Iran War's Explosive Costs Could Finance Health Care Coverage For Millions

The Pentagon is asking the White House for an additional $200 billion to fight the president’s ill-conceived war in the Middle East.

While it’s unclear from the initial news reports whether this is a one-year or multi-year appropriation, the size of the request suggests this war is going to drag on a lot longer and involve far more manpower and firepower than President Trump and Secretary of Defense Pete Hegseth have let on. The now three-week-old war of choice has already left 13 soldiers dead and more than 140 wounded. It has already cost over $12 billion, according to reported estimates.

Let’s put that cost and this latest request in perspective. The $12 billion already spent is enough to have extended the Affordable Care Act subsidies for close to six months.

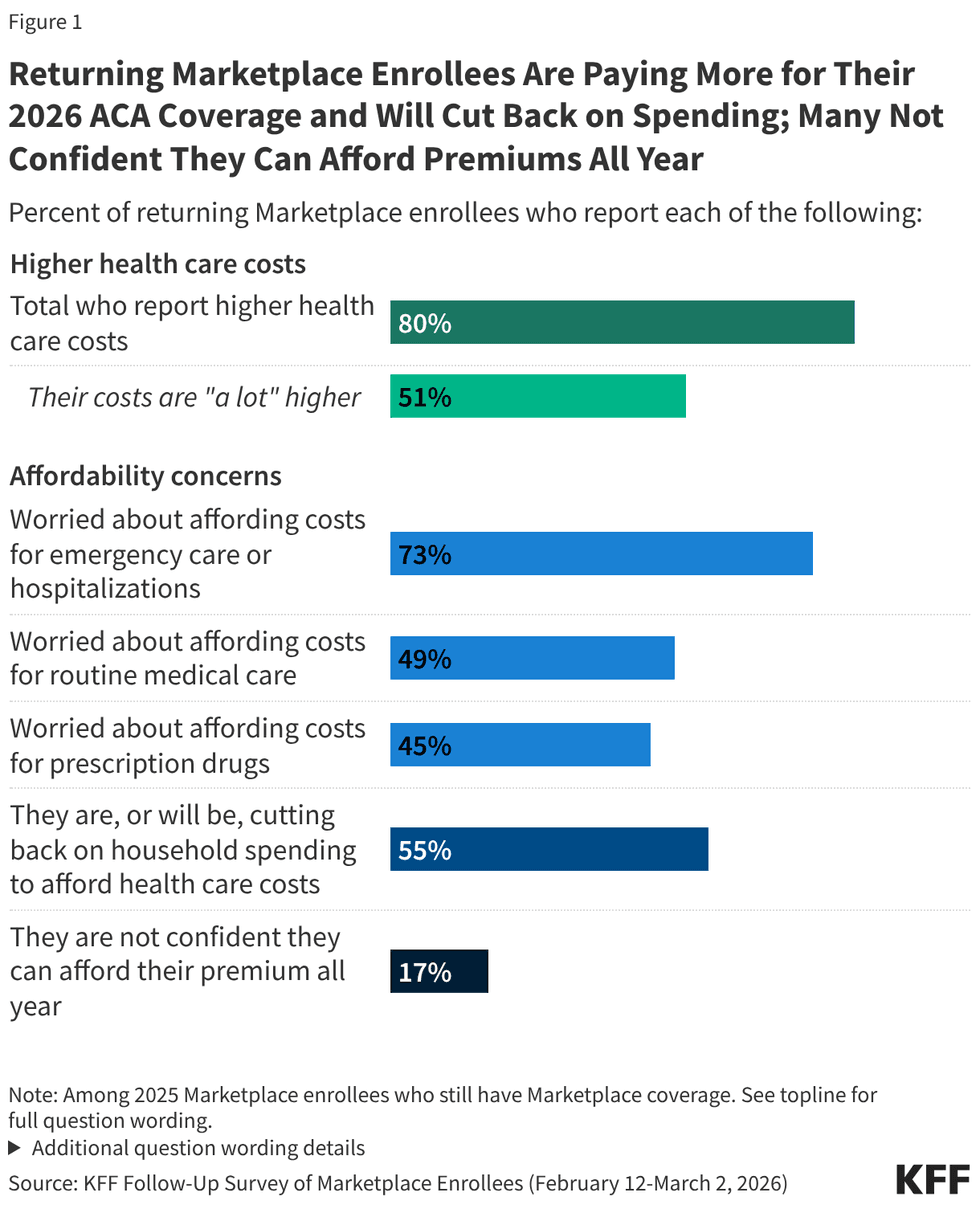

Instead, over two million or nine percent of people in ACA health insurance plans last year dropped them for this year (the first without the expanded subsidies) because they couldn’t afford the huge increase in their premiums, according to a new survey released yesterday by KFF, a health care think tank. That’s nearly a 10 percent increase in the ranks of the uninsured, which alone will bring the uninsured rate close to 10 percent overall.

And many more will drop coverage in the years ahead, given ACA marketplace purchasers’ concerns about their ability to pay the new, higher rates without subsidies.

The $200 billion the Pentagon is requesting is sufficient to extend the ACA subsidies for over five years. Where did I get that estimate? The failure to extend the subsidies helped pay for the $7.7 trillion in tax cuts for the wealthy and large corporations in last year’s One Big Ugly Bill (OBUB). It reduced health care spending by about $350 billion over ten years, an average of $35 billion a year. $200 billion ÷ $35 billion = 5.7 years.

The same math applies to the alleged Medicaid “savings” in the OBUB. Imposing work requirements (a lexicographic subterfuge for erecting bureaucratic barriers that will make it difficult for qualified Medicaid beneficiaries to re-certify their eligibility) will cut an estimated $326 billion from the program over the next decade, according to the Congressional Budget Office. Cuts to the federal share of aid to state Medicaid programs will “save” the federal government another $300 to $400 billion. The two together add up to at least $65 billion a year ripped from Medicaid.

