Starkman, editor of the Columbia Journalism Review and fellow at The Investigative Fund at The Nation Institute. Starkman argues that the institutionalization of muckraking from the 1960s and the investigative culture of journalism have worn off. This has led to silence and unreported stories of corruption, as made evident in the years that preceded the 2008 financial crisis.

You can purchase the book here.

The U.S. business press failed to investigate and hold accountable Wall Street banks and major mortgage lenders in the years leading up to the financial crisis of 2008. That’s why the crisis came as such a shock to the public and to the press itself.

And that’s the news about the news.

The watchdog didn’t bark. What happened? How could an entire journalism subculture, understood to be sophisticated and plugged in, miss the central story occurring on its beat? And why was it that some journalists, mostly outside the mainstream, were able to produce work that in fact did reflect the radical changes overtaking the financials system while the vast majority in the mainstream did not?

This book is about journalism watchdogs and what happens when they don’t bark. What happens is the public is left in the dark about and powerless against complex problems that overtake important national institutions. In this case, the complex problem was the corruption of the U.S. financial system. The book is intended for the lay reader—not journalists, not finance aficionados—but those whom the historian Richard Hofstadter called the “literate citizen[s].” That would be anyone who wonders why an entirely manmade event like the financial crisis could take the whole world by surprise.

Few need reminders, even today, of the costs of the crisis: 10 million Americans uprooted by foreclosure with even more still threatened, 23 million unemployed or underemployed, whole communities set back a generation, shocking bailouts for the perpetrators, political polarization here and instability abroad. And so on and so forth.

![]()

Was the brewing crisis really such a secret? Was it all so complex as to be beyond the capacity of conventional journalism and, through it, the public to understand? Was it all so hidden? In fact, the answer to all those questions is “no.” The problem—distorted incentives corrupting the financial industry—was plain, but not to Wall Street executives, traders, rating agencies, analysts, quants, or other financial insiders. It was plain to the outsiders: state regulators, plaintiffs’ lawyers, community groups, defrauded mortgage borrowers, and, mostly, to former employees of financial institutions, the whistleblowers, who were, in fact, blowing the whistle. A few reporters actually talked to them, understood the metastasizing problem, and wrote about it. You’ll meet a couple of them in this book. Unfortunately, they didn’t work for the mainstream business press.

In the aftermath of the Lehman bankruptcy of September 2008, a great fight broke out over the causes of the crisis—a fight that’s more or less resolved at this point. While of course it’s complicated, Wall Street and the mortgage lenders stand front and center in the dock. Meanwhile, a smaller fight broke out over the business press’s role. After all, its central beat—the one over which it claims particular mastery—is the same one that suddenly melted down, to the shock of one and all. For business reporters, the crisis was more than a surprise. There was even something uncanny about it. A generation of professionals had, in effect, grown up with this set of Wall Street firms and had put them on the covers of Fortune and Forbes, the front page of the Wall Street Journal and the New York Times, and the rest, scores of times. The firms were so familiar, the press had even given them anthropomorphized personalities over the years: Morgan Stanley, the “white-shoe” WASP firm; Merrill Lynch, the scrappy Irish Catholic firm, often considered the dumb one; Goldman, the elite Jewish firm; Lehman, the scrappy Jewish firm; Bear Stearns, the naughty one, and so on. Love them or hate them, there they were, blessed by accounting firms, rating agencies, and regulators, gleaming towers of power. Until one day, they weren’t.

Critics contended, understandably, that the business press must have been asleep at the wheel. In a March 2009 interview that would go viral, the comedian Jon Stewart confronted the CNBC personality Jim Cramer with the problem. Stewart said, in effect, that business journalism presents itself as providing wall-to-wall, 24/7 coverage of Wall Street but had somehow managed to miss the most important thing ever to happen on that beat—the Big One. “It is a game that you know is going on, but you go on television as a financial network and pretend it isn’t happening,” is how Stewart framed it. And many understood exactly what he meant.