To sum up: Cuts in ACA subsidies and Medicaid in the OBUB will average over $100 billion a year over the next decade. At the rate the Trump regime is spending on the war against Iran, the Pentagon will eat that up in two years.

This accounting doesn’t take into consideration the long-term costs of U.S. involvement in overseas quagmires of its own making. The Iraq War, which began in 2002, cost close to $1 trillion in direct military spending. The long-term cost of caring for the wounded, veterans’ special health care needs, and related spending has been estimated to cost an additional $2 to $3 trillion.

Those of us old enough to remember the Vietnam War will recall the “guns and butter” debate that accompanied President Lyndon B. Johnson’s slow descent into that quagmire. LBJ’s advisers assured him the U.S. could do both.

Wrong. Inflation began escalating by the late 1960s, throwing the country into a recession by December 1969. During the decade after regular combat began in 1965, prices rose by a total of 176 percent, twice the rate of inflation during the previous decade. The biggest increases were triggered by soaring oil prices due to an Arab oil embargo after the 1973 Middle East war.

President George W. Bush tried his hand at guns and butter in 2003 when, to bolster his reelection chances amid widening opposition to the Iraq War, he pushed through an unfunded Medicare drug benefit and pushed further deregulation of the financial sector. By the end of his term in office, the resulting housing bubble and sub-prime lending crisis led to the worst economic downturn since the Great Depression.

While looking up some of the specifics of that history, I stumbled across the origination of the phrase “guns and butter.” It wasn’t a 1960s coinage. It was popularized during the 1930s by German Reich Marshall Hermann Goering, who defended Germany’s huge military build-up by saying, "Guns will make us powerful. Butter will only make us fat."

It was Theodor Reik, a Jewish intellectual who fled Nazi Germany, who in 1965 took issue with the idea that history repeats itself. “This is perhaps not quite correct,” he said. “It merely rhymes.”

What does the Trump regime’s escalating military spending amid evisceration of social spending rhyme with?

Merrill Goozner, the former editor of Modern Healthcare, writes about health care and politics at GoozNews.substack.com, where this column first appeared. Please consider subscribing to support his work.

Reprinted with permission from Gooz News

Source: Atlanta Federal Reserve

Source: Atlanta Federal Reserve