Top business-news professionals—also understandably, perhaps—have defended their industry’s pre-crisis performance. In speeches and interviews, these professionals assert that the press in fact did provide clear warnings and presented examples of pre-crisis stories that told about brewing problems in the lending system before the crash. Some have gone further and asserted that it was the public itself that had failed—failed to respond to the timely information the press had been providing all along. “Anybody who’s been paying attention has seen business journalists waving the red flag for several years,” wrote Chris Roush, in an article entitled “Unheeded Warnings,” which articulated the professionals’ view at length. Diana Henriques, a respected New York Times business and investigative reporter, defended her profession in a speech in November 2008: “The government, the financial industry and the American consumer—if they had only paid attention—would have gotten ample warning about this crisis from us, years in advance, when there was still time to evacuate and seek shelter from this storm.” There were many such pronouncements. Then the press moved on.

It is only fair to point out that, beyond speeches and assertions, the business press did not publish a major story on its own peculiar role in the financial system before the crisis. It has, meanwhile,investigated and taken to task, after the fact, virtually every other possible agent in the crisis: Wall Street banks, mortgage lenders, the Federal Reserve, the Securities and Exchange Commission, Fannie Mae, Freddy Mac, the Office of Thrift Supervision, the Office of the Comptroller of the Currency, compensation consultants, and so on. On it own role, the press has been notably silent. This kind of forensic work is entirely appropriate. But what about the watchdog?

In the spring of 2009, the Columbia Journalism Review, where I work as an editor, undertook a project with a simple goal: to assess whether the business press, as it contended, did indeed provide the public with fair warning of looming dangers when it could have made a difference. The idea was to perform a fair reading of the record of institutional business reporting before the crash. I created a commonsense list of nine major business news outlets (the Wall Street Journal, Fortune, Forbes, Businessweek, the Financial Times, Bloomberg, the New York Times, the Los Angeles Times, and the Washington Post) and, with the help of two researchers, used news databases to search for stories that could plausibly be considered warnings about the heart of the problem: abusive mortgage lenders and their funders on Wall Street. We then asked the news outlets to volunteer their best work during this period, and, to their credit, nearly all of them cooperated. (A description of the methodology can be found in chapter 8.)

![]()

The result was “Power Problem,” published in CJR in the spring of 2009. Its conclusion was simple: the business press had done everything but take on the institutions that brought down the financial system. As I’ll discuss in later chapters, the record shows that the press published its hardest-hitting investigations of lenders and Wall Street between 2000 and 2003, even if there were only a few of them. Then, for reasons I will attempt to explain, it lapsed into useful but not sufficient consumer- and investor-oriented stories during the critical years of 2004 through 2006. Missing are investigative stories that directly confront powerful institutions about basic business practices while those institutions were still powerful. The watchdog didn’t bark.

To read various journalistic accounts of mortgage lending and Wall Street during the bubble is to come away with radically differing representations of the soundness of the U.S. financial system. It all depended on what you were reading. Anyone “paying attention” to the conventional business press could be forgiven for thinking that things were, in the end, basically normal. Yes, there was a housing bubble. Any fair reading of the press of the era makes that clear, even if warnings were mitigated by just-as-loud celebrations of the boom. And yes, the press said there were a lot of terrible mortgage products out there. Those are important consumer and investor issues. But that’s all they are. When the gaze turned to financial institutions, the message was entirely different: “all clear.” It’s not just the puff pieces (“Washington Mutual Is Using a Creative Retail Approach to Turn the Banking World Upside Down”; “Citi’s chief hasn’t just stepped out of Sandy Weill’s shadow—he’s stepped out of his own as he strives to make himself into a leader with vision”; and so on) or the language that sometimes lapses into toadying (“Some of its old-world gentility remains: Goldman agreed to talk for this story only reluctantly, wary of looking like a braggart”; “His 6-foot-4 linebacker-esque frame is economically packed into a club chair in his palatial yet understated office”): it’s that even stories that were ostensibly critical of individual Wall Street firms and mortgage lenders described them in terms of their competition with one another: would their earnings be okay? There was a bubble all right, and the business press was in it.

If you enjoyed this excerpt, you can purchase the full book here.

Excerpted from The Watchdog that Didn’t Bark by Dean Starkman. Copyright © 2014 Dean Starkman. Used by arrangement with Columbia University Press. All rights reserved